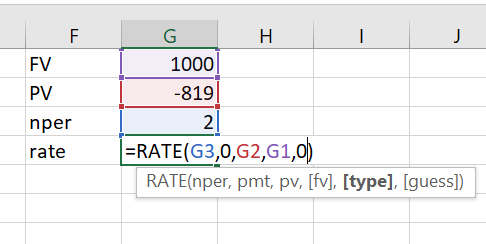

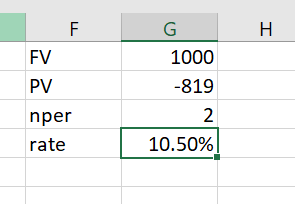

A 2-year $1,000 par zero-coupon bond is currently priced at $819.00. A 2-year $1,000 annuity is...

A 2-year $1,000 par zero-coupon bond is currently priced at $819.00. A 2-year $1,000 annuity is currently priced at $1,712.52. If you want to invest $10,000 in one of the two securities, which is a better buy? You can assume

a. the pure expectations theory of interest rates holds,

b. neither bond has any default risk, maturity premium, or liquidity premium, and

c. you can purchase partial bonds.

| A. |

none of the choices |

|

| B. |

2-year annuity |

|

| C. |

they are equally good |

|

| D. |

2-year zero-coupon bond |

Homework Answers

Interest Rate provided by first bond is 10.5%. Calculation is given below:

And the interest provided by second bond is 11% as per calculation given below:

Hence, 2 year annuity is a better choice

Option B is correct.

Add Answer to:

A 2-year $1,000 par zero-coupon bond is currently priced at

$819.00. A 2-year $1,000 annuity is...

The yield to maturity on 1-year zero-coupon bonds is currently 7%; the YTM on 2-year zeros is 8%. The Government plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupo...

The yield to maturity on 1-year zero-coupon bonds is currently 7%; the YTM on 2-year zeros is 8%. The Government plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 9%. The face value of the bond is $100. a. At what price will the bond sell? b. What will the yield to maturity on the bond be? (Hint: Use a financial calculator to get the YTM) c. If the expectations theory...

The yield to maturity on 1-year zero-coupon bonds is currently 4.5%; the YTM on 2-year zeros...

The yield to maturity on 1-year zero-coupon bonds is currently 4.5%; the YTM on 2-year zeros is 5.5%. The Treasury plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 6% The face value of the bond is $100. a. At what price will the bond sell? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Price b. What will the yield to maturity on the bond be? (Do...

The yield to maturity on 1-year zero-coupon bonds is currently 4.5%; the YTM on 2-year zeros is 5.5%. The Treasury plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 6% The face value of the bond is $100. a. At what price will the bond sell? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Price b. What will the yield to maturity on the bond be? (Do...

2. A bond matures in 7 years, has a par value of $1,000, and an annual...

2. A bond matures in 7 years, has a par value of $1,000, and an annual coupon payment of $70. Investors require a return of 8.5%. Calculate the price of the bond. [8 points] 3. A bond is priced at $1,280, has a par value of $1,000, 15 years to maturity, and a $135 annual coupon. The bond is callable in 5 years at $1,050. Calculate the yield to call. [8 points] 4. If 10-year Treasury bonds yield 6.2%, 10-year...

2. A bond matures in 7 years, has a par value of $1,000, and an annual coupon payment of $70. Investors require a return of 8.5%. Calculate the price of the bond. [8 points] 3. A bond is priced at $1,280, has a par value of $1,000, 15 years to maturity, and a $135 annual coupon. The bond is callable in 5 years at $1,050. Calculate the yield to call. [8 points] 4. If 10-year Treasury bonds yield 6.2%, 10-year...

15.5 The yield to maturity on 1-year zero-coupon bonds is currently 7.5%; the YTM on 2-year...

15.5 The yield to maturity on 1-year zero-coupon bonds is currently 7.5%; the YTM on 2-year zeros is 8.5%. The Treasury plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 9.5%. The face value of the bond is $100. a. At what price will the bond sell? (Do not round intermediate calculations. Round your answer to 2 decimal places.) b. What will the yield to maturity on the bond be? (Do...

The yield to maturity on 1-year zero-coupon bonds is currently 6.5%; the YTM on 2-year zeros...

The yield to maturity on 1-year zero-coupon bonds is currently 6.5%; the YTM on 2-year zeros is 7.5%. The Government of Canada plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 8.5%. The face value of the bond is $100. a. At what price will the bond sell? (Do not round intermediate calculations. Round your answer to 2 decimal places. Omit the "$" sign in your response.) 6.25 points Price $...

The yield to maturity on 1-year zero-coupon bonds is currently 6.5%; the YTM on 2-year zeros is 7.5%. The Government of Canada plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 8.5%. The face value of the bond is $100. a. At what price will the bond sell? (Do not round intermediate calculations. Round your answer to 2 decimal places. Omit the "$" sign in your response.) 6.25 points Price $...

The following information is for zero-coupon bonds with $1,000 maturity value. Maturity (years) Bond Price ($)...

The following information is for zero-coupon bonds with $1,000 maturity value. Maturity (years) Bond Price ($) 970 940 910 a) Derive the yield curve that is consistent with the above data. b) Assume the liquidity preference hypothesis holds and the liquidity premium for each period is constant at 1%. What is the “true” three-year spot rate?

The following information is for zero-coupon bonds with $1,000 maturity value. Maturity (years) Bond Price ($) 970 940 910 a) Derive the yield curve that is consistent with the above data. b) Assume the liquidity preference hypothesis holds and the liquidity premium for each period is constant at 1%. What is the “true” three-year spot rate?

What is the yield-to-maturity of a $1,000 zero-coupon 2-year note priced at 96.79 and maturing on...

What is the yield-to-maturity of a $1,000 zero-coupon 2-year note priced at 96.79 and maturing on Dec. 15, 2019? Assume you bought the bond on February 21, 2018. Current rates are 3.5%.

Help with finance question please. 7. Below is a list of prices for $1,000 par zero-coupon...

Help with finance question please.

7. Below is a list of prices for $1,000 par zero-coupon bonds of various maturities. Maturity (Years) Bond AWNA Price $930 $850 $770 $700 1.4 a. Compute the zero-coupon rates for years 1, 2, 3 and 4. b. Consider an 8% coupon $1,000 par bond (denoted by B) paying annual coupons and expiring in 4 years. Compute the no-arbitrage price of the bond and its yield-to-maturity. c. If the expectations hypothesis holds, what is your...

Help with finance question please.

7. Below is a list of prices for $1,000 par zero-coupon bonds of various maturities. Maturity (Years) Bond AWNA Price $930 $850 $770 $700 1.4 a. Compute the zero-coupon rates for years 1, 2, 3 and 4. b. Consider an 8% coupon $1,000 par bond (denoted by B) paying annual coupons and expiring in 4 years. Compute the no-arbitrage price of the bond and its yield-to-maturity. c. If the expectations hypothesis holds, what is your...

Which of the following are correct? i. The liquidity premium for a 2-year government bond is...

Which of the following are correct? i. The liquidity premium for a 2-year government bond is higher than the liquidity premium for a 5-year government bond. ii. The liquidity premium for a 3-year government bond is lower than the liquidity premium for a 3-year corporate bond. iii. The expected return from holding an illiquid two year zero-coupon bond to maturity is higher than the expected return from buying a liquid one-year zero-coupon bond (and holding it to maturity) followed by...

4. Suppose a coupon bond with a par value of $1,000 is currently priced at $950...

4. Suppose a coupon bond with a par value of $1,000 is currently priced at $950 and has a coupon of $40. Which of the following is true? A) current yield < coupon rate B) current yield> coupon rate C) coupon rate has risen D) coupon rate has declined

4. Suppose a coupon bond with a par value of $1,000 is currently priced at $950 and has a coupon of $40. Which of the following is true? A) current yield < coupon rate B) current yield> coupon rate C) coupon rate has risen D) coupon rate has declined

The yield to maturity on 1-year zero-coupon bonds is currently 4.5%; the YTM on 2-year zeros is 5.5%. The Treasury plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 6% The face value of the bond is $100. a. At what price will the bond sell? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Price b. What will the yield to maturity on the bond be? (Do...

The yield to maturity on 1-year zero-coupon bonds is currently 4.5%; the YTM on 2-year zeros is 5.5%. The Treasury plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 6% The face value of the bond is $100. a. At what price will the bond sell? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Price b. What will the yield to maturity on the bond be? (Do...

2. A bond matures in 7 years, has a par value of $1,000, and an annual coupon payment of $70. Investors require a return of 8.5%. Calculate the price of the bond. [8 points] 3. A bond is priced at $1,280, has a par value of $1,000, 15 years to maturity, and a $135 annual coupon. The bond is callable in 5 years at $1,050. Calculate the yield to call. [8 points] 4. If 10-year Treasury bonds yield 6.2%, 10-year...

2. A bond matures in 7 years, has a par value of $1,000, and an annual coupon payment of $70. Investors require a return of 8.5%. Calculate the price of the bond. [8 points] 3. A bond is priced at $1,280, has a par value of $1,000, 15 years to maturity, and a $135 annual coupon. The bond is callable in 5 years at $1,050. Calculate the yield to call. [8 points] 4. If 10-year Treasury bonds yield 6.2%, 10-year...

The yield to maturity on 1-year zero-coupon bonds is currently 6.5%; the YTM on 2-year zeros is 7.5%. The Government of Canada plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 8.5%. The face value of the bond is $100. a. At what price will the bond sell? (Do not round intermediate calculations. Round your answer to 2 decimal places. Omit the "$" sign in your response.) 6.25 points Price $...

The yield to maturity on 1-year zero-coupon bonds is currently 6.5%; the YTM on 2-year zeros is 7.5%. The Government of Canada plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 8.5%. The face value of the bond is $100. a. At what price will the bond sell? (Do not round intermediate calculations. Round your answer to 2 decimal places. Omit the "$" sign in your response.) 6.25 points Price $...

The following information is for zero-coupon bonds with $1,000 maturity value. Maturity (years) Bond Price ($) 970 940 910 a) Derive the yield curve that is consistent with the above data. b) Assume the liquidity preference hypothesis holds and the liquidity premium for each period is constant at 1%. What is the “true” three-year spot rate?

The following information is for zero-coupon bonds with $1,000 maturity value. Maturity (years) Bond Price ($) 970 940 910 a) Derive the yield curve that is consistent with the above data. b) Assume the liquidity preference hypothesis holds and the liquidity premium for each period is constant at 1%. What is the “true” three-year spot rate?

Help with finance question please.

7. Below is a list of prices for $1,000 par zero-coupon bonds of various maturities. Maturity (Years) Bond AWNA Price $930 $850 $770 $700 1.4 a. Compute the zero-coupon rates for years 1, 2, 3 and 4. b. Consider an 8% coupon $1,000 par bond (denoted by B) paying annual coupons and expiring in 4 years. Compute the no-arbitrage price of the bond and its yield-to-maturity. c. If the expectations hypothesis holds, what is your...

Help with finance question please.

7. Below is a list of prices for $1,000 par zero-coupon bonds of various maturities. Maturity (Years) Bond AWNA Price $930 $850 $770 $700 1.4 a. Compute the zero-coupon rates for years 1, 2, 3 and 4. b. Consider an 8% coupon $1,000 par bond (denoted by B) paying annual coupons and expiring in 4 years. Compute the no-arbitrage price of the bond and its yield-to-maturity. c. If the expectations hypothesis holds, what is your...

4. Suppose a coupon bond with a par value of $1,000 is currently priced at $950 and has a coupon of $40. Which of the following is true? A) current yield < coupon rate B) current yield> coupon rate C) coupon rate has risen D) coupon rate has declined

4. Suppose a coupon bond with a par value of $1,000 is currently priced at $950 and has a coupon of $40. Which of the following is true? A) current yield < coupon rate B) current yield> coupon rate C) coupon rate has risen D) coupon rate has declined

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago