y is output, pi is inflation, pi^e is expected inflation, i is interest rate

Homework Answers

a)

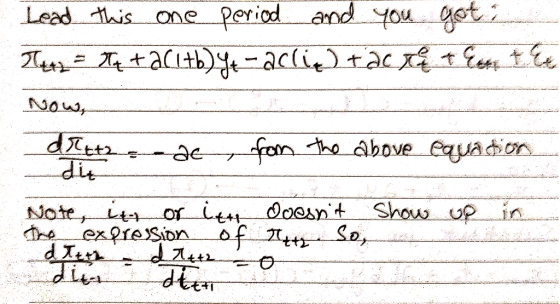

You can show this by showing that t period interest rate only t+2 period inflation. It doesn't influence t period or t+1 period inflation.

This way you show that t period inflation doesn't influence any t+i period inflation for i not equal to 2.

Now, we can write the Loss function as follows (by just opening the bracket):

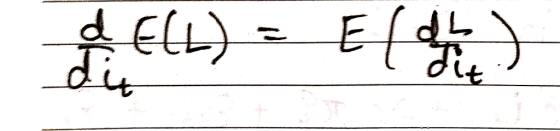

To minimize, you'll have to differentiate the loss function with respect to t period interest rate. By properties of expectations, you have:

To get your final result, just differentiate the loss function.

Notice something. The derivative all other terms except the one that has t+2 period inflation, when differentiated with respect to t period interest rate, become 0. So whether you minimize the whole loss function, or whether you minimize only that term of the loss function that has t+2 period inflation, it won't make a difference. Your final result will be the same. Hence, you can write the optimization problem with just the term corresponding to t+2 period inflation (as has been written in part a of the question).

b) The optimal interest rate ensures that

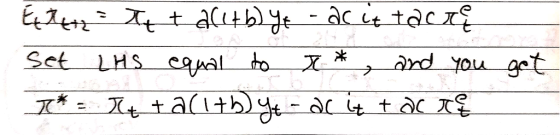

Now, look at the final solution for t+2 period inflation in part a. You had:

Take expectations on both sides, and you'll get:

A central bank knows all the all the terms in the RHS of the

expression for interest rate. This is because we've taken t period

expectations- that means they used all the information available

with them as of the end of period t. They know the actual inflation

at time t:

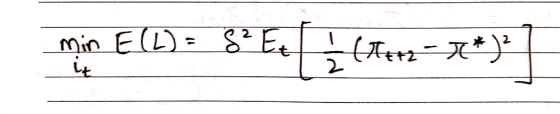

c) From part a) you found that the optimization problem can be written as follows:

Now just use basic calculus to minimize this expression with respect to t period interest rate.

The final expression shows that the solution to the optimization problem requires that the two period ahead forecast of inflation equal the inflation target.

Add Answer to:

y is output, pi is inflation, pi^e is expected inflation, i is interest rate Consider the dynamic IS-AS model presented by Svensson (1999) where all the symbols have the usual meaning. The monetar...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago