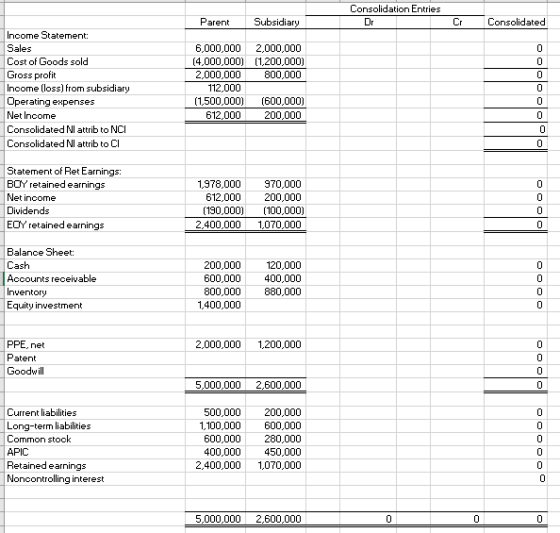

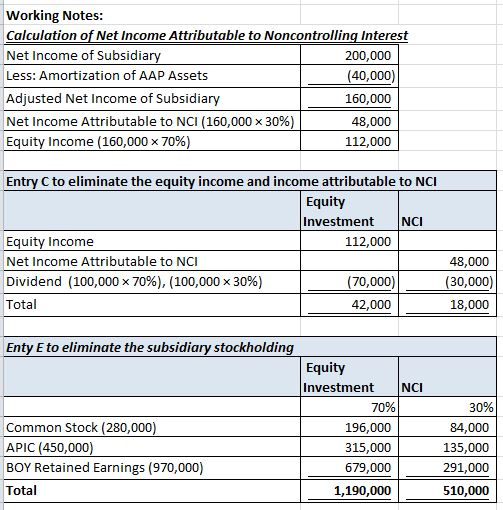

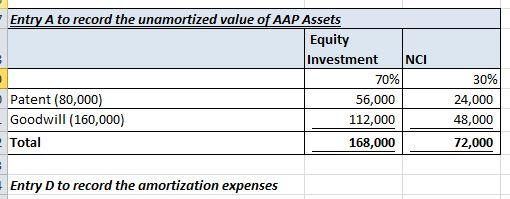

Assume that on 1/1/X0, a parent company acquires a 70% interest in its subsidiary for a price at $480,000 over book value. The excess is assigned as follows:

| Asset | Fair Value | Useful Life |

| Patent | $320,000 | 8 years |

| Goodwill | 160,000 | Indefinite |

70% of the goodwill is allocated to the parent.

Included in the attached Excel spreadsheet are the pre-consolidation financial statements for both the parent and the subsidiary.

Submission Requirements:

- Prepare the consolidated financial statements at 12/31/X6 by placing the appropriate entries in their respective debit/credit column cells.

- Indicate, in the blank column cell to the left of the debit and credit column cells if the entry is a [C], [E], [A], [D] or [I]entry.

- Use Excel formulas to derive the Consolidated column amounts

and totals.

- Using the “Home” key in Excel, go to the “Styles” area and highlight the [C], [E], [A], [D] or [I]entry cells in different shades.

Homework Answers

Add Answer to:

Assume that on 1/1/X0, a parent company acquires a 70% interest in its subsidiary for a price at ...

Consolidation at Date Acquisition, Ownership <100%, FMV>BV. Assume that a parent company acquires a 70% interest...

Consolidation at Date Acquisition, Ownership <100%, FMV>BV. Assume that a parent company acquires a 70% interest in a subsidiary for a purchase price of $1,078,000. The excess of total fair value of controlling and noncontrolling interests over book value is assigned to; a building (PPE net) that is worth $100,000 more than book value, an unrecorded patent valued at $200,000 and goodwill valued at $300,000. Goodwill is assigned proportionately to the controlling and noncontrolling interests. Prepare the consolidated balance sheet...

Consolidation at Date Acquisition, Ownership <100%, FMV>BV. Assume that a parent company acquires a 70% interest...

Consolidation at Date Acquisition, Ownership <100%, FMV>BV. Assume that a parent company acquires a 70% interest in a subsidiary for a purchase price of $1,078,000. The excess of total fair value of controlling and noncontrolling interests over book value is assigned to; a building (PPE net) that is worth $100,000 more than book value, an unrecorded patent valued at $200,000 and goodwill valued at $300,000. Goodwill is assigned proportionately to the controlling and noncontrolling interests. Prepare the consolidated balance sheet...

Consolidation at Date Acquisition, Ownership <100%, FMV>BV. Assume that a parent company acquires a 70% interest...

Consolidation at Date Acquisition, Ownership <100%, FMV>BV. Assume that a parent company acquires a 70% interest in a subsidiary for a purchase price of $1,078,000. The excess of total fair value of controlling and noncontrolling interests over book value is assigned to; a building (PPE net) that is worth $100,000 more than book value, an unrecorded patent valued at $200,000 and goodwill valued at $300,000. Goodwill is assigned proportionately to the controlling and noncontrolling interests. Submission Requirements: • Prepare the...

Assume the Parent company acquires its subsidiary by exchanging 35,000 shares of its Common Stock, with...

Assume the Parent company acquires its subsidiary by exchanging 35,000 shares of its Common Stock, with a fair value on the acquisition date of $60 per share, for all of the outstanding voting shares of the investee. In its analysis of the investee company, the parent values all of the subsidiary’s assets and liabilities at an amount equaling their book values except for an unrecorded Patent owned by the subsidiary with a fair value of $200,000. Any further discrepancy between...

Below is the equity section of the consolidated worksheet between a parent and its subsidiary Subsidiary...

Below is the equity section of the consolidated worksheet between a parent and its subsidiary Subsidiary Parent Accounts Payable 1,083 890 Long-term Debt 2,013 1,262 Common Stock 3,356 1,759 Retained Earnings 5,467 4,677 Here is the separate income and dividends paid during the year Separate Net Income Dividends Declared Parent 9,434 2,201 Subsidiary 2,520 850 After the consolidation entry is prepared the consolidated net income will be $

Below is the equity section of the consolidated worksheet between a parent...

Below is the equity section of the consolidated worksheet between a parent and its subsidiary Subsidiary Parent Accounts Payable 1,083 890 Long-term Debt 2,013 1,262 Common Stock 3,356 1,759 Retained Earnings 5,467 4,677 Here is the separate income and dividends paid during the year Separate Net Income Dividends Declared Parent 9,434 2,201 Subsidiary 2,520 850 After the consolidation entry is prepared the consolidated net income will be $

Below is the equity section of the consolidated worksheet between a parent...

Assume that a parent company owns 75 percent of its subsidiary. On January 1, 2016, the...

Assume that a parent company owns 75 percent of its subsidiary. On January 1, 2016, the parent company had a $100,000 (face value) 8 percent bond payable outstanding with a carrying value of $94,000. Several years ago, the bond was originally issued to an unaffiliated company for 92% of par value. On January 1, 2016, the subsidiary acquired the bond for $91,000. During 2016, the parent company reported $400,000 of (pre-consolidation) income from its own operations (prior to any equity...

Option #1: Consolidation at Date Acquisition, Ownership < 100%, FMV>BV. Assume that a parent company acquires...

Option #1: Consolidation at Date Acquisition, Ownership < 100%, FMV>BV. Assume that a parent company acquires a 70% interest in a subsidiary for a purchase price of $1,078,000. The excess of total fair value of controlling and noncontrolling interests over book value is assigned to; a building (PPE net) that is worth $100,000 more than book value, an unrecorded patent valued at $200,000 and goodwill valued at $300,000. Goodwill is assigned proportionately to the controlling and noncontrolling interests. Submission Requirements:...

Option #1: Consolidation at Date Acquisition, Ownership < 100%, FMV>BV. Assume that a parent company acquires a 70% interest in a subsidiary for a purchase price of $1,078,000. The excess of total fair value of controlling and noncontrolling interests over book value is assigned to; a building (PPE net) that is worth $100,000 more than book value, an unrecorded patent valued at $200,000 and goodwill valued at $300,000. Goodwill is assigned proportionately to the controlling and noncontrolling interests. Submission Requirements:...

Determining ending balances of accounts on the consolidated balance sheet Assume that the parent company acquires...

Determining ending balances of accounts on the consolidated balance sheet Assume that the parent company acquires its subsidiary by exchanging 80,000 shares of its Common Stock, with a fair value on the acquisition date of $24 per share, for all of the outstanding voting shares of the investee. In its analysis of the investee company, the parent values all of the subsidiary’s assets and liabilities at an amount equaling their book values except for a building that is undervalued by...

Inferring consolidation entries from consolidated financial statements—Cost method Assume a parent company acquired a subsidiary on...

Inferring consolidation entries from consolidated financial statements—Cost method Assume a parent company acquired a subsidiary on January 1, 2012. The purchase price was $1,312,000 in excess of the subsidiary’s book value of Stockholders’ Equity on the acquisition date, and that excess was assigned to the following [A] assets: [A] Asset Original Amount Original Useful Life Property, plant and equipment (PPE), net $300,000 20 years Patent 432,000 12 years Goodwill 580,000 Indefinite $1,312,000 The parent company uses the cost method of...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume a parent...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume a parent company acquires a 75% interest in its subsidiary for a purchase price of $924,000. The excess of the total fair value of the controlling and noncontrolling Interests over the book value of the subsidiary's Stockholders' Equity is assigned to a building in PPE, net) that is worth $88,000 more than its book value, an unrecorded patent with a fair value of $144,000, and Goodwill...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume a parent company acquires a 75% interest in its subsidiary for a purchase price of $924,000. The excess of the total fair value of the controlling and noncontrolling Interests over the book value of the subsidiary's Stockholders' Equity is assigned to a building in PPE, net) that is worth $88,000 more than its book value, an unrecorded patent with a fair value of $144,000, and Goodwill...

Below is the equity section of the consolidated worksheet between a parent and its subsidiary Subsidiary Parent Accounts Payable 1,083 890 Long-term Debt 2,013 1,262 Common Stock 3,356 1,759 Retained Earnings 5,467 4,677 Here is the separate income and dividends paid during the year Separate Net Income Dividends Declared Parent 9,434 2,201 Subsidiary 2,520 850 After the consolidation entry is prepared the consolidated net income will be $

Below is the equity section of the consolidated worksheet between a parent...

Below is the equity section of the consolidated worksheet between a parent and its subsidiary Subsidiary Parent Accounts Payable 1,083 890 Long-term Debt 2,013 1,262 Common Stock 3,356 1,759 Retained Earnings 5,467 4,677 Here is the separate income and dividends paid during the year Separate Net Income Dividends Declared Parent 9,434 2,201 Subsidiary 2,520 850 After the consolidation entry is prepared the consolidated net income will be $

Below is the equity section of the consolidated worksheet between a parent...

Option #1: Consolidation at Date Acquisition, Ownership < 100%, FMV>BV. Assume that a parent company acquires a 70% interest in a subsidiary for a purchase price of $1,078,000. The excess of total fair value of controlling and noncontrolling interests over book value is assigned to; a building (PPE net) that is worth $100,000 more than book value, an unrecorded patent valued at $200,000 and goodwill valued at $300,000. Goodwill is assigned proportionately to the controlling and noncontrolling interests. Submission Requirements:...

Option #1: Consolidation at Date Acquisition, Ownership < 100%, FMV>BV. Assume that a parent company acquires a 70% interest in a subsidiary for a purchase price of $1,078,000. The excess of total fair value of controlling and noncontrolling interests over book value is assigned to; a building (PPE net) that is worth $100,000 more than book value, an unrecorded patent valued at $200,000 and goodwill valued at $300,000. Goodwill is assigned proportionately to the controlling and noncontrolling interests. Submission Requirements:...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume a parent company acquires a 75% interest in its subsidiary for a purchase price of $924,000. The excess of the total fair value of the controlling and noncontrolling Interests over the book value of the subsidiary's Stockholders' Equity is assigned to a building in PPE, net) that is worth $88,000 more than its book value, an unrecorded patent with a fair value of $144,000, and Goodwill...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume a parent company acquires a 75% interest in its subsidiary for a purchase price of $924,000. The excess of the total fair value of the controlling and noncontrolling Interests over the book value of the subsidiary's Stockholders' Equity is assigned to a building in PPE, net) that is worth $88,000 more than its book value, an unrecorded patent with a fair value of $144,000, and Goodwill...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago