I ONLY NEED PART (E) PLEASE! On a market with monopolistic competition, a firm meets the demand Q...

I ONLY NEED PART (E) PLEASE!

On a market with monopolistic competition, a firm meets the

demand Q

D

= 400 – 4P. The

firm’s marginal cost is given by MC = 40 + 2Q.

A. Which quantity should the firm produce to maximize its profit?

Which is the profit

maximizing price on the market?

B. Draw a figure that shows the firm’s profit maximizing quantity

and price.

C. What is the firm’s long-term profit?

D. Now instead assume the market is a duopoly, and that the total

demand is given by Q

D

=

1600 – 2P. The two firms on the market, Delta and Gamme, have

identical cost functions

TC

D

= TC

G

= 200 + 50Q. The firm’s respective boards have agreed to

collaborate to

maximize their collective profit. What is the profit of Delta and

Gamma if the firms together

agree on which quantity to produce?

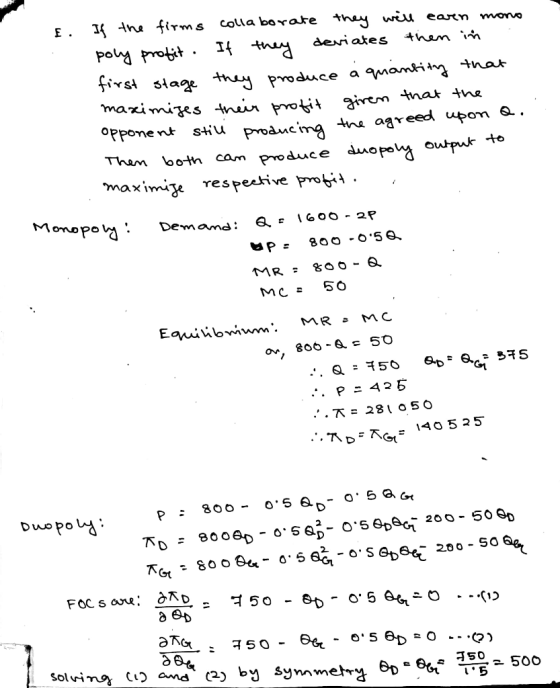

E. Gamma’s board doesn’t trust Delta’s board and therefore lays out

a strategy for what

would happen if Delta deviates from the firms’ mutual agreement.

Since Gamma’s chief

economist recently brushed up on his game theory, he’d like to make

use of it immediately.

What would the result matrix that the chief economist would produce

look like, based on your

calculations from part A of this question? As your starting point,

consider that the firms can

choose to produce the agreed-upon quantity from part A, and another

quantity. Also provide

the combinations of strategies that provide the Nash equilibrium

points.

I ONLY NEED PART (E) PLEASE on this one!

Homework Answers

Add Answer to:

I ONLY NEED PART (E) PLEASE! On a market with monopolistic competition, a firm meets the demand Q...

I ONLY NEED PART (E) PLEASE! On a market with monopolistic competition, a firm meets the...

I ONLY NEED PART (E) PLEASE! On a market with monopolistic competition, a firm meets the demand Q D = 400 – 4P. The firm’s marginal cost is given by MC = 40 + 2Q. A. Which quantity should the firm produce to maximize its profit? Which is the profit maximizing price on the market? B. Draw a figure that shows the firm’s profit maximizing quantity and price. C. What is the firm’s long-term profit? D. Now instead assume the...

i just need the answer for "e". Problem 1 (4 points) Knope Industries is a firm...

i

just need the answer for "e".

Problem 1 (4 points) Knope Industries is a firm that produces miniature model souvenirs with total cost function TC(Q) = 2500 + 50Q +0.02Q2 (e) Sketch a graph with the demand curve, marginal revenue curve, and marginal cost curve, and label the profit-maximizing price and quantity. (1 pt) Problem 1 (4 points) Knope Industries is a firm that produces miniature model souvenirs with total cost function TCQ) = 2500+ 500+ 0.02Q (a) Write...

i

just need the answer for "e".

Problem 1 (4 points) Knope Industries is a firm that produces miniature model souvenirs with total cost function TC(Q) = 2500 + 50Q +0.02Q2 (e) Sketch a graph with the demand curve, marginal revenue curve, and marginal cost curve, and label the profit-maximizing price and quantity. (1 pt) Problem 1 (4 points) Knope Industries is a firm that produces miniature model souvenirs with total cost function TCQ) = 2500+ 500+ 0.02Q (a) Write...

Two duopoly firms each have a cost function: TC(Q) 60Q Market Inverse Demand is: Pp (Q)824 0.6Q After the duopolist...

Two duopoly firms each have a cost function: TC(Q) 60Q Market Inverse Demand is: Pp (Q)824 0.6Q After the duopolists meet secretly and agree to evenly split the profit-maximizing output, Firm 1 decides to break the monopoly-splitting agreement and change its output to maximize its own profit. What will be the net loss of profit for the two firms to the nearest dollar?

Two duopoly firms each have a cost function: TC(Q) 60Q Market Inverse Demand is: Pp (Q)824 0.6Q...

Two duopoly firms each have a cost function: TC(Q) 60Q Market Inverse Demand is: Pp (Q)824 0.6Q After the duopolists meet secretly and agree to evenly split the profit-maximizing output, Firm 1 decides to break the monopoly-splitting agreement and change its output to maximize its own profit. What will be the net loss of profit for the two firms to the nearest dollar?

Two duopoly firms each have a cost function: TC(Q) 60Q Market Inverse Demand is: Pp (Q)824 0.6Q...

3. Suppose the firm in monopolistic market faces the following demand function: Q = 5,000 -...

3. Suppose the firm in monopolistic market faces the following demand function: Q = 5,000 - 125P ; and total cost function TC - 50 +0.00802 a. Write the equation for the inverse demand function. (1 pt) b. Find the marginal revenue function. (1 pt) c. How much output should the manager produce to maximize profit? What price should be charged for the output? (2 pt) d. Calculate the marginal cost function. (2 pt) e. At the output level, how...

3. Suppose the firm in monopolistic market faces the following demand function: Q = 5,000 - 125P ; and total cost function TC - 50 +0.00802 a. Write the equation for the inverse demand function. (1 pt) b. Find the marginal revenue function. (1 pt) c. How much output should the manager produce to maximize profit? What price should be charged for the output? (2 pt) d. Calculate the marginal cost function. (2 pt) e. At the output level, how...

Two duopoly firms each have a cost function: TC (Q) 600 Market Inverse Demand is: Po (Q)-824 0.6Q After the duopoli...

Two duopoly firms each have a cost function: TC (Q) 600 Market Inverse Demand is: Po (Q)-824 0.6Q After the duopolists meet secretly and agree to evenly split the profit-maximizing output, Firm 1 decides to break the monopoly-splitting agreement and change its output to maximize its own profit. What will be the reduction in price for both firms to the nearest dollar? (Subtract the new price from the monopoly price]

Two duopoly firms each have a cost function: TC (Q)...

Two duopoly firms each have a cost function: TC (Q) 600 Market Inverse Demand is: Po (Q)-824 0.6Q After the duopolists meet secretly and agree to evenly split the profit-maximizing output, Firm 1 decides to break the monopoly-splitting agreement and change its output to maximize its own profit. What will be the reduction in price for both firms to the nearest dollar? (Subtract the new price from the monopoly price]

Two duopoly firms each have a cost function: TC (Q)...

11.3 A single firm monopolizes the entire market for Batman masks and can produce at constant...

11.3 A single firm monopolizes the entire market for Batman masks and can produce at constant average and marginal costs of AC=MC=10: Originally, the firm faces a market demand curve given by Q=60-P a. Calculate the profit-maximizing price-quantity combination for the firm. What are the firm’s profits? b. Now assume that the market demand curve becomes steeper and is given by Q=45-0.5P with the marginal revenue function given by MR=90-4Q: What is the firm’s profit-maximizing price quantity combination now? What...

A single firm monopolizes the entire market for single-lever, ball-type faucets which it can produce at...

A single firm monopolizes the entire market for single-lever, ball-type faucets which it can produce at a constant average and marginal cost of AC=MC=10. Originally, the firm faces a market demand curve given by Q=60 – P Calculate the profit-maximizing price and quantity combination for the firm. What is the firm’s profit? Suppose the market demand curve shifts outward and becomes steeper. Market demand is now described as Q=45-0.5P. What is the firm’s profit maximizing price and quantity combination now?...

Please Answer Part 2. The market for fabric has only one producer. Assume that daily market...

Please Answer Part 2. The market for fabric has only one producer. Assume that daily market demand for fabric is y = 100,000 - 100p, where y denotes the quantity and p denotes the unit price. Also assume that producing y units of fabric costs 100y. 1. How many units of fabric should the producer produce and sell in order to maximize profits? Calculate the profit-maximizing price and the profit. 2. Now suppose that to produce one unit of fabric...

The market demand curve is given by Q = 200-2p. There is one dominant firm, which sets the market...

The market demand curve is given by Q = 200-2p. There is one dominant firm, which sets the market price and has a constant marginal cost of 5, and a competitive fringe of 10 price-taking firms, each of which has a marginal cost function MC (Q) = 10 +Q. Derive the equation of the dominant firm’s residual demand curve. What price will the dominant firm set to maximize its profits? At this price, how much does the competitive fringe produce?

3. Consider a market of two firms with demand given by P = 200 – Q....

3. Consider a market of two firms with demand given by P = 200 – Q. Each firm has a constant marginal cost of $20 and fixed costs of $2,000. Competition is characterized by making simultaneous profit-maximizing quantity decisions. a. What will be an individual firm’s quantities and profits if n = 2? n = 3? n = 4? (Make sure to include fixed costs in your profit calculations.) b. Assuming no changes to demand or cost structure, how many...

i

just need the answer for "e".

Problem 1 (4 points) Knope Industries is a firm that produces miniature model souvenirs with total cost function TC(Q) = 2500 + 50Q +0.02Q2 (e) Sketch a graph with the demand curve, marginal revenue curve, and marginal cost curve, and label the profit-maximizing price and quantity. (1 pt) Problem 1 (4 points) Knope Industries is a firm that produces miniature model souvenirs with total cost function TCQ) = 2500+ 500+ 0.02Q (a) Write...

i

just need the answer for "e".

Problem 1 (4 points) Knope Industries is a firm that produces miniature model souvenirs with total cost function TC(Q) = 2500 + 50Q +0.02Q2 (e) Sketch a graph with the demand curve, marginal revenue curve, and marginal cost curve, and label the profit-maximizing price and quantity. (1 pt) Problem 1 (4 points) Knope Industries is a firm that produces miniature model souvenirs with total cost function TCQ) = 2500+ 500+ 0.02Q (a) Write...

Two duopoly firms each have a cost function: TC(Q) 60Q Market Inverse Demand is: Pp (Q)824 0.6Q After the duopolists meet secretly and agree to evenly split the profit-maximizing output, Firm 1 decides to break the monopoly-splitting agreement and change its output to maximize its own profit. What will be the net loss of profit for the two firms to the nearest dollar?

Two duopoly firms each have a cost function: TC(Q) 60Q Market Inverse Demand is: Pp (Q)824 0.6Q...

Two duopoly firms each have a cost function: TC(Q) 60Q Market Inverse Demand is: Pp (Q)824 0.6Q After the duopolists meet secretly and agree to evenly split the profit-maximizing output, Firm 1 decides to break the monopoly-splitting agreement and change its output to maximize its own profit. What will be the net loss of profit for the two firms to the nearest dollar?

Two duopoly firms each have a cost function: TC(Q) 60Q Market Inverse Demand is: Pp (Q)824 0.6Q...

3. Suppose the firm in monopolistic market faces the following demand function: Q = 5,000 - 125P ; and total cost function TC - 50 +0.00802 a. Write the equation for the inverse demand function. (1 pt) b. Find the marginal revenue function. (1 pt) c. How much output should the manager produce to maximize profit? What price should be charged for the output? (2 pt) d. Calculate the marginal cost function. (2 pt) e. At the output level, how...

3. Suppose the firm in monopolistic market faces the following demand function: Q = 5,000 - 125P ; and total cost function TC - 50 +0.00802 a. Write the equation for the inverse demand function. (1 pt) b. Find the marginal revenue function. (1 pt) c. How much output should the manager produce to maximize profit? What price should be charged for the output? (2 pt) d. Calculate the marginal cost function. (2 pt) e. At the output level, how...

Two duopoly firms each have a cost function: TC (Q) 600 Market Inverse Demand is: Po (Q)-824 0.6Q After the duopolists meet secretly and agree to evenly split the profit-maximizing output, Firm 1 decides to break the monopoly-splitting agreement and change its output to maximize its own profit. What will be the reduction in price for both firms to the nearest dollar? (Subtract the new price from the monopoly price]

Two duopoly firms each have a cost function: TC (Q)...

Two duopoly firms each have a cost function: TC (Q) 600 Market Inverse Demand is: Po (Q)-824 0.6Q After the duopolists meet secretly and agree to evenly split the profit-maximizing output, Firm 1 decides to break the monopoly-splitting agreement and change its output to maximize its own profit. What will be the reduction in price for both firms to the nearest dollar? (Subtract the new price from the monopoly price]

Two duopoly firms each have a cost function: TC (Q)...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago