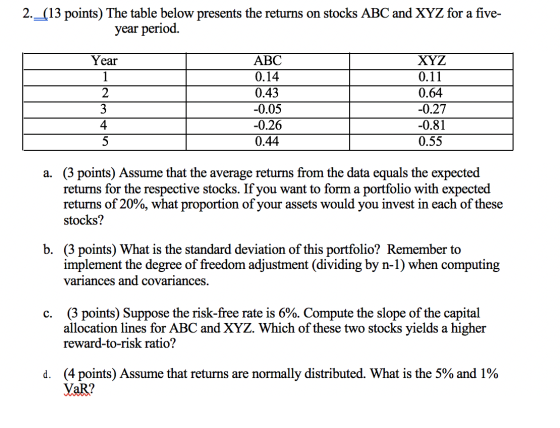

2. (13 points) The table below presents the returns on stocks ABC and XYZ for a five- year period.

Year ABC XYZ

1 0.14 0.11

2 0.43 0.64

3 -0.05 -0.27

4 -0.26 -0.81

5 0.44 0.55

a. (3 points) Assume that the average returns from the data equals the expected returns for the respective stocks. If you want to form a portfolio with expected returns of 20%, what proportion of your assets would you invest in each of these stocks?

b. (3 points) What is the standard deviation of this portfolio? Remember to implement the degree of freedom adjustment (dividing by n-1) when computing variances and covariances.

c. (3 points) Suppose the risk-free rate is 6%. Compute the slope of the capital allocation lines for ABC and XYZ. Which of these two stocks yields a higher reward-to-risk ratio?

d. (4 points) Assume that returns are normally distributed. What is the 5% and 1% VaR?

Homework Answers

| Year | ABC | XYZ |

| 1 | 0.14 | 0.11 |

| 2 | 0.43 | 0.64 |

| 3 | -0.5 | -0.27 |

| 4 | -0.26 | -0.81 |

| 5 | 0.44 | 0.55 |

| Average (Also Expected return) | 0.05 | 0.044 |

| Std Deviation | 0.42 | 0.60 |

| Correlation (ABC, XYZ) | 86% | |

| Convariance | 17% | |

| Variance | 24% |

a) Weight of a portfolio:

Expected return of Portfolio = W * Expected return of ABC + (1-W) * Expected return of XYZ

Expected return of Portfolio = W * 0.05 + (1-W) * 0.044 = 20%

Solving above equation:

W (ABC) = 26%

W (XYZ)= 1-26% = 74%

2) Std. Deviation of Portfolio

Formula

Std. Deviation of Portfolio = Sqrt [ W (ABC)^2 * Std Dev (ABC)^2 + W (XYZ)^2 * Std Dev (XYZ)^2 + 2* W (ABC) * Std Dev (ABC) + W (XYZ) * Std Dev (XYZ) * Correlation (ABC, XYZ)]

Std. Deviation of Portfolio = Sqrt [ (0.26^2 * 0.42^2) + (.74^2 * .6^2) + (2. 0.42 * 0.26 * 0.74 * 0.6 * 0.86)] = 54.1%

Slope of the portfolio:

Formula = (Portfolio Return - Risk Free Return)/ Std Dev of Portfolio

Slope of Portfolio = (20%- 6% ) / 54.1% = 0.258

4)

a) 5 % VAR= -1.65 * 54.1 % = -89%

b) 1 % VAR= -2.33 * 54.1 % = -126%

Add Answer to:

2. (13

points) The table below presents the returns on stocks ABC and XYZ

for a...

2. (13 points) The table below presents the returns on stocks ABC and XYZ for a...

2. (13 points) The table below presents the returns on stocks ABC and XYZ for a five- year period. Year 1 2 ABC 0.14 0.43 -0.05 -0.26 0.44 XYZ 0.11 0.64 -0.27 -0.81 0.55 3 4. a. (3 points) Assume that the average returns from the data equals the expected returns for the respective stocks. If you want to form a portfolio with expected returns of 20%, what proportion of your assets would you invest in each of these stocks?...

2. (13 points) The table below presents the returns on stocks ABC and XYZ for a five- year period. Year 1 2 ABC 0.14 0.43 -0.05 -0.26 0.44 XYZ 0.11 0.64 -0.27 -0.81 0.55 3 4. a. (3 points) Assume that the average returns from the data equals the expected returns for the respective stocks. If you want to form a portfolio with expected returns of 20%, what proportion of your assets would you invest in each of these stocks?...

2. You are given annual returns for stocks ABC and XYZ from the last 5 years:...

2. You are given annual returns for stocks ABC and XYZ from the last 5 years: Return on Stock ABC (in %) Return on Stock XYZ (in %) Year 1 11 9 2 12 7 13 6 4 15 5 5 14 11 a. What is your estimate of expected return for each of the stocks? b. What is your estimate of return standard deviation for each of the stocks? c. What is your estimate of the correlation between the...

2. You are given annual returns for stocks ABC and XYZ from the last 5 years: Return on Stock ABC (in %) Return on Stock XYZ (in %) Year 1 11 9 2 12 7 13 6 4 15 5 5 14 11 a. What is your estimate of expected return for each of the stocks? b. What is your estimate of return standard deviation for each of the stocks? c. What is your estimate of the correlation between the...

The expected returns for Securities ABC and XYZ are 8 percent and 13 percent, respectively. The...

The expected returns for Securities ABC and XYZ are 8 percent

and 13 percent, respectively. The standard deviation is 12 percent

for ABC and 18 percent for XYZ. There is no relationship between

the returns on the two securities. The market return is 12.5

percent with a standard deviation of 16 percent. The risk-free rate

is 5 percent. What is the Sharpe ratio of a portfolio with 40

percent of the funds in ABC and 60 percent in XYZ?

0.47...

The expected returns for Securities ABC and XYZ are 8 percent

and 13 percent, respectively. The standard deviation is 12 percent

for ABC and 18 percent for XYZ. There is no relationship between

the returns on the two securities. The market return is 12.5

percent with a standard deviation of 16 percent. The risk-free rate

is 5 percent. What is the Sharpe ratio of a portfolio with 40

percent of the funds in ABC and 60 percent in XYZ?

0.47...

Consider the rate of return of stocks ABC and XYZ. 14 Year 2 3 ABC 20%...

Consider the rate of return of stocks ABC and XYZ. 14 Year 2 3 ABC 20% 10 15 4 1 ΓΧΥΣ sex 12 18 1 -11 00:32:02 5 a. Calculate the arithmetic average return on these stocks over the sample period. (Do not round intermediate calculations. Round your answers to 2 decimal places.) Arithmetic Average ABC |XYZ b. Which stock has greater dispersion around the mean return? XYZ ОАВС c. Calculate the geometric average returns of each stock. What do...

Consider the rate of return of stocks ABC and XYZ. 14 Year 2 3 ABC 20% 10 15 4 1 ΓΧΥΣ sex 12 18 1 -11 00:32:02 5 a. Calculate the arithmetic average return on these stocks over the sample period. (Do not round intermediate calculations. Round your answers to 2 decimal places.) Arithmetic Average ABC |XYZ b. Which stock has greater dispersion around the mean return? XYZ ОАВС c. Calculate the geometric average returns of each stock. What do...

Stocks A and B have the following returns: Stock A Stock B 1 0.11 0.05 2...

Stocks A and B have the following returns: Stock A Stock B 1 0.11 0.05 2 0.04 0.04 3 0.14 0.05 4 -0.05 0.03 5 0.08 -0.02 c. If their correlation is 0.48, what is the expected return and standard deviation of a portfolio of 79 % stock A and 21% stock B? (Round to four decimal places.)

Stocks A & B have the expected returns and standard deviations shown in the table below:...

Stocks A & B have the expected returns and standard deviations shown in the table below: Stock E(R) 12% 30% 19% 50% The correlation between A and B is 0.4. The risk-free rate is 3% and you have a risk-aversion parameter of 2. What is the proportion of your investment in A and B, respectively, in your optimal risky portfolio?

Stocks A & B have the expected returns and standard deviations shown in the table below: Stock E(R) 12% 30% 19% 50% The correlation between A and B is 0.4. The risk-free rate is 3% and you have a risk-aversion parameter of 2. What is the proportion of your investment in A and B, respectively, in your optimal risky portfolio?

Question 8 (0.2 points) Consider the following probability distribution of returns on stock XYZ. What is...

Question 8 (0.2 points) Consider the following probability distribution of returns on stock XYZ. What is the expected return of stock XYZ? (Enter your answer as a percentage rounded to 2 decimal places. For example, enter 8.43%, instead of 0.0843) Probability Return 0.20 -3% 0.40 12% 0.40 27% Your Answer: Answer units View hint for Question 8 Question 9 (0.2 points) Calculate the expected return on a portfolio that contains 30% of a stock with an expected return of 1%...

Question 8 (0.2 points) Consider the following probability distribution of returns on stock XYZ. What is the expected return of stock XYZ? (Enter your answer as a percentage rounded to 2 decimal places. For example, enter 8.43%, instead of 0.0843) Probability Return 0.20 -3% 0.40 12% 0.40 27% Your Answer: Answer units View hint for Question 8 Question 9 (0.2 points) Calculate the expected return on a portfolio that contains 30% of a stock with an expected return of 1%...

2. Consider a market with only two risky stocks, A and B, and one risk-free asset....

2. Consider a market with only two risky stocks, A and B, and one risk-free asset. We have the following information about the stocks. Stock A Stock B Number of shares in the market 600 400 Price per share $2.00 $2.50 Expected rate of return 20% Standard dev.of return 12% Furthermore, the correlation coefficient between the returns of stocks A and B is PABWe assume that the returns are annual, and that the assumptions of CAPM hold. (a) (4 points)...

2. Consider a market with only two risky stocks, A and B, and one risk-free asset. We have the following information about the stocks. Stock A Stock B Number of shares in the market 600 400 Price per share $2.00 $2.50 Expected rate of return 20% Standard dev.of return 12% Furthermore, the correlation coefficient between the returns of stocks A and B is PABWe assume that the returns are annual, and that the assumptions of CAPM hold. (a) (4 points)...

4 Stocks below A В C Е 1 25 POINTS 2 You currently own the four...

4 Stocks below

A В C Е 1 25 POINTS 2 You currently own the four stocks below. 3 4 1. Please compute the portfolio beta and expected return. Put your final answers in the 5 provided green shaded cells. 6 2. Which of the stocks should you sell? Why? 7 10 11 3. Assume you sell the stock you mentioned in #2 above and invest the proceeds in an S&P 12 500 index fund. What will your new portfolio...

4 Stocks below

A В C Е 1 25 POINTS 2 You currently own the four stocks below. 3 4 1. Please compute the portfolio beta and expected return. Put your final answers in the 5 provided green shaded cells. 6 2. Which of the stocks should you sell? Why? 7 10 11 3. Assume you sell the stock you mentioned in #2 above and invest the proceeds in an S&P 12 500 index fund. What will your new portfolio...

Use Table 8.1, a computer, or a calculator to answer the following. Suppose a candidate for...

Use Table 8.1, a computer, or a calculator to answer the following. Suppose a candidate for public office is favored by only 47% of the voters. If a sample survey randomly selects 2,500 voters, the percentage in the sample who favor the candidate can be thought of as a measurement from a normal curve with a mean of 47% and a standard deviation of 1%. Based on this information, how often (as a %) would such a survey show that...

Use Table 8.1, a computer, or a calculator to answer the following. Suppose a candidate for public office is favored by only 47% of the voters. If a sample survey randomly selects 2,500 voters, the percentage in the sample who favor the candidate can be thought of as a measurement from a normal curve with a mean of 47% and a standard deviation of 1%. Based on this information, how often (as a %) would such a survey show that...

2. (13 points) The table below presents the returns on stocks ABC and XYZ for a five- year period. Year 1 2 ABC 0.14 0.43 -0.05 -0.26 0.44 XYZ 0.11 0.64 -0.27 -0.81 0.55 3 4. a. (3 points) Assume that the average returns from the data equals the expected returns for the respective stocks. If you want to form a portfolio with expected returns of 20%, what proportion of your assets would you invest in each of these stocks?...

2. (13 points) The table below presents the returns on stocks ABC and XYZ for a five- year period. Year 1 2 ABC 0.14 0.43 -0.05 -0.26 0.44 XYZ 0.11 0.64 -0.27 -0.81 0.55 3 4. a. (3 points) Assume that the average returns from the data equals the expected returns for the respective stocks. If you want to form a portfolio with expected returns of 20%, what proportion of your assets would you invest in each of these stocks?...

2. You are given annual returns for stocks ABC and XYZ from the last 5 years: Return on Stock ABC (in %) Return on Stock XYZ (in %) Year 1 11 9 2 12 7 13 6 4 15 5 5 14 11 a. What is your estimate of expected return for each of the stocks? b. What is your estimate of return standard deviation for each of the stocks? c. What is your estimate of the correlation between the...

2. You are given annual returns for stocks ABC and XYZ from the last 5 years: Return on Stock ABC (in %) Return on Stock XYZ (in %) Year 1 11 9 2 12 7 13 6 4 15 5 5 14 11 a. What is your estimate of expected return for each of the stocks? b. What is your estimate of return standard deviation for each of the stocks? c. What is your estimate of the correlation between the...

The expected returns for Securities ABC and XYZ are 8 percent

and 13 percent, respectively. The standard deviation is 12 percent

for ABC and 18 percent for XYZ. There is no relationship between

the returns on the two securities. The market return is 12.5

percent with a standard deviation of 16 percent. The risk-free rate

is 5 percent. What is the Sharpe ratio of a portfolio with 40

percent of the funds in ABC and 60 percent in XYZ?

0.47...

The expected returns for Securities ABC and XYZ are 8 percent

and 13 percent, respectively. The standard deviation is 12 percent

for ABC and 18 percent for XYZ. There is no relationship between

the returns on the two securities. The market return is 12.5

percent with a standard deviation of 16 percent. The risk-free rate

is 5 percent. What is the Sharpe ratio of a portfolio with 40

percent of the funds in ABC and 60 percent in XYZ?

0.47...

Consider the rate of return of stocks ABC and XYZ. 14 Year 2 3 ABC 20% 10 15 4 1 ΓΧΥΣ sex 12 18 1 -11 00:32:02 5 a. Calculate the arithmetic average return on these stocks over the sample period. (Do not round intermediate calculations. Round your answers to 2 decimal places.) Arithmetic Average ABC |XYZ b. Which stock has greater dispersion around the mean return? XYZ ОАВС c. Calculate the geometric average returns of each stock. What do...

Consider the rate of return of stocks ABC and XYZ. 14 Year 2 3 ABC 20% 10 15 4 1 ΓΧΥΣ sex 12 18 1 -11 00:32:02 5 a. Calculate the arithmetic average return on these stocks over the sample period. (Do not round intermediate calculations. Round your answers to 2 decimal places.) Arithmetic Average ABC |XYZ b. Which stock has greater dispersion around the mean return? XYZ ОАВС c. Calculate the geometric average returns of each stock. What do...

Stocks A & B have the expected returns and standard deviations shown in the table below: Stock E(R) 12% 30% 19% 50% The correlation between A and B is 0.4. The risk-free rate is 3% and you have a risk-aversion parameter of 2. What is the proportion of your investment in A and B, respectively, in your optimal risky portfolio?

Stocks A & B have the expected returns and standard deviations shown in the table below: Stock E(R) 12% 30% 19% 50% The correlation between A and B is 0.4. The risk-free rate is 3% and you have a risk-aversion parameter of 2. What is the proportion of your investment in A and B, respectively, in your optimal risky portfolio?

Question 8 (0.2 points) Consider the following probability distribution of returns on stock XYZ. What is the expected return of stock XYZ? (Enter your answer as a percentage rounded to 2 decimal places. For example, enter 8.43%, instead of 0.0843) Probability Return 0.20 -3% 0.40 12% 0.40 27% Your Answer: Answer units View hint for Question 8 Question 9 (0.2 points) Calculate the expected return on a portfolio that contains 30% of a stock with an expected return of 1%...

Question 8 (0.2 points) Consider the following probability distribution of returns on stock XYZ. What is the expected return of stock XYZ? (Enter your answer as a percentage rounded to 2 decimal places. For example, enter 8.43%, instead of 0.0843) Probability Return 0.20 -3% 0.40 12% 0.40 27% Your Answer: Answer units View hint for Question 8 Question 9 (0.2 points) Calculate the expected return on a portfolio that contains 30% of a stock with an expected return of 1%...

2. Consider a market with only two risky stocks, A and B, and one risk-free asset. We have the following information about the stocks. Stock A Stock B Number of shares in the market 600 400 Price per share $2.00 $2.50 Expected rate of return 20% Standard dev.of return 12% Furthermore, the correlation coefficient between the returns of stocks A and B is PABWe assume that the returns are annual, and that the assumptions of CAPM hold. (a) (4 points)...

2. Consider a market with only two risky stocks, A and B, and one risk-free asset. We have the following information about the stocks. Stock A Stock B Number of shares in the market 600 400 Price per share $2.00 $2.50 Expected rate of return 20% Standard dev.of return 12% Furthermore, the correlation coefficient between the returns of stocks A and B is PABWe assume that the returns are annual, and that the assumptions of CAPM hold. (a) (4 points)...

4 Stocks below

A В C Е 1 25 POINTS 2 You currently own the four stocks below. 3 4 1. Please compute the portfolio beta and expected return. Put your final answers in the 5 provided green shaded cells. 6 2. Which of the stocks should you sell? Why? 7 10 11 3. Assume you sell the stock you mentioned in #2 above and invest the proceeds in an S&P 12 500 index fund. What will your new portfolio...

4 Stocks below

A В C Е 1 25 POINTS 2 You currently own the four stocks below. 3 4 1. Please compute the portfolio beta and expected return. Put your final answers in the 5 provided green shaded cells. 6 2. Which of the stocks should you sell? Why? 7 10 11 3. Assume you sell the stock you mentioned in #2 above and invest the proceeds in an S&P 12 500 index fund. What will your new portfolio...

Use Table 8.1, a computer, or a calculator to answer the following. Suppose a candidate for public office is favored by only 47% of the voters. If a sample survey randomly selects 2,500 voters, the percentage in the sample who favor the candidate can be thought of as a measurement from a normal curve with a mean of 47% and a standard deviation of 1%. Based on this information, how often (as a %) would such a survey show that...

Use Table 8.1, a computer, or a calculator to answer the following. Suppose a candidate for public office is favored by only 47% of the voters. If a sample survey randomly selects 2,500 voters, the percentage in the sample who favor the candidate can be thought of as a measurement from a normal curve with a mean of 47% and a standard deviation of 1%. Based on this information, how often (as a %) would such a survey show that...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago