Homework Answers

27.00%

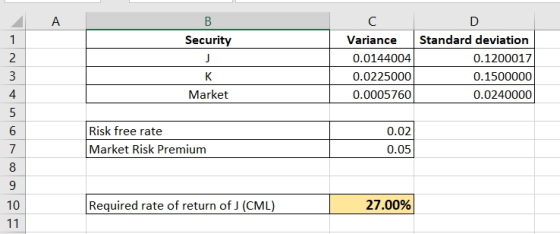

Required return under Capital market line:

Please refer to below spreadsheet for calculation and answer. Cell reference also provided.

Cell reference -

Hope this will help, please do comment if you need any further explanation. Your feedback would be highly appreciated.

Add Answer to:

JUS You are given the following correlation matrix for Securities J. K. and the Market: Correlation Security Securi...

Question 7 5 pts You are given the following information for Securities J and K for...

Question 7 5 pts You are given the following information for Securities J and K for the coming year: State of Nature Probability 20.00% 50.00% 30.00% Return J 14.00% 19.00% 16.00% Return K 14.00% 16.00% 25.00% You create a portfolio, with 40 percent of your money invested in Security K. and the rest of your money invested in Security J. Given this information, determine the coefficient of variation (CV) of this portfolio for the coming year. Enter your answer with...

Question 7 5 pts You are given the following information for Securities J and K for the coming year: State of Nature Probability 20.00% 50.00% 30.00% Return J 14.00% 19.00% 16.00% Return K 14.00% 16.00% 25.00% You create a portfolio, with 40 percent of your money invested in Security K. and the rest of your money invested in Security J. Given this information, determine the coefficient of variation (CV) of this portfolio for the coming year. Enter your answer with...

Question 3 Suppose you observe the following market data on debt securities: Security Coupon (p.a.) Yield...

Question 3 Suppose you observe the following market data on debt securities: Security Coupon (p.a.) Yield to maturity (p.a. continuously compounded) n.a. 2.00% 6-month Treasury Bond 1-year NZ Government Stock 10%, semi-annual 4.00% Note: Data deviates from the current market conditions as it simplifies the calculations. Required: (a) What are the continuously compounded zero-coupon yields for 6 months and one year, respectively? Report your answer in percentage (%) with 4 dps. (4 marks) (b) What is the duration of the...

Question 3 Suppose you observe the following market data on debt securities: Security Coupon (p.a.) Yield to maturity (p.a. continuously compounded) n.a. 2.00% 6-month Treasury Bond 1-year NZ Government Stock 10%, semi-annual 4.00% Note: Data deviates from the current market conditions as it simplifies the calculations. Required: (a) What are the continuously compounded zero-coupon yields for 6 months and one year, respectively? Report your answer in percentage (%) with 4 dps. (4 marks) (b) What is the duration of the...

You have been provided the following data about the securities of three firms, the market portfolio,...

You have been provided the following data about the securities

of three firms, the market portfolio, and the risk-free asset:

a. Fill in the missing values in the table. (Leave no cells

blank - be certain to enter 0 wherever required. Do not round

intermediate calculations and round your answers to 2 decimal

places, e.g., 32.16.)

b-1. What is the expected return of Firm A? (Do not round

intermediate calculations and enter your answer as a percent

rounded to 2...

You have been provided the following data about the securities

of three firms, the market portfolio, and the risk-free asset:

a. Fill in the missing values in the table. (Leave no cells

blank - be certain to enter 0 wherever required. Do not round

intermediate calculations and round your answers to 2 decimal

places, e.g., 32.16.)

b-1. What is the expected return of Firm A? (Do not round

intermediate calculations and enter your answer as a percent

rounded to 2...

Question 7 5 pts You are given the following information for Securities J and K for the coming year: State of Nature Probability 20.00% 50.00% 30.00% Return J 14.00% 19.00% 16.00% Return K 14.00% 16.00% 25.00% You create a portfolio, with 40 percent of your money invested in Security K. and the rest of your money invested in Security J. Given this information, determine the coefficient of variation (CV) of this portfolio for the coming year. Enter your answer with...

Question 7 5 pts You are given the following information for Securities J and K for the coming year: State of Nature Probability 20.00% 50.00% 30.00% Return J 14.00% 19.00% 16.00% Return K 14.00% 16.00% 25.00% You create a portfolio, with 40 percent of your money invested in Security K. and the rest of your money invested in Security J. Given this information, determine the coefficient of variation (CV) of this portfolio for the coming year. Enter your answer with...

Question 3 Suppose you observe the following market data on debt securities: Security Coupon (p.a.) Yield to maturity (p.a. continuously compounded) n.a. 2.00% 6-month Treasury Bond 1-year NZ Government Stock 10%, semi-annual 4.00% Note: Data deviates from the current market conditions as it simplifies the calculations. Required: (a) What are the continuously compounded zero-coupon yields for 6 months and one year, respectively? Report your answer in percentage (%) with 4 dps. (4 marks) (b) What is the duration of the...

Question 3 Suppose you observe the following market data on debt securities: Security Coupon (p.a.) Yield to maturity (p.a. continuously compounded) n.a. 2.00% 6-month Treasury Bond 1-year NZ Government Stock 10%, semi-annual 4.00% Note: Data deviates from the current market conditions as it simplifies the calculations. Required: (a) What are the continuously compounded zero-coupon yields for 6 months and one year, respectively? Report your answer in percentage (%) with 4 dps. (4 marks) (b) What is the duration of the...

You have been provided the following data about the securities

of three firms, the market portfolio, and the risk-free asset:

a. Fill in the missing values in the table. (Leave no cells

blank - be certain to enter 0 wherever required. Do not round

intermediate calculations and round your answers to 2 decimal

places, e.g., 32.16.)

b-1. What is the expected return of Firm A? (Do not round

intermediate calculations and enter your answer as a percent

rounded to 2...

You have been provided the following data about the securities

of three firms, the market portfolio, and the risk-free asset:

a. Fill in the missing values in the table. (Leave no cells

blank - be certain to enter 0 wherever required. Do not round

intermediate calculations and round your answers to 2 decimal

places, e.g., 32.16.)

b-1. What is the expected return of Firm A? (Do not round

intermediate calculations and enter your answer as a percent

rounded to 2...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago