Payoffs of strategies. Draw the payoffs for these strategies. All derivatives are on the same stock....

Homework Answers

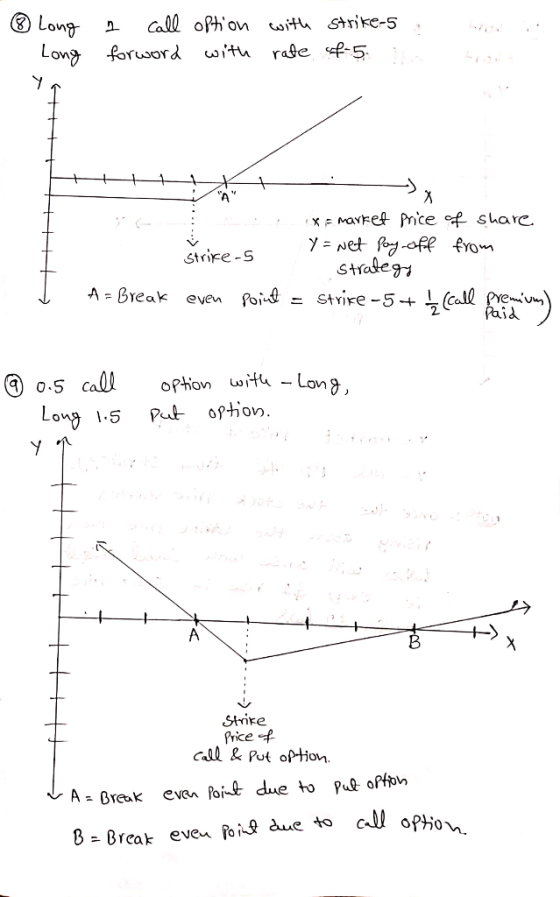

please refer above posted

images for graphs

please refer above posted

images for graphs

And hear we take an assumption that

Strike 1 < strike 2 < strike 3

Add Answer to:

Payoffs of strategies. Draw the payoffs for these strategies. All derivatives are on the same stock....

The goal of this project is to examine option trading strategies. The project requires you to...

The goal of this project is to examine option trading strategies. The project requires you to work in Excel with the provided spreadsheet. A) Bull Spread Payoff Long call option K1 = Short call option K2 = Stock Price (ST) Total Payoff $0.00 $5.00 $10.00 $15.00 $20.00 $25.00 $30.00 $35.00 $40.00 $45.00 $50.00 $55.00 $60.00 A) Consider buying a call option with a strike of $20 and a selling call option with strike of $30. Fill in the table for...

A 1-year European put option on a stock with strike price of $50 is quoted as...

A 1-year European put option on a stock with strike price of $50 is quoted as $7; a 1-year European call option on the same stock with strike price $30 is quoted as $5. Suppose you long one put and short one call (one option is on 100 share). a) Draw the payoff diagram for your put position and call position. (5 points) b) After 1-year, stock price turns out to be $45. What is your total payoff? What is...

Suppose you buy 100 shares of Google stock which has a current price of $1,265.13 a...

Suppose you buy 100 shares of Google stock which has a current price of $1,265.13 a share. You want to ensure that you do not lose more than $200 a share. Which of the following option strategies would allow you to do this? A. A covered call B. A naked call C. A protective put D. You cannot ensure that you will not have losses with stocks Suppose I buy 100 shares of AMD and want to limit my losses...

Assume the following premia: Strike $950 Call $120.405 93.809 84.470 71.802 51.873 Put $51.777 74.201 1000...

Assume the following premia: Strike $950 Call $120.405 93.809 84.470 71.802 51.873 Put $51.777 74.201 1000 1020 84.470 101.214 1050 1107 137.167 I 1) Suppose you invest in the S&P stock index for $1000, buy a 950-strike put, and sell a 1050- strike call. Draw a profit diagram for this position. What is the net option premium? 2) Here is a quote from an investment website about an investment strategy using options: One strategy investors apply is a "synthetic stock."...

Assume the following premia: Strike $950 Call $120.405 93.809 84.470 71.802 51.873 Put $51.777 74.201 1000 1020 84.470 101.214 1050 1107 137.167 I 1) Suppose you invest in the S&P stock index for $1000, buy a 950-strike put, and sell a 1050- strike call. Draw a profit diagram for this position. What is the net option premium? 2) Here is a quote from an investment website about an investment strategy using options: One strategy investors apply is a "synthetic stock."...

Problem 1: Portfolio of Options Draw the resulting payoff from the following combination of options. Make...

Problem 1: Portfolio of Options Draw the resulting payoff from the following combination of options. Make sure that you specify the coordinates of the payoff (x,y) at the intercept and at every strike price. a. 1 long call with strike price 10 and 1 short call with strike price 12. b. 1 short put with strike price 5 and one long put with strike price 9. c. 1 long call with strike price 10 and 2 short call with strike...

5. A call option on Company B common stock is worth $8 with 7 months before...

5. A call option on Company B common stock is worth $8 with 7 months before expiration. The strike price on the call is $40 and the price per share is currently trading at $44 per share. The put option at the same exercise price is worth $1.50. a. Is the call option in or out or the money? b. Is the put option in or out of the money? c. At what extra above expiration value is the call...

1. Draw payoff diagrams for the following option trading strategies. Assume all options have the same...

1. Draw payoff diagrams for the following option trading strategies. Assume all options have the same expiration date. a. Buy a share and write a call on the stock b. Buy a call with exercise price X1 and write a call with an exercise price X2 on the same stock, with X1 < X2. c. Buy a call with exercise price X1, sell two calls with exercise price X2 and buy a call with exercise price X3 with X1 X2...

1. Draw payoff diagrams for the following option trading strategies. Assume all options have the same expiration date. a. Buy a share and write a call on the stock b. Buy a call with exercise price X1 and write a call with an exercise price X2 on the same stock, with X1 < X2. c. Buy a call with exercise price X1, sell two calls with exercise price X2 and buy a call with exercise price X3 with X1 X2...

Assume that we have the following derivatives portfolio: A long futures contract on stock A, with...

Assume that we have the following derivatives portfolio: A long futures contract on stock A, with strike price 82 and a long put option contract on the same stock, with the same strike price. The option's premium is 8 and is payed today. The risk free rate of interest is 5%, and the time of expiration is 1 year. What will be the present value profit for the above derivatives portfolio if the stock's spot price is 109 at the...

1. (Put-call parity) A stock currently costs So per share. In each time period, the value...

1. (Put-call parity) A stock currently costs So per share. In each time period, the value of the stock will either increase or decrease by u and d respectively, and the risk-free interest rate is r. Let Sn be the price of the stock at t n, for O < n < V, and consider three derivatives which expire at t- N, a call option Vall-(SN-K)+, a put option Vpul-(K-Sy)+, ad a forward contract Fv -SN -K (a) The forward...

1. (Put-call parity) A stock currently costs So per share. In each time period, the value of the stock will either increase or decrease by u and d respectively, and the risk-free interest rate is r. Let Sn be the price of the stock at t n, for O < n < V, and consider three derivatives which expire at t- N, a call option Vall-(SN-K)+, a put option Vpul-(K-Sy)+, ad a forward contract Fv -SN -K (a) The forward...

g) European call with a strike price of $40 costs $7. European put with the same...

g) European call with a strike price of $40 costs $7. European put with the same strike price and expiration date costs $6. Assume that you buy two calls and one put (strap strategy). Sketch the graph and write down functions of payoff and profit h) Consider a stock with a price of $50 and there is European put option on that stock with the strike of $55 and premium of $4. Assume that you buy 1/3 of a stock...

g) European call with a strike price of $40 costs $7. European put with the same strike price and expiration date costs $6. Assume that you buy two calls and one put (strap strategy). Sketch the graph and write down functions of payoff and profit h) Consider a stock with a price of $50 and there is European put option on that stock with the strike of $55 and premium of $4. Assume that you buy 1/3 of a stock...

Assume the following premia: Strike $950 Call $120.405 93.809 84.470 71.802 51.873 Put $51.777 74.201 1000 1020 84.470 101.214 1050 1107 137.167 I 1) Suppose you invest in the S&P stock index for $1000, buy a 950-strike put, and sell a 1050- strike call. Draw a profit diagram for this position. What is the net option premium? 2) Here is a quote from an investment website about an investment strategy using options: One strategy investors apply is a "synthetic stock."...

Assume the following premia: Strike $950 Call $120.405 93.809 84.470 71.802 51.873 Put $51.777 74.201 1000 1020 84.470 101.214 1050 1107 137.167 I 1) Suppose you invest in the S&P stock index for $1000, buy a 950-strike put, and sell a 1050- strike call. Draw a profit diagram for this position. What is the net option premium? 2) Here is a quote from an investment website about an investment strategy using options: One strategy investors apply is a "synthetic stock."...

1. Draw payoff diagrams for the following option trading strategies. Assume all options have the same expiration date. a. Buy a share and write a call on the stock b. Buy a call with exercise price X1 and write a call with an exercise price X2 on the same stock, with X1 < X2. c. Buy a call with exercise price X1, sell two calls with exercise price X2 and buy a call with exercise price X3 with X1 X2...

1. Draw payoff diagrams for the following option trading strategies. Assume all options have the same expiration date. a. Buy a share and write a call on the stock b. Buy a call with exercise price X1 and write a call with an exercise price X2 on the same stock, with X1 < X2. c. Buy a call with exercise price X1, sell two calls with exercise price X2 and buy a call with exercise price X3 with X1 X2...

1. (Put-call parity) A stock currently costs So per share. In each time period, the value of the stock will either increase or decrease by u and d respectively, and the risk-free interest rate is r. Let Sn be the price of the stock at t n, for O < n < V, and consider three derivatives which expire at t- N, a call option Vall-(SN-K)+, a put option Vpul-(K-Sy)+, ad a forward contract Fv -SN -K (a) The forward...

1. (Put-call parity) A stock currently costs So per share. In each time period, the value of the stock will either increase or decrease by u and d respectively, and the risk-free interest rate is r. Let Sn be the price of the stock at t n, for O < n < V, and consider three derivatives which expire at t- N, a call option Vall-(SN-K)+, a put option Vpul-(K-Sy)+, ad a forward contract Fv -SN -K (a) The forward...

g) European call with a strike price of $40 costs $7. European put with the same strike price and expiration date costs $6. Assume that you buy two calls and one put (strap strategy). Sketch the graph and write down functions of payoff and profit h) Consider a stock with a price of $50 and there is European put option on that stock with the strike of $55 and premium of $4. Assume that you buy 1/3 of a stock...

g) European call with a strike price of $40 costs $7. European put with the same strike price and expiration date costs $6. Assume that you buy two calls and one put (strap strategy). Sketch the graph and write down functions of payoff and profit h) Consider a stock with a price of $50 and there is European put option on that stock with the strike of $55 and premium of $4. Assume that you buy 1/3 of a stock...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago