![Customer list Royalty agreement PPE net Customer list [lcogs isales] [lcogs] [ipay]](http://img.homeworklib.com/images/95e9246f-3c9e-41d3-a3d5-af31f40d5ae0.png?x-oss-process=image/resize,w_560)

![[lpay] d. Prepare the consolidation spreadsheet for the year ended December 31, 2013. Hint: Use negative signs with answers w](http://img.homeworklib.com/images/86c47c93-85c6-45ec-8254-c2b146bc55b0.png?x-oss-process=image/resize,w_560)

![ID) Royalty agreement Goodwill IC] Equity investment [lcogs] Liabilities and stockholders equity $93,459 Ipayl Accounts paya](http://img.homeworklib.com/images/d825f455-551f-4aa9-b7ae-3c82cd400212.png?x-oss-process=image/resize,w_560)

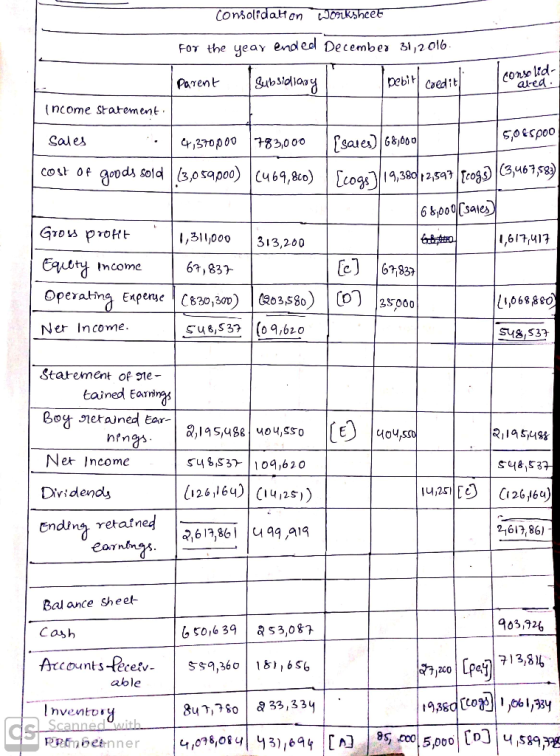

The financial statements of the parent and its subsidiary for the year ended December 31, 2013, follow in part d. below. a. Show the computation to yield the pre-consolidation $71,837 Income (loss) from subsidiary reported by the parent during 2013. Hint: Use negative signs with answers when appropriate. Plus: Less: Income (loss) from subsidiary b. Show the computation to yield the Equity Investment balance of $962,189 reported by the parent at December 31, 2013. Hint: Use negative signs with answers when appropriate. Common stock APIC Retained earnings BOY unamortized AAP BOY deferred profit Income (loss) from subsidiary Dividends

Customer list Royalty agreement PPE net Customer list [lcogs isales] [lcogs] [ipay]

[lpay] d. Prepare the consolidation spreadsheet for the year ended December 31, 2013. Hint: Use negative signs with answers when appropriate Elimination Entries Sub Parent Consolidated Income statement: $787,000 [Isales] Sales $4,370,000 (469,800) [Icogs] (3,059,000) Cost of goods sold [lcogs] lsales] Gross profit 317,200 1,311,000 Income (loss) from subsidiary 71,837 IC] 203,580) [D] (830,300) Operating expenses $552,537 $113,620 Net income Statement of retained earnings 404,550 E] BOY retained earnings $2,195,488 113,620 Net income 552,537 (130,164) (14,251) Dividends

ID) Royalty agreement Goodwill IC] Equity investment [lcogs] Liabilities and stockholders' equity $93,459 Ipayl Accounts payable $327,313 Other current liabilities 403,228 127,943 Long-term liabilities 2,500,000 261,000 714,495 52,200 [E] Common stock 535,155 65,250 E] APIC 2,617,861 503,919 Retained earnings $7,098,052 $1,103,771

Homework Answers

![Royalty igiecncn o o000 0,00 o ,82 1,099, ccounts payable | 323313 | q3,459 | Cray] | 27,200 Other cuene la- 343,s72 2A43 61,](http://img.homeworklib.com/images/53da0cfe-15d2-4dbd-8cea-23a3a5cf1305.png?x-oss-process=image/resize,w_560)

Add Answer to:

Consolidation spreadsheet for continuous sale of inventory - Equity method Assume that a parent c...

Prepare consolidation spreadsheet for intercompany sale of land - Equity method Assume that a parent company acquired i...

Prepare consolidation spreadsheet for intercompany sale of land - Equity method Assume that a parent company acquired its subsidiary on January 1, 2014, at a purchase price that was $300,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. Of that excess, $200,000 was assigned to an unrecorded Patent owned by the subsidiary that is being amortized over a 10-year period. The [A] Patent asset has been amortized as part of the parent's equity...

Prepare consolidation spreadsheet for intercompany sale of land - Equity method Assume that a parent company acquired its subsidiary on January 1, 2014, at a purchase price that was $300,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. Of that excess, $200,000 was assigned to an unrecorded Patent owned by the subsidiary that is being amortized over a 10-year period. The [A] Patent asset has been amortized as part of the parent's equity...

c. Complete the consolidating entries according to the C-E-A-D-I sequence and complete the consolidation worksheet. Use...

c. Complete the consolidating entries according to the

C-E-A-D-I sequence and complete the consolidation

worksheet.

Use negative signs with answers in the

Consolidated column for Cost of goods sold, Operating expenses and

Dividends.

Consolidation Worksheet

Income statement

Parent

Subsidiary

Debit

Credit

Consolidated

Sales

$3,045,000

$560,000

[Isales]

Answer

Answer

Cost of goods sold

(2,135,000)

(336,000)

[Icogs]

Answer

Answer

[Icogs]

Answer

Answer

[Isales]

Gross profit

910,000

224,000

Answer

Equity income

10,500

-

[C]

Answer

Answer

Operating expenses

(581,000)

(140,000)

[D]

Answer

Answer...

c. Complete the consolidating entries according to the

C-E-A-D-I sequence and complete the consolidation

worksheet.

Use negative signs with answers in the

Consolidated column for Cost of goods sold, Operating expenses and

Dividends.

Consolidation Worksheet

Income statement

Parent

Subsidiary

Debit

Credit

Consolidated

Sales

$3,045,000

$560,000

[Isales]

Answer

Answer

Cost of goods sold

(2,135,000)

(336,000)

[Icogs]

Answer

Answer

[Icogs]

Answer

Answer

[Isales]

Gross profit

910,000

224,000

Answer

Equity income

10,500

-

[C]

Answer

Answer

Operating expenses

(581,000)

(140,000)

[D]

Answer

Answer...

Consolidation spreadsheet for continuous sale of inventory-Equity method

Consolidation spreadsheet for continuous sale of inventory-Equity method Assume a parent company acquired a subsidiary on January 1. 2016. The purchase price was S600,000 in excess of the subsidiary's book value of Stockholders' Equity on the acquisition date, and that excess was assigned to the following AAP assets: The AAP assets with a definite useful life have been amortized as part of the parent's equity method accounting. The Goodwill asset has been tested annually for impairment, and has not been found to...

Consolidation spreadsheet for continuous sale of inventory-Equity method Assume a parent company acquired a subsidiary on January 1. 2016. The purchase price was S600,000 in excess of the subsidiary's book value of Stockholders' Equity on the acquisition date, and that excess was assigned to the following AAP assets: The AAP assets with a definite useful life have been amortized as part of the parent's equity method accounting. The Goodwill asset has been tested annually for impairment, and has not been found to...

Prepare consolidation spreadsheet for intercompany sale of equipment - Equity method Assume a parent company acquired...

Prepare consolidation spreadsheet for intercompany sale

of equipment - Equity method

Assume a parent company acquired its subsidiary on January 1, 2015,

at a purchase price that was $222,000 in excess of the book value

of the subsidiary’s Stockholders’ Equity on the acquisition date.

Of that excess, $132,000 was assigned to a Customer List that is

being amortized over a 10-year period. The remaining $90,000 was

assigned to Goodwill.

In January of 2018, the wholly owned subsidiary sold Equipment

to...

Prepare consolidation spreadsheet for intercompany sale

of equipment - Equity method

Assume a parent company acquired its subsidiary on January 1, 2015,

at a purchase price that was $222,000 in excess of the book value

of the subsidiary’s Stockholders’ Equity on the acquisition date.

Of that excess, $132,000 was assigned to a Customer List that is

being amortized over a 10-year period. The remaining $90,000 was

assigned to Goodwill.

In January of 2018, the wholly owned subsidiary sold Equipment

to...

Consolidation subsequent to date of acquisition - Equity method with noncontrolling interest and ...

Consolidation subsequent to date of acquisition - Equity method with noncontrolling interest and AAP Assume that, on January 1, 2009, a parent company acquired an 80% interest in its subsidiary. The total fair value of the controlling and noncontrolling interests was $500,000 over the book value of the subsidiary’s Stockholders’ Equity on the acquisition date. The parent assigned the excess to the following [A] assets: [A] Asset Initial Fair Value Useful Life (years) [A] Asset Initial Fair Value Useful Life...

Prepare consolidation spreadsheet for intercompany sale of land - Equity Method Assume a parent company acquired...

Prepare consolidation spreadsheet for intercompany sale of land - Equity Method Assume a parent company acquired its subsidiary on January 1, 2017, at a purchase price that was $270,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. Of that excess, $180,000 was assigned to an unrecorded patent owned by the subsidiary that is being amortized over a 10 year period. The [A] Patent asset has been amortized as part of the parent's equity...

Use negative signs with answers in the Consolidated column for Cost of goods sold, Operating expenses...

Use negative signs with answers in the

Consolidated column for Cost of goods sold, Operating expenses and

Dividends.

Parent Subsidiary Subsidiary Balance sheet $800,000 Assets (480,000) Cash 320,000 Accounts receivable Parent Income statement Sales $4,350,000 Cost of goods sold (3,050,000) Gross profit 1,300,000 Income (loss) from subsidiary 15,000 Operating expenses (830,000) Net income $485,000 Statement of retained earnings BOY retained earnings | $2,000,000 Net income 485,000 Dividends (125,000) Ending retained earnings $2,360,000 - Inventory (200,000) Equity investment $120,000 Property, plant...

Use negative signs with answers in the

Consolidated column for Cost of goods sold, Operating expenses and

Dividends.

Parent Subsidiary Subsidiary Balance sheet $800,000 Assets (480,000) Cash 320,000 Accounts receivable Parent Income statement Sales $4,350,000 Cost of goods sold (3,050,000) Gross profit 1,300,000 Income (loss) from subsidiary 15,000 Operating expenses (830,000) Net income $485,000 Statement of retained earnings BOY retained earnings | $2,000,000 Net income 485,000 Dividends (125,000) Ending retained earnings $2,360,000 - Inventory (200,000) Equity investment $120,000 Property, plant...

200 Chapter 41 Consolidated PROBLEMS base price was date, and that was LO 19. Consolidation spreadsheet...

200 Chapter 41 Consolidated PROBLEMS base price was date, and that was LO 19. Consolidation spreadsheet for continuous cale of inventory-Equity method Assume a parent company acquired a subsidiary on January 1, 2016. The purchas i n excess of the subsidiary's book value of Stockholders' Equity on the acquisition was assigned to the following AAP assets: X Original Amount Original Use Line . $120.000 210.000 150.000 120,000 $600,000 AAP Asset Property, plant and equipment (PPE), net . Customer list... Royalty...

200 Chapter 41 Consolidated PROBLEMS base price was date, and that was LO 19. Consolidation spreadsheet for continuous cale of inventory-Equity method Assume a parent company acquired a subsidiary on January 1, 2016. The purchas i n excess of the subsidiary's book value of Stockholders' Equity on the acquisition was assigned to the following AAP assets: X Original Amount Original Use Line . $120.000 210.000 150.000 120,000 $600,000 AAP Asset Property, plant and equipment (PPE), net . Customer list... Royalty...

Prepare consolidation spreadsheet for intercompany sale of equipment- Equity Method Assume a parent company acquired its...

Prepare consolidation spreadsheet for intercompany sale of equipment- Equity Method Assume a parent company acquired its subsidiary on January 1, 2015, at a purchase price that was $222,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. Of that excess, $132,000 was assigned to a Customer List that is being amortized over a 10-year period. The remaining $90,000 was assigned to Goodwill. In January of 2018, the wholly owned subsidiary sold Equipment to the...

Inferring consolidation entries from consolidated financial statements—Cost method Assume a parent company acquired a subsidiary on...

Inferring consolidation entries from consolidated financial statements—Cost method Assume a parent company acquired a subsidiary on January 1, 2012. The purchase price was $1,312,000 in excess of the subsidiary’s book value of Stockholders’ Equity on the acquisition date, and that excess was assigned to the following [A] assets: [A] Asset Original Amount Original Useful Life Property, plant and equipment (PPE), net $300,000 20 years Patent 432,000 12 years Goodwill 580,000 Indefinite $1,312,000 The parent company uses the cost method of...

Prepare consolidation spreadsheet for intercompany sale of land - Equity method Assume that a parent company acquired its subsidiary on January 1, 2014, at a purchase price that was $300,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. Of that excess, $200,000 was assigned to an unrecorded Patent owned by the subsidiary that is being amortized over a 10-year period. The [A] Patent asset has been amortized as part of the parent's equity...

Prepare consolidation spreadsheet for intercompany sale of land - Equity method Assume that a parent company acquired its subsidiary on January 1, 2014, at a purchase price that was $300,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. Of that excess, $200,000 was assigned to an unrecorded Patent owned by the subsidiary that is being amortized over a 10-year period. The [A] Patent asset has been amortized as part of the parent's equity...

c. Complete the consolidating entries according to the

C-E-A-D-I sequence and complete the consolidation

worksheet.

Use negative signs with answers in the

Consolidated column for Cost of goods sold, Operating expenses and

Dividends.

Consolidation Worksheet

Income statement

Parent

Subsidiary

Debit

Credit

Consolidated

Sales

$3,045,000

$560,000

[Isales]

Answer

Answer

Cost of goods sold

(2,135,000)

(336,000)

[Icogs]

Answer

Answer

[Icogs]

Answer

Answer

[Isales]

Gross profit

910,000

224,000

Answer

Equity income

10,500

-

[C]

Answer

Answer

Operating expenses

(581,000)

(140,000)

[D]

Answer

Answer...

c. Complete the consolidating entries according to the

C-E-A-D-I sequence and complete the consolidation

worksheet.

Use negative signs with answers in the

Consolidated column for Cost of goods sold, Operating expenses and

Dividends.

Consolidation Worksheet

Income statement

Parent

Subsidiary

Debit

Credit

Consolidated

Sales

$3,045,000

$560,000

[Isales]

Answer

Answer

Cost of goods sold

(2,135,000)

(336,000)

[Icogs]

Answer

Answer

[Icogs]

Answer

Answer

[Isales]

Gross profit

910,000

224,000

Answer

Equity income

10,500

-

[C]

Answer

Answer

Operating expenses

(581,000)

(140,000)

[D]

Answer

Answer...

Prepare consolidation spreadsheet for intercompany sale

of equipment - Equity method

Assume a parent company acquired its subsidiary on January 1, 2015,

at a purchase price that was $222,000 in excess of the book value

of the subsidiary’s Stockholders’ Equity on the acquisition date.

Of that excess, $132,000 was assigned to a Customer List that is

being amortized over a 10-year period. The remaining $90,000 was

assigned to Goodwill.

In January of 2018, the wholly owned subsidiary sold Equipment

to...

Prepare consolidation spreadsheet for intercompany sale

of equipment - Equity method

Assume a parent company acquired its subsidiary on January 1, 2015,

at a purchase price that was $222,000 in excess of the book value

of the subsidiary’s Stockholders’ Equity on the acquisition date.

Of that excess, $132,000 was assigned to a Customer List that is

being amortized over a 10-year period. The remaining $90,000 was

assigned to Goodwill.

In January of 2018, the wholly owned subsidiary sold Equipment

to...

Use negative signs with answers in the

Consolidated column for Cost of goods sold, Operating expenses and

Dividends.

Parent Subsidiary Subsidiary Balance sheet $800,000 Assets (480,000) Cash 320,000 Accounts receivable Parent Income statement Sales $4,350,000 Cost of goods sold (3,050,000) Gross profit 1,300,000 Income (loss) from subsidiary 15,000 Operating expenses (830,000) Net income $485,000 Statement of retained earnings BOY retained earnings | $2,000,000 Net income 485,000 Dividends (125,000) Ending retained earnings $2,360,000 - Inventory (200,000) Equity investment $120,000 Property, plant...

Use negative signs with answers in the

Consolidated column for Cost of goods sold, Operating expenses and

Dividends.

Parent Subsidiary Subsidiary Balance sheet $800,000 Assets (480,000) Cash 320,000 Accounts receivable Parent Income statement Sales $4,350,000 Cost of goods sold (3,050,000) Gross profit 1,300,000 Income (loss) from subsidiary 15,000 Operating expenses (830,000) Net income $485,000 Statement of retained earnings BOY retained earnings | $2,000,000 Net income 485,000 Dividends (125,000) Ending retained earnings $2,360,000 - Inventory (200,000) Equity investment $120,000 Property, plant...

200 Chapter 41 Consolidated PROBLEMS base price was date, and that was LO 19. Consolidation spreadsheet for continuous cale of inventory-Equity method Assume a parent company acquired a subsidiary on January 1, 2016. The purchas i n excess of the subsidiary's book value of Stockholders' Equity on the acquisition was assigned to the following AAP assets: X Original Amount Original Use Line . $120.000 210.000 150.000 120,000 $600,000 AAP Asset Property, plant and equipment (PPE), net . Customer list... Royalty...

200 Chapter 41 Consolidated PROBLEMS base price was date, and that was LO 19. Consolidation spreadsheet for continuous cale of inventory-Equity method Assume a parent company acquired a subsidiary on January 1, 2016. The purchas i n excess of the subsidiary's book value of Stockholders' Equity on the acquisition was assigned to the following AAP assets: X Original Amount Original Use Line . $120.000 210.000 150.000 120,000 $600,000 AAP Asset Property, plant and equipment (PPE), net . Customer list... Royalty...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago