The following information is taken from the accounts of Latta Company. The entries in the T-accounts...

|

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. |

| Manufacturing Overhead | Work in Process | |||

|

(a) 460,000 |

(b) 390,000 |

Bal. 15,000 |

(c) 710,000 |

|||

| 260,000 | ||||||

|

Bal. 70,000 |

85,000 |

|||||

|

(b) 390,000 |

||||||

|

Bal. 40,000 |

| Finished Goods | Cost of Goods Sold | |||

|

Bal. 50,000 |

(d) 640,000 |

(d) 640,000 |

|

|||

|

(c) 710,000 |

|

|||||

|

Bal. 120,000 |

|

|

The overhead that had been applied to production during the year is distributed among the ending balances in the accounts as follows: |

| Work in process, ending | $ | 19,500 |

| Finished goods, ending | 58,500 | |

| Cost of goods Sold | 312,000 | |

| Overhead applied | $ | 390,000 |

|

For example, of the $40,000 ending balance in work in process, $19,500 was overhead that had been applied during the year. |

| Required: | |

| 1. | Identify the reasons for entries (a) through (d). |

| 2. |

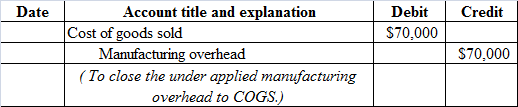

Assume that the company closes any balance in the manufacturing overhead account directly to cost of goods sold. Prepare the necessary journal entry. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.) |

| 3. |

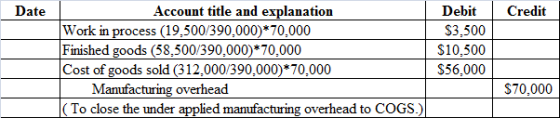

Assume instead that the company allocates any balance in the manufacturing overhead account to the other accounts in proportion to the overhead applied during the year that is in the ending balance in each account. Prepare the necessary journal entry. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field. Do not round intermediate calculations.) |

Homework Answers

Accounting: Accounting is the process of recording the transactions, classifying it in the specific manner and further the process of summarising and, analysing is done and thus the results are interpreted. It is the process of preserving the accounts.

Transaction: Transaction is an act of buying or selling goods or rendering any service that is reliably measured in terms of money.

Journal entry: Journal entry is the recording of transactions in a systematic manner as they occur. Thus it is a summary of all transactions which has debit and credit aspects recorded chronologically.

Overheads: Overheads are the indirect expenses borne by the company. The types of overheads are Factory overheads, office and administration overheads and selling and distribution overheads.

Work in Process: Work in process is the partially completed units. It is in the stage before completion.

Manufacturing Overhead: Manufacturing overheads are the overheads related to the manufacturing of product. They are the indirect expenses during manufacturing.

Finished goods: Finished goods are the goods completed and being ready for sale. They are the stock and regarded as current assets of the company.

Cost of Goods Sold: Cost of Goods Sold is the cost that is directly incurred for the sale of goods. It includes cost such as travelling expenses during the time of sale, salesmen remuneration, etc. It is also known as cost of sales.

Rules for debit and credit

When asset increases debit it; asset decreases credit it.

When liabilities increases credit it; liabilities decreases debit it.

When stockholders’ equity increases credit it; stockholders’ equity decreases debit it.

Expenses and losses increases debit it; expenses and losses decreases credit it.

Incomes and gains increases credit it; incomes and gains decreases debit it

(1.a)

Entry (a) denotes the actual manufacturing overhead cost for the period and it is the balance brought down during the period.

(1.b)

The balance of $390,000 represents the actual manufacturing cost applied to production during the period. Thus it is credited in the manufacturing overheads account

(1.c)

The cost of completed goods is $710,000 which has been transferred to finished goods inventory from the work in process account.

(1.d)

In the cost of goods sold account it represents the finished goods inventory and it has been transferred to cost of goods sold account. It represents the cost of goods sold for the year.

(2)

Journal entry for applied manufacturing overhead

(3)

Journal entry

Working notes:

Therefore amount allocated to Work in process is $3,500

Therefore amount allocated to Cost of goods sold is $56,000

Therefore amount allocated to finished goods is $10,500

Ans: Part 1.aThe actual manufacturing overhead during the period is $460,000

Part 1.bIt represents the manufacturing overhead cost applied to production during the period.

Part 1.cIt represents the cost of goods manufactured during the year

Part 1.dIt represents the cost of finished goods inventory which has been transferred to cost of goods sold.

Part 2

Add Answer to:

The following information is taken from the accounts of Latta

Company. The entries in the T-accounts...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead (a) 481,536 (b) 401,280 Bal. 80,256 Work in Process Bal. 12,720 (c) 746,000 291,500 89,500 (b) 401,280 Bal. 49,000 Finished Goods Bal. 41,000 (d) 658,000 (c) 746,000 Bal. 129,000 Cost of Goods Sold (d) 658,000 The overhead that had been applied to production during the year is distributed among Work...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead 506,880) 422,400 Bal. 84,480 Bal. Work in Process 2,600 (c) 790,000 330,000 95,000 422,400 60,000 Bal. (e) Bal. Finished Goods 30,000 (d) 680,000 790,000 140,000 (b) Bal. es (d) Cost of Goods Sold 680,000 The overhead that had been applied to production during the year is distributed among Work in...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead 506,880) 422,400 Bal. 84,480 Bal. Work in Process 2,600 (c) 790,000 330,000 95,000 422,400 60,000 Bal. (e) Bal. Finished Goods 30,000 (d) 680,000 790,000 140,000 (b) Bal. es (d) Cost of Goods Sold 680,000 The overhead that had been applied to production during the year is distributed among Work in...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead 488,448 (b) 407,040 81,408 Bal. (a Bal. 758,000 664,000 Work in Process 9,960 (c) 302,000 91,000 407,040 52,000 Finished Goods 38,000 (d) 758,000 132,000 Bal. (C) Bal. (b) Bal. (d) Cost of Goods Sold 664,000 The overhead that had been applied to production during the year is distributed among Work...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead 488,448 (b) 407,040 81,408 Bal. (a Bal. 758,000 664,000 Work in Process 9,960 (c) 302,000 91,000 407,040 52,000 Finished Goods 38,000 (d) 758,000 132,000 Bal. (C) Bal. (b) Bal. (d) Cost of Goods Sold 664,000 The overhead that had been applied to production during the year is distributed among Work...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead Work in Process Finished Goods 479,232 b) 399,360 Bal 13.640 (e) 742,000 Bal. 42,000(d) 656,000 79,872 288.000 le) 742.000 89,000 Bal. 128,000 399,360 49,000 Cost of Goods Sold (d) 656,000 Bal. The overhead that had been applied to production during the year is distributed among Work in Process, Finished Goods,...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead Work in Process Finished Goods 479,232 b) 399,360 Bal 13.640 (e) 742,000 Bal. 42,000(d) 656,000 79,872 288.000 le) 742.000 89,000 Bal. 128,000 399,360 49,000 Cost of Goods Sold (d) 656,000 Bal. The overhead that had been applied to production during the year is distributed among Work in Process, Finished Goods,...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. 25 Manufacturing Overhead (a) 504,576 (b) 420,480 Bal. 84,096 Work in Process Finished Goods points 3,520 (c) 786,000 326,500 94,500 (b) 420,480 Bal. 59,000 Bal. 31,000 (d) 678,000 Bal 786,000 (c) Bal.139,000 еВook Cost of Goods Sold (d) 678,000 Hint The overhead that had been applied to production during the year is...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. 25 Manufacturing Overhead (a) 504,576 (b) 420,480 Bal. 84,096 Work in Process Finished Goods points 3,520 (c) 786,000 326,500 94,500 (b) 420,480 Bal. 59,000 Bal. 31,000 (d) 678,000 Bal 786,000 (c) Bal.139,000 еВook Cost of Goods Sold (d) 678,000 Hint The overhead that had been applied to production during the year is...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead (a) 483,840 (b) 403,200 Bal. 80,640 Work in Process Bal. 11,800 (c) 750,000 295,000 90,000 (b) 403,200 Bal. 50,000 Finished Goods Bal. 40,000 (d) 660,000 (c) 750,000 Bal. 130,000 Cost of Goods Sold (d) 660,000 The overhead that had been applied to production during the year is distributed among Work...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead (a) 467,712(b) 389,760 Bal. 77,952 Bal. Work in Process 18,240 (0) 722,000 270,500 86,500 389,760 43,000 Bal. (c) Bal. Finished Goods 47,000 (d) 646,000 722,880 123,000 (b) Ral (d) Cost of Goods Sold 646,000 The overhead that had been applied to production during the year is distributed among Work in...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead (a) 467,712(b) 389,760 Bal. 77,952 Bal. Work in Process 18,240 (0) 722,000 270,500 86,500 389,760 43,000 Bal. (c) Bal. Finished Goods 47,000 (d) 646,000 722,880 123,000 (b) Ral (d) Cost of Goods Sold 646,000 The overhead that had been applied to production during the year is distributed among Work in...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead Work in Process Finished Goods 470,016 Kb) 391,680 Bal 17,320 (0) 726,000 Bal. 46,000 (d) 648,000 Bal. 78,336 274,000 (c) 726 000 87,000 Bal. 124,000 391,680 Bal. 44,000 Cost of Goods Sold (d) 648,000 The overhead that had been applied to production during the year is distributed among Work in...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead Work in Process Finished Goods 470,016 Kb) 391,680 Bal 17,320 (0) 726,000 Bal. 46,000 (d) 648,000 Bal. 78,336 274,000 (c) 726 000 87,000 Bal. 124,000 391,680 Bal. 44,000 Cost of Goods Sold (d) 648,000 The overhead that had been applied to production during the year is distributed among Work in...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead (a) 463, 104(b) 385, 920 Bal. 77, 184| Work in Process Bal. 20,080 (c) 714,000 263,500 85,500 (b) 385, 920 Bal. 41,000 Finished Goods Bal. 49,000(d) 642,000 (c) 714,000 Bal. 121,000 Cost of Goods Sold (d) 642,000 The overhead that had been applied to production during the year is distributed...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead (a) 463, 104(b) 385, 920 Bal. 77, 184| Work in Process Bal. 20,080 (c) 714,000 263,500 85,500 (b) 385, 920 Bal. 41,000 Finished Goods Bal. 49,000(d) 642,000 (c) 714,000 Bal. 121,000 Cost of Goods Sold (d) 642,000 The overhead that had been applied to production during the year is distributed...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead 497,664(b) 414,720 Bal. 82,944 (a) Bal. (b) Bal. Work in Process 6,280 (c) 774,000 316,000 93,000 414,720 56,000 Cost of Goods Sold 672,000 ces Finished Goods 34,000 (d) 672,000 774,000 136,000 Bal. (c) Bal. (d) The overhead that had been applied to production during the year is distributed among Work...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead 497,664(b) 414,720 Bal. 82,944 (a) Bal. (b) Bal. Work in Process 6,280 (c) 774,000 316,000 93,000 414,720 56,000 Cost of Goods Sold 672,000 ces Finished Goods 34,000 (d) 672,000 774,000 136,000 Bal. (c) Bal. (d) The overhead that had been applied to production during the year is distributed among Work...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead 506,880) 422,400 Bal. 84,480 Bal. Work in Process 2,600 (c) 790,000 330,000 95,000 422,400 60,000 Bal. (e) Bal. Finished Goods 30,000 (d) 680,000 790,000 140,000 (b) Bal. es (d) Cost of Goods Sold 680,000 The overhead that had been applied to production during the year is distributed among Work in...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead 506,880) 422,400 Bal. 84,480 Bal. Work in Process 2,600 (c) 790,000 330,000 95,000 422,400 60,000 Bal. (e) Bal. Finished Goods 30,000 (d) 680,000 790,000 140,000 (b) Bal. es (d) Cost of Goods Sold 680,000 The overhead that had been applied to production during the year is distributed among Work in...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead 488,448 (b) 407,040 81,408 Bal. (a Bal. 758,000 664,000 Work in Process 9,960 (c) 302,000 91,000 407,040 52,000 Finished Goods 38,000 (d) 758,000 132,000 Bal. (C) Bal. (b) Bal. (d) Cost of Goods Sold 664,000 The overhead that had been applied to production during the year is distributed among Work...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead 488,448 (b) 407,040 81,408 Bal. (a Bal. 758,000 664,000 Work in Process 9,960 (c) 302,000 91,000 407,040 52,000 Finished Goods 38,000 (d) 758,000 132,000 Bal. (C) Bal. (b) Bal. (d) Cost of Goods Sold 664,000 The overhead that had been applied to production during the year is distributed among Work...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead Work in Process Finished Goods 479,232 b) 399,360 Bal 13.640 (e) 742,000 Bal. 42,000(d) 656,000 79,872 288.000 le) 742.000 89,000 Bal. 128,000 399,360 49,000 Cost of Goods Sold (d) 656,000 Bal. The overhead that had been applied to production during the year is distributed among Work in Process, Finished Goods,...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead Work in Process Finished Goods 479,232 b) 399,360 Bal 13.640 (e) 742,000 Bal. 42,000(d) 656,000 79,872 288.000 le) 742.000 89,000 Bal. 128,000 399,360 49,000 Cost of Goods Sold (d) 656,000 Bal. The overhead that had been applied to production during the year is distributed among Work in Process, Finished Goods,...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. 25 Manufacturing Overhead (a) 504,576 (b) 420,480 Bal. 84,096 Work in Process Finished Goods points 3,520 (c) 786,000 326,500 94,500 (b) 420,480 Bal. 59,000 Bal. 31,000 (d) 678,000 Bal 786,000 (c) Bal.139,000 еВook Cost of Goods Sold (d) 678,000 Hint The overhead that had been applied to production during the year is...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. 25 Manufacturing Overhead (a) 504,576 (b) 420,480 Bal. 84,096 Work in Process Finished Goods points 3,520 (c) 786,000 326,500 94,500 (b) 420,480 Bal. 59,000 Bal. 31,000 (d) 678,000 Bal 786,000 (c) Bal.139,000 еВook Cost of Goods Sold (d) 678,000 Hint The overhead that had been applied to production during the year is...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead (a) 467,712(b) 389,760 Bal. 77,952 Bal. Work in Process 18,240 (0) 722,000 270,500 86,500 389,760 43,000 Bal. (c) Bal. Finished Goods 47,000 (d) 646,000 722,880 123,000 (b) Ral (d) Cost of Goods Sold 646,000 The overhead that had been applied to production during the year is distributed among Work in...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead (a) 467,712(b) 389,760 Bal. 77,952 Bal. Work in Process 18,240 (0) 722,000 270,500 86,500 389,760 43,000 Bal. (c) Bal. Finished Goods 47,000 (d) 646,000 722,880 123,000 (b) Ral (d) Cost of Goods Sold 646,000 The overhead that had been applied to production during the year is distributed among Work in...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead Work in Process Finished Goods 470,016 Kb) 391,680 Bal 17,320 (0) 726,000 Bal. 46,000 (d) 648,000 Bal. 78,336 274,000 (c) 726 000 87,000 Bal. 124,000 391,680 Bal. 44,000 Cost of Goods Sold (d) 648,000 The overhead that had been applied to production during the year is distributed among Work in...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead Work in Process Finished Goods 470,016 Kb) 391,680 Bal 17,320 (0) 726,000 Bal. 46,000 (d) 648,000 Bal. 78,336 274,000 (c) 726 000 87,000 Bal. 124,000 391,680 Bal. 44,000 Cost of Goods Sold (d) 648,000 The overhead that had been applied to production during the year is distributed among Work in...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead (a) 463, 104(b) 385, 920 Bal. 77, 184| Work in Process Bal. 20,080 (c) 714,000 263,500 85,500 (b) 385, 920 Bal. 41,000 Finished Goods Bal. 49,000(d) 642,000 (c) 714,000 Bal. 121,000 Cost of Goods Sold (d) 642,000 The overhead that had been applied to production during the year is distributed...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead (a) 463, 104(b) 385, 920 Bal. 77, 184| Work in Process Bal. 20,080 (c) 714,000 263,500 85,500 (b) 385, 920 Bal. 41,000 Finished Goods Bal. 49,000(d) 642,000 (c) 714,000 Bal. 121,000 Cost of Goods Sold (d) 642,000 The overhead that had been applied to production during the year is distributed...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead 497,664(b) 414,720 Bal. 82,944 (a) Bal. (b) Bal. Work in Process 6,280 (c) 774,000 316,000 93,000 414,720 56,000 Cost of Goods Sold 672,000 ces Finished Goods 34,000 (d) 672,000 774,000 136,000 Bal. (c) Bal. (d) The overhead that had been applied to production during the year is distributed among Work...

The following information is taken from the accounts of Latta Company. The entries in the T-accounts are summaries of the transactions that affected those accounts during the year. Manufacturing Overhead 497,664(b) 414,720 Bal. 82,944 (a) Bal. (b) Bal. Work in Process 6,280 (c) 774,000 316,000 93,000 414,720 56,000 Cost of Goods Sold 672,000 ces Finished Goods 34,000 (d) 672,000 774,000 136,000 Bal. (c) Bal. (d) The overhead that had been applied to production during the year is distributed among Work...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago