During Heaton Company’s first two years of operations, it reported absorption costing net operating income as follows:

| Year 1 | Year 2 | ||||

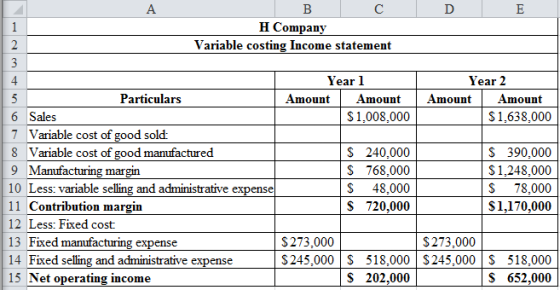

| Sales (@ $63 per unit) | $ | 1,008,000 | $ | 1,638,000 | |

| Cost of goods sold (@ $28 per unit) | 448,000 | 728,000 | |||

| Gross margin | 560,000 | 910,000 | |||

| Selling and administrative expenses* | 293,000 | 323,000 | |||

| Net operating income | $ | \267,000\ | $ | 587,000 | |

* $3 per unit variable; $245,000 fixed each year.

The company’s $28 unit product cost is computed as follows:

| Direct materials | $ | 6 |

| Direct labor | 8 | |

| Variable manufacturing overhead | 1 | |

| Fixed manufacturing overhead ($273,000 ÷ 21,000 units) | 13 | |

| Absorption costing unit product cost | $ | 28 |

Forty percent of fixed manufacturing overhead consists of wages and salaries; the remainder consists of depreciation charges on production equipment and buildings.

Production and cost data for the first two years of operatons are:

| Year 1 | Year 2 | |

| Units produced | 21,000 | 21,000 |

| Units sold | 16,000 | 26,000 |

Required:

1. Using variable costing, what is the unit product cost for both years?

2. What is the variable costing net operating income in Year 1 and in Year 2?

3. Reconcile the absorption costing and the variable costing net operating income figures for each year.

Complete this question by entering your answers in the tabs below

Required 1 : Using variable costing, what is the unit product cost for both years?

| Unit Product cost | ?????? |

Required 2 : What is the variable costing net operating income in Year 1 and in Year 2?

| Year 1 | Year 2 | |

| Net operating income (loss) |

Required 3 : Reconcile the absorption costing and the variable costing net operating income figures for each year. (Enter any losses or deductions as a negative value.)

Homework Answers

Absorption costing: The method of costing where both fixed and variable costs are charged to the products. Absorption costing absorbs the costs which are directly related to the product. The fixed overheads are charged to all the units manufactured irrespective of the number of units sold.

Variable costing: The method of costing where only variable costs are charged to the products is called as variable costing. The fixed overheads are charged to the units which are sold.

Variable cost: Variable cost refers to that cost which gets increased with the increase in the volume of output and decreases along with its decrease.

Fixed cost: The fixed cost is an expense which does not get affected by the level of output or the goods being produced.

Contribution margin: The balance when the sales are deducted by the variable costs is known as contribution margin. The management uses contribution margin to develop the weight of sales mix for multiple products. The contribution margin signifies the profit earned before deducting the fixed costs.

Unit product cost: The product cost per unit is determined by dividing the total of variable and fixed cost with the total number of units.

Net operating income: The net operating income is computed by deducting all fixed and variable expenses from the sales.

Inventory: Inventory refers to the goods purchased by a company from the manufacturers for reselling them to the customers. Transportation charges at the time of purchase, storage, insurance cost, and many more are included in the merchandise inventory account. Inventory is one of the important current assets of the company.

Selling and administrative overhead cost: The indirect cost involved in selling and distributing the goods or rendering the services are the selling cost and the cost involved in administrative purposes such as salary to employees, depreciation of office equipment are administrative cost.

Direct material cost: Direct material cost is the cost related to the purchase of the raw materials that are directly related to the production of the goods. It includes opening stock of materials, purchases, cost of purchases, and deducts the closing stock of materials.

Direct labor cost: It refers to the cost of providing wages to the workers who are directly associated with the production of goods or services rendered to the customers. The cost of direct labour includes the wages, payroll taxes, and all the benefits sponsored by the manufacturer.

(1)

Compute the unit product cost for both years using variable costing:

Thus, the unit product cost for both years using variable costing is $15.

(2)

Determine the net operating income in Year 1 and Year 2 under variable costing:

Thus,

Working note:

The variable costing income statement has been prepared as in the following manner:

(3)

Reconcile the absorption costing and the variable costing net operating income figures for each year:

Working note:

The unit product cost for both years using variable costing is $15.

Part 2

Add Answer to:

During Heaton Company’s first two years of operations, it

reported absorption costing net operating income as...

During Heaton Company’s first two years of operations, it reported absorption costing net operating income as...

During Heaton Company’s first two years of operations, it

reported absorption costing net operating income as follows:

* $3 per unit variable; $250,000 fixed each year.

The company’s $43 unit product cost is computed as follows:

Forty percent of fixed manufacturing overhead consists of wages

and salaries; the remainder consists of depreciation charges on

production equipment and buildings.

Production and cost data for the first two years of operatons

are:

Required:

1. Using variable costing, what is the unit product...

During Heaton Company’s first two years of operations, it

reported absorption costing net operating income as follows:

* $3 per unit variable; $250,000 fixed each year.

The company’s $43 unit product cost is computed as follows:

Forty percent of fixed manufacturing overhead consists of wages

and salaries; the remainder consists of depreciation charges on

production equipment and buildings.

Production and cost data for the first two years of operatons

are:

Required:

1. Using variable costing, what is the unit product...

During Heaton Company’s first two years of operations, it reported absorption costing net operating income as...

During Heaton Company’s first two years of operations, it reported absorption costing net operating income as follows: Year 1 Year 2 Sales (@ $62 per unit) $ 1,054,000 $ 1,674,000 Cost of goods sold (@ $32 per unit) 544,000 864,000 Gross margin 510,000 810,000 Selling and administrative expenses* 303,000 333,000 Net operating income $ \207,000\ $ 477,000 * $3 per unit variable; $252,000 fixed each year. The company’s $32 unit product cost is computed as follows: Direct materials $ 7...

During Heaton Company’s first two years of operations, it reported absorption costing net operating income as...

During Heaton Company’s first two years of operations, it reported absorption costing net operating income as follows: Year 1 Year 2 Sales (@ $60 per unit) $ 1,080,000 $ 1,680,000 Cost of goods sold (@ $33 per unit) 594,000 924,000 Gross margin 486,000 756,000 Selling and administrative expenses* 303,000 333,000 Net operating income $ \183,000\ $ 423,000 * $3 per unit variable; $249,000 fixed each year. The company’s $33 unit product cost is computed as follows: Direct materials $ 6...

During Heaton Company’s first two years of operations, it reported absorption costing net operating income as...

During Heaton Company’s first two years of operations, it reported absorption costing net operating income as follows: Year 1 Year 2 Sales (@ $62 per unit) $ 930,000 $ 1,550,000 Cost of goods sold (@ $35 per unit) 525,000 875,000 Gross margin 405,000 675,000 Selling and administrative expenses* 293,000 323,000 Net operating income $ \112,000\ $ 352,000 * $3 per unit variable; $248,000 fixed each year. The company’s $35 unit product cost is computed as follows: Direct materials $ 7...

During Heaton Company’s first two years of operations, it reported absorption costing net operating income as...

During Heaton Company’s first two years of operations, it reported absorption costing net operating income as follows: Year 1 Year 2 Sales (@ $61 per unit) $ 976,000 $ 1,586,000 Cost of goods sold (@ $38 per unit) 608,000 988,000 Gross margin 368,000 598,000 Selling and administrative expenses* 301,000 331,000 Net operating income $ \67,000\ $ 267,000 * $3 per unit variable; $253,000 fixed each year. The company’s $38 unit product cost is computed as follows: Direct materials $ 8...

During Heaton Company’s first two years of operations, it reported absorption costing net operating income as...

During Heaton Company’s first two years of operations, it reported absorption costing net operating income as follows: Year 1 Year 2 Sales (@ $61 per unit) $ 976,000 $ 1,586,000 Cost of goods sold (@ $38 per unit) 608,000 988,000 Gross margin 368,000 598,000 Selling and administrative expenses* 294,000 324,000 Net operating income $ \74,000\ $ 274,000 * $3 per unit variable; $246,000 fixed each year. The company’s $38 unit product cost is computed as follows: Direct materials $ 8...

During Heaton Company’s first two years of operations, it reported absorption costing net operating income as...

During Heaton Company’s first two years of operations, it reported absorption costing net operating income as follows: Year 1 Year 2 Sales (@ $62 per unit) $ 992,000 $ 1,612,000 Cost of goods sold (@ $35 per unit) 560,000 910,000 Gross margin 432,000 702,000 Selling and administrative expenses* 295,000 325,000 Net operating income $ \137,000\ $ 377,000 * $3 per unit variable; $247,000 fixed each year. The company’s $35 unit product cost is computed as follows: Direct materials $ 7...

During Heaton Company's first two years of operations, it reported absorption costing net operating income as...

During Heaton Company's first two years of operations, it reported absorption costing net operating income as follows: Sales @ $63 per unit) Cost of goods sold @ $39 per unit) Gross margin Selling and administrative expenses* Net operating income Year 1 $ 1,008,000 624,000 384,000 301,000 $ 83,000 Year 2 $ 1,638,000 1,014,000 624,000 331,000 $ 293,000 * $3 per unit variable: $253,000 fixed each year. The company's $39 unit product cost is computed as follows: Direct materials Direct labor...

During Heaton Company's first two years of operations, it reported absorption costing net operating income as follows: Sales @ $63 per unit) Cost of goods sold @ $39 per unit) Gross margin Selling and administrative expenses* Net operating income Year 1 $ 1,008,000 624,000 384,000 301,000 $ 83,000 Year 2 $ 1,638,000 1,014,000 624,000 331,000 $ 293,000 * $3 per unit variable: $253,000 fixed each year. The company's $39 unit product cost is computed as follows: Direct materials Direct labor...

During Heaton Company’s first two years of operations, it reported absorption costing net operating income as...

During Heaton Company’s first two years of operations, it

reported absorption costing net operating income as follows:

Year 1

Year 2

Sales (@ $62 per unit)

$

1,054,000

$

1,674,000

Cost of goods sold (@ $40 per unit)

680,000

1,080,000

Gross margin

374,000

594,000

Selling and administrative expenses*

300,000

330,000

Net operating income

$

74,000

$

264,000

* $3 per unit variable; $249,000 fixed each year.

The company’s $40 unit product cost is computed as follows:

Direct materials

$

7...

During Heaton Company’s first two years of operations, it

reported absorption costing net operating income as follows:

Year 1

Year 2

Sales (@ $62 per unit)

$

1,054,000

$

1,674,000

Cost of goods sold (@ $40 per unit)

680,000

1,080,000

Gross margin

374,000

594,000

Selling and administrative expenses*

300,000

330,000

Net operating income

$

74,000

$

264,000

* $3 per unit variable; $249,000 fixed each year.

The company’s $40 unit product cost is computed as follows:

Direct materials

$

7...

During Heaton Company’s first two years of operations, it reported absorption costing net operating income as...

During Heaton Company’s first two years of operations, it reported absorption costing net operating income as follows: Year 1 Year 2 Sales (@ $60 per unit) $ 960,000 $ 1,560,000 Cost of goods sold (@ $44 per unit) 704,000 1,144,000 Gross margin 256,000 416,000 Selling and administrative expenses* 303,000 333,000 Net operating income $ -47,000 $ 83,000 * $3 per unit variable; $255,000 fixed each year. The company’s $44 unit product cost is computed as follows: Direct materials $ 9...

During Heaton Company’s first two years of operations, it

reported absorption costing net operating income as follows:

* $3 per unit variable; $250,000 fixed each year.

The company’s $43 unit product cost is computed as follows:

Forty percent of fixed manufacturing overhead consists of wages

and salaries; the remainder consists of depreciation charges on

production equipment and buildings.

Production and cost data for the first two years of operatons

are:

Required:

1. Using variable costing, what is the unit product...

During Heaton Company’s first two years of operations, it

reported absorption costing net operating income as follows:

* $3 per unit variable; $250,000 fixed each year.

The company’s $43 unit product cost is computed as follows:

Forty percent of fixed manufacturing overhead consists of wages

and salaries; the remainder consists of depreciation charges on

production equipment and buildings.

Production and cost data for the first two years of operatons

are:

Required:

1. Using variable costing, what is the unit product...

During Heaton Company's first two years of operations, it reported absorption costing net operating income as follows: Sales @ $63 per unit) Cost of goods sold @ $39 per unit) Gross margin Selling and administrative expenses* Net operating income Year 1 $ 1,008,000 624,000 384,000 301,000 $ 83,000 Year 2 $ 1,638,000 1,014,000 624,000 331,000 $ 293,000 * $3 per unit variable: $253,000 fixed each year. The company's $39 unit product cost is computed as follows: Direct materials Direct labor...

During Heaton Company's first two years of operations, it reported absorption costing net operating income as follows: Sales @ $63 per unit) Cost of goods sold @ $39 per unit) Gross margin Selling and administrative expenses* Net operating income Year 1 $ 1,008,000 624,000 384,000 301,000 $ 83,000 Year 2 $ 1,638,000 1,014,000 624,000 331,000 $ 293,000 * $3 per unit variable: $253,000 fixed each year. The company's $39 unit product cost is computed as follows: Direct materials Direct labor...

During Heaton Company’s first two years of operations, it

reported absorption costing net operating income as follows:

Year 1

Year 2

Sales (@ $62 per unit)

$

1,054,000

$

1,674,000

Cost of goods sold (@ $40 per unit)

680,000

1,080,000

Gross margin

374,000

594,000

Selling and administrative expenses*

300,000

330,000

Net operating income

$

74,000

$

264,000

* $3 per unit variable; $249,000 fixed each year.

The company’s $40 unit product cost is computed as follows:

Direct materials

$

7...

During Heaton Company’s first two years of operations, it

reported absorption costing net operating income as follows:

Year 1

Year 2

Sales (@ $62 per unit)

$

1,054,000

$

1,674,000

Cost of goods sold (@ $40 per unit)

680,000

1,080,000

Gross margin

374,000

594,000

Selling and administrative expenses*

300,000

330,000

Net operating income

$

74,000

$

264,000

* $3 per unit variable; $249,000 fixed each year.

The company’s $40 unit product cost is computed as follows:

Direct materials

$

7...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago