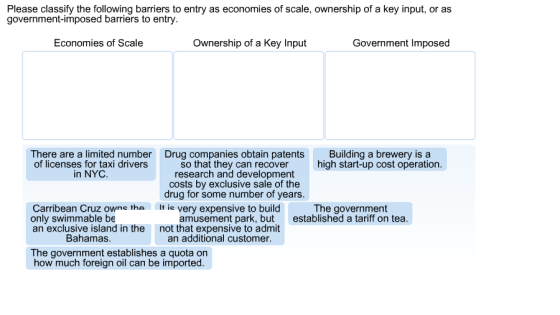

Please classify the following barriers to entry as economies of scale, ownership of a key input,...

Please classify the following barriers to entry as economies of

scale, ownership of a key input, or as government-imposed barriers

to entry.

Homework Answers

Add Answer to:

Please classify the following barriers to entry as economies of

scale, ownership of a key input,...

There are several types of barriers to entry that can create a monopoly. Which of the...

There are several types of barriers to entry that can create a monopoly. Which of the following barriers is the result of government action? a. network externalities b. control of a key resource c. economies of scale d. public franchise

Which of the following are common barriers to entry in a market that has a monopoly?...

Which of the following are common barriers to entry in a market that has a monopoly? Choose one or more: A. A monopolist could enjoy the benefits of a government-imposed barrier.B. A monopolist could charge a higher price than potential competitorsC. A monopolist could enjoy economies of scale. D. A monopolist could control a vital resource.

Which of the following is not a barrier to entry? Government intervention Economies of scale The...

Which of the following is not a barrier to entry? Government intervention Economies of scale The price elasticity of demand Scarce resources Aggressive business tactics Which of the following is is not an example of a barrier to entry that would lead to monopoly power? The government grants a copyright to the author of a book. Firms cannot enter industries in the short run, so there may be a single firm in the industry. To produce oil, a firm must...

What do patents, economies of scale, and exclusive franchises have in common? All three of the...

What do patents, economies of scale, and exclusive franchises have in common? All three of the other answers are correct they are granted by the government to monopoly firms They are all barriers to entry they guarantee that a market will be competitive

What do patents, economies of scale, and exclusive franchises have in common? All three of the other answers are correct they are granted by the government to monopoly firms They are all barriers to entry they guarantee that a market will be competitive

1. close or imperfect 2. lack or ownership 3. scale or inefficiency please answer asapp 20SUSL...

1. close or imperfect

2. lack or ownership

3. scale or inefficiency

please answer asapp

20SUSL Economics II Microeconomics (ECO-212-66250) Paige Hink & 07/30/20 8:57 PM Test: Third test-micro Time Remaining: 01:21:51 Submit Test This Question: 1 pt 20 of 48 (16 complete) This Test: 48 pts possible A monopolist is the single seller of a product or good for which there is no Substitute To maintain a monopoly, there must be barriers to entry Barriers to entry include patents,...

1. close or imperfect

2. lack or ownership

3. scale or inefficiency

please answer asapp

20SUSL Economics II Microeconomics (ECO-212-66250) Paige Hink & 07/30/20 8:57 PM Test: Third test-micro Time Remaining: 01:21:51 Submit Test This Question: 1 pt 20 of 48 (16 complete) This Test: 48 pts possible A monopolist is the single seller of a product or good for which there is no Substitute To maintain a monopoly, there must be barriers to entry Barriers to entry include patents,...

A monopoly is a market in which there are high barriers to entry, which are restrictions...

A monopoly is a market in which there are high barriers to entry, which are restrictions that make it difficult for new firms to enter a market. There are two types of barriers to entry: natural barriers and government-created barriers. Sort the following into the appropriate type of entry barrier. Taxi companies have market power because it is difficult for new companies to obtain a license to operate. ALCOA’s production costs per unit of aluminum continued to fall as the...

Below are several barriers to entry that businesses can use to maintain market power. Which of...

Below are several barriers to entry that businesses can use to maintain market power. Which of these barriers to entry is especially common among large oligopoly firms trying to maintain or increase their market power? O Legal rights to produce and sell their product Economies of scale Large spending on advertising Advanced technology that is difficult for other producers to replicate

Below are several barriers to entry that businesses can use to maintain market power. Which of these barriers to entry is especially common among large oligopoly firms trying to maintain or increase their market power? O Legal rights to produce and sell their product Economies of scale Large spending on advertising Advanced technology that is difficult for other producers to replicate

A monopoly is the single supplier of a product with no a. barriers to entry b....

A monopoly is the single supplier of a product with no a. barriers to entry b. close substitutes c. established price d. limit to supply over the relevant range of output with declining average total costs. In a natural monopoly, a firm has a. illegal barriers b.twenty-year patents c. pure competition d. economies of scale How does the demand curve for a product in a pure monopoly compare to the demand curve for the industry? a. They are the same....

A monopoly is the single supplier of a product with no a. barriers to entry b. close substitutes c. established price d. limit to supply over the relevant range of output with declining average total costs. In a natural monopoly, a firm has a. illegal barriers b.twenty-year patents c. pure competition d. economies of scale How does the demand curve for a product in a pure monopoly compare to the demand curve for the industry? a. They are the same....

Monopolies exist because of barriers to entry, obstacles that prevent other firms from entering an industry...

Monopolies exist because of barriers to entry, obstacles that prevent other firms from entering an industry and competing for market share. For each case below, indicate which barrier to entry applies. a. Coca-Cola's vast market share in the soft drink market: O Control of a resource O Legal barrier O Network externalities Economies of scale O Brand loyalty b. China's control of the market for rare earths (a group of minerals used to produce electronics): O Brand loyalty O Legal...

Monopolies exist because of barriers to entry, obstacles that prevent other firms from entering an industry and competing for market share. For each case below, indicate which barrier to entry applies. a. Coca-Cola's vast market share in the soft drink market: O Control of a resource O Legal barrier O Network externalities Economies of scale O Brand loyalty b. China's control of the market for rare earths (a group of minerals used to produce electronics): O Brand loyalty O Legal...

Part 1: List 5 Barriers to entry into a market

Part 1: List 5 Barriers to entry into a market1) _____________________________________ 2) _____________________________________3) _____________________________________ 4) _____________________________________5) _____________________________________Complete the following calculationsQuantityPriceTotal RevenueMarginal Revenue0$221$202$183$164$145$126$107$88$6Fill in the blanksA) ____________ ____________ is the ability of a seller or a buyer to affect market price.B) ____________ ____________ is the change in total revenue from selling one additional unit of output.C) ____________ to entry are factors that block the entry of new firms into a market.D) ____________ is a firm that is the lone seller of...

What do patents, economies of scale, and exclusive franchises have in common? All three of the other answers are correct they are granted by the government to monopoly firms They are all barriers to entry they guarantee that a market will be competitive

What do patents, economies of scale, and exclusive franchises have in common? All three of the other answers are correct they are granted by the government to monopoly firms They are all barriers to entry they guarantee that a market will be competitive

1. close or imperfect

2. lack or ownership

3. scale or inefficiency

please answer asapp

20SUSL Economics II Microeconomics (ECO-212-66250) Paige Hink & 07/30/20 8:57 PM Test: Third test-micro Time Remaining: 01:21:51 Submit Test This Question: 1 pt 20 of 48 (16 complete) This Test: 48 pts possible A monopolist is the single seller of a product or good for which there is no Substitute To maintain a monopoly, there must be barriers to entry Barriers to entry include patents,...

1. close or imperfect

2. lack or ownership

3. scale or inefficiency

please answer asapp

20SUSL Economics II Microeconomics (ECO-212-66250) Paige Hink & 07/30/20 8:57 PM Test: Third test-micro Time Remaining: 01:21:51 Submit Test This Question: 1 pt 20 of 48 (16 complete) This Test: 48 pts possible A monopolist is the single seller of a product or good for which there is no Substitute To maintain a monopoly, there must be barriers to entry Barriers to entry include patents,...

Below are several barriers to entry that businesses can use to maintain market power. Which of these barriers to entry is especially common among large oligopoly firms trying to maintain or increase their market power? O Legal rights to produce and sell their product Economies of scale Large spending on advertising Advanced technology that is difficult for other producers to replicate

Below are several barriers to entry that businesses can use to maintain market power. Which of these barriers to entry is especially common among large oligopoly firms trying to maintain or increase their market power? O Legal rights to produce and sell their product Economies of scale Large spending on advertising Advanced technology that is difficult for other producers to replicate

A monopoly is the single supplier of a product with no a. barriers to entry b. close substitutes c. established price d. limit to supply over the relevant range of output with declining average total costs. In a natural monopoly, a firm has a. illegal barriers b.twenty-year patents c. pure competition d. economies of scale How does the demand curve for a product in a pure monopoly compare to the demand curve for the industry? a. They are the same....

A monopoly is the single supplier of a product with no a. barriers to entry b. close substitutes c. established price d. limit to supply over the relevant range of output with declining average total costs. In a natural monopoly, a firm has a. illegal barriers b.twenty-year patents c. pure competition d. economies of scale How does the demand curve for a product in a pure monopoly compare to the demand curve for the industry? a. They are the same....

Monopolies exist because of barriers to entry, obstacles that prevent other firms from entering an industry and competing for market share. For each case below, indicate which barrier to entry applies. a. Coca-Cola's vast market share in the soft drink market: O Control of a resource O Legal barrier O Network externalities Economies of scale O Brand loyalty b. China's control of the market for rare earths (a group of minerals used to produce electronics): O Brand loyalty O Legal...

Monopolies exist because of barriers to entry, obstacles that prevent other firms from entering an industry and competing for market share. For each case below, indicate which barrier to entry applies. a. Coca-Cola's vast market share in the soft drink market: O Control of a resource O Legal barrier O Network externalities Economies of scale O Brand loyalty b. China's control of the market for rare earths (a group of minerals used to produce electronics): O Brand loyalty O Legal...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago