Let the dynamics Xi , i = 1, 2, . . . , d be independently...

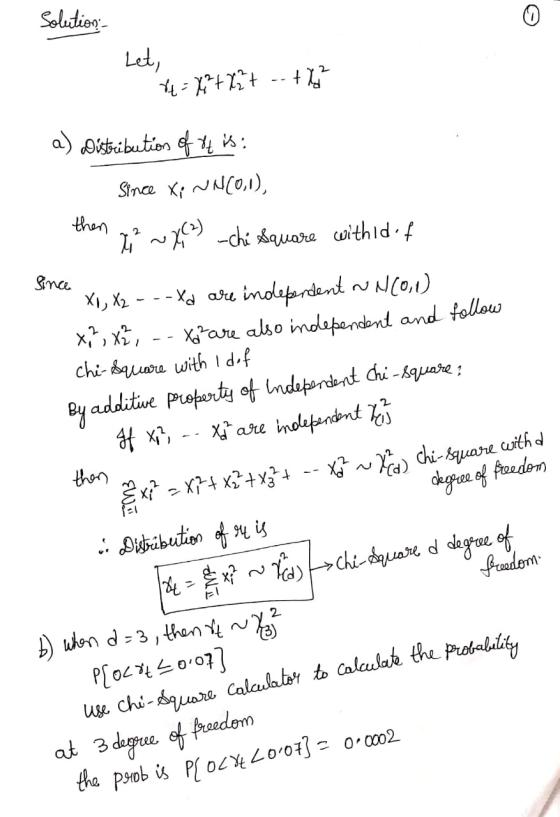

Let the dynamics Xi , i = 1, 2, . . . , d be independently and identically distributed as Z ∼ N(0, 1). One approach for modeling the short-term interest rate rt at any time t is given by defining rt ∆= X2 1 + X2 2 + . . . + X2 d .

(a) Describe the distribution of the continuous random variable rt.

(b) Find the probability that rt ∈ (0, 0.07] if d = 3.

(c) Find the probability that rt ∈ (0, 0.07] if d = 5.

Homework Answers

2. Let Xi exp(1) and X2 ~ variables with rate 1. Let: erp(1) be independent and...

2. Let Xi exp(1) and X2 ~ variables with rate 1. Let: erp(1) be independent and identically-distributed exponential random (a) What is the cdf of X1? b) What is the joint pdf of (Xi, X2)? (c) What is the joint pdf of (Y, Z)? d) What is the marginal pdf of z?

2. Let Xi exp(1) and X2 ~ variables with rate 1. Let: erp(1) be independent and identically-distributed exponential random (a) What is the cdf of X1? b) What is the joint pdf of (Xi, X2)? (c) What is the joint pdf of (Y, Z)? d) What is the marginal pdf of z?

PLEASE SOLVE ONLY QUESTION B B. Let be identically and independently distributed exponential random variables with...

PLEASE SOLVE ONLY QUESTION B

B. Let

be identically and independently distributed exponential random

variables with each having probability density function

. Then, find the probability density function of

HINT- Use the following decomposition:

A. LetX1,X2, ..., Xn be identically and independently distributed random variables with each having zero mean and variance σ. If j is defined as z,-X -X, j -1,2,..n where 7t k-1 then find E(Z,) and Var Z)

PLEASE SOLVE ONLY QUESTION B

B. Let

be identically and independently distributed exponential random

variables with each having probability density function

. Then, find the probability density function of

HINT- Use the following decomposition:

A. LetX1,X2, ..., Xn be identically and independently distributed random variables with each having zero mean and variance σ. If j is defined as z,-X -X, j -1,2,..n where 7t k-1 then find E(Z,) and Var Z)

2. [12 marksj Let Xi and X2 be independent and identically distributed random variables, each having...

2. [12 marksj Let Xi and X2 be independent and identically distributed random variables, each having an exponential distribution with density function (x),foro, 0, elsewbere Pdof W Let W = X1 +X2 and's Use the -method-of transformatiou- to find jhe joint probability density fuactíion of-W andy. AreWandfindependent?AThy? M covered m w, r 201 Instead tyto ind pdf of w b methed of colf

2. [12 marksj Let Xi and X2 be independent and identically distributed random variables, each having an exponential distribution with density function (x),foro, 0, elsewbere Pdof W Let W = X1 +X2 and's Use the -method-of transformatiou- to find jhe joint probability density fuactíion of-W andy. AreWandfindependent?AThy? M covered m w, r 201 Instead tyto ind pdf of w b methed of colf

Exercise 7. Let Xi, X2, . . . be independent, identically distributed rundorn variables uithEX and Var(X) 9, and let Yǐ = Xi/2. We also define Tn and An to be the sum and the sample mean, respectivel...

Exercise 7. Let Xi, X2, . . . be independent, identically distributed rundorn variables uithEX and Var(X) 9, and let Yǐ = Xi/2. We also define Tn and An to be the sum and the sample mean, respectively, of the random variablesy, ,Y,- 1) Evaluate the mean and variance of Yn, T,, and A (2) Does Yn converge in probability? If so, to what value? 3) Does Tn converge in probability? If so, to what value? (4) Does An converge...

Exercise 7. Let Xi, X2, . . . be independent, identically distributed rundorn variables uithEX and Var(X) 9, and let Yǐ = Xi/2. We also define Tn and An to be the sum and the sample mean, respectively, of the random variablesy, ,Y,- 1) Evaluate the mean and variance of Yn, T,, and A (2) Does Yn converge in probability? If so, to what value? 3) Does Tn converge in probability? If so, to what value? (4) Does An converge...

2. Let Xi, X2, . Xn be a random sample from a distribution with the probability...

2. Let Xi, X2, . Xn be a random sample from a distribution with the probability density function f(x; θ-829-1, 0 < x < 1,0 < θ < oo. Find the MLE θ

2. Let Xi, X2, . Xn be a random sample from a distribution with the probability density function f(x; θ-829-1, 0 < x < 1,0 < θ < oo. Find the MLE θ

Let Xi,X2, , Xn be independent and identically distributed (ii.d.) Exponential(1) random variable...

Let Xi,X2, , Xn be independent and identically distributed (ii.d.) Exponential(1) random variables. 14] [41 (a) Find the method of moments estimator for X (b) Find the method of moments estimator for (c) Find the bias, variance and MSE (mean square erop) for the essimator in part () Total: [16]

Let Xi,X2, , Xn be independent and identically distributed (ii.d.) Exponential(1) random variables. 14] [41 (a) Find the method of moments estimator for X (b) Find the method of moments...

Let Xi,X2, , Xn be independent and identically distributed (ii.d.) Exponential(1) random variables. 14] [41 (a) Find the method of moments estimator for X (b) Find the method of moments estimator for (c) Find the bias, variance and MSE (mean square erop) for the essimator in part () Total: [16]

Let Xi,X2, , Xn be independent and identically distributed (ii.d.) Exponential(1) random variables. 14] [41 (a) Find the method of moments estimator for X (b) Find the method of moments...

5. (8 marks) Let X1, X2, ..., X6 be identically and independently distributed standard nor- mal...

5. (8 marks) Let X1, X2, ..., X6 be identically and independently distributed standard nor- mal random variables. Let X = Lit. What is the distribution of the random variable (a) W = L X}; (b) U = L-1(X; – ); (e) 230; and (d) 265x4+x3) ? You need to provide the answer as well as justification.

5. (8 marks) Let X1, X2, ..., X6 be identically and independently distributed standard nor- mal random variables. Let X = Lit. What is the distribution of the random variable (a) W = L X}; (b) U = L-1(X; – ); (e) 230; and (d) 265x4+x3) ? You need to provide the answer as well as justification.

D. Let Xi, X2,. be independent random variables from a uniform distribution over the interval [0,...

D. Let Xi, X2,. be independent random variables from a uniform distribution over the interval [0, 1]. Prove that the sequence X+XX. converges in probability and find the limit

D. Let Xi, X2,. be independent random variables from a uniform distribution over the interval [0, 1]. Prove that the sequence X+XX. converges in probability and find the limit

1. The random variables Xi, X2,.. are independent and identically distributed (iid), each with pdf f given in Assignment 4, Question 1. Let Sn- Xi+.+X Using the Central Limit Theorem and the graph of...

1. The random variables Xi, X2,.. are independent and identically distributed (iid), each with pdf f given in Assignment 4, Question 1. Let Sn- Xi+.+X Using the Central Limit Theorem and the graph of the standard normal distribution in Figure 1, approximate the probability P(S100 >600). Express your answer in the format x.x-10-x. Verify your answer by simulating 10,000 outcomes of Si00 and counting how many of them are > 600. Show the code 1.00 0.95 0.90 0.85 1.2 1.4...

1. The random variables Xi, X2,.. are independent and identically distributed (iid), each with pdf f given in Assignment 4, Question 1. Let Sn- Xi+.+X Using the Central Limit Theorem and the graph of the standard normal distribution in Figure 1, approximate the probability P(S100 >600). Express your answer in the format x.x-10-x. Verify your answer by simulating 10,000 outcomes of Si00 and counting how many of them are > 600. Show the code 1.00 0.95 0.90 0.85 1.2 1.4...

Let ?1, ... , ?10 are identically independently distributed (iid) with Gamma(2, ?) a) Compute the...

Let ?1, ... , ?10 are identically independently distributed (iid) with Gamma(2, ?) a) Compute the likelihood function (LF). b) Adopt the appropriate conjugate prior to the parameter ? (Hint: Choose hyperparameters optionally within the support of distribution). c) Using (a) and (b), find the posterior distribution of ?. d) Compute the minimum Bayesian risk estimator of ?.

2. Let Xi exp(1) and X2 ~ variables with rate 1. Let: erp(1) be independent and identically-distributed exponential random (a) What is the cdf of X1? b) What is the joint pdf of (Xi, X2)? (c) What is the joint pdf of (Y, Z)? d) What is the marginal pdf of z?

2. Let Xi exp(1) and X2 ~ variables with rate 1. Let: erp(1) be independent and identically-distributed exponential random (a) What is the cdf of X1? b) What is the joint pdf of (Xi, X2)? (c) What is the joint pdf of (Y, Z)? d) What is the marginal pdf of z?

PLEASE SOLVE ONLY QUESTION B

B. Let

be identically and independently distributed exponential random

variables with each having probability density function

. Then, find the probability density function of

HINT- Use the following decomposition:

A. LetX1,X2, ..., Xn be identically and independently distributed random variables with each having zero mean and variance σ. If j is defined as z,-X -X, j -1,2,..n where 7t k-1 then find E(Z,) and Var Z)

PLEASE SOLVE ONLY QUESTION B

B. Let

be identically and independently distributed exponential random

variables with each having probability density function

. Then, find the probability density function of

HINT- Use the following decomposition:

A. LetX1,X2, ..., Xn be identically and independently distributed random variables with each having zero mean and variance σ. If j is defined as z,-X -X, j -1,2,..n where 7t k-1 then find E(Z,) and Var Z)

2. [12 marksj Let Xi and X2 be independent and identically distributed random variables, each having an exponential distribution with density function (x),foro, 0, elsewbere Pdof W Let W = X1 +X2 and's Use the -method-of transformatiou- to find jhe joint probability density fuactíion of-W andy. AreWandfindependent?AThy? M covered m w, r 201 Instead tyto ind pdf of w b methed of colf

2. [12 marksj Let Xi and X2 be independent and identically distributed random variables, each having an exponential distribution with density function (x),foro, 0, elsewbere Pdof W Let W = X1 +X2 and's Use the -method-of transformatiou- to find jhe joint probability density fuactíion of-W andy. AreWandfindependent?AThy? M covered m w, r 201 Instead tyto ind pdf of w b methed of colf

Exercise 7. Let Xi, X2, . . . be independent, identically distributed rundorn variables uithEX and Var(X) 9, and let Yǐ = Xi/2. We also define Tn and An to be the sum and the sample mean, respectively, of the random variablesy, ,Y,- 1) Evaluate the mean and variance of Yn, T,, and A (2) Does Yn converge in probability? If so, to what value? 3) Does Tn converge in probability? If so, to what value? (4) Does An converge...

Exercise 7. Let Xi, X2, . . . be independent, identically distributed rundorn variables uithEX and Var(X) 9, and let Yǐ = Xi/2. We also define Tn and An to be the sum and the sample mean, respectively, of the random variablesy, ,Y,- 1) Evaluate the mean and variance of Yn, T,, and A (2) Does Yn converge in probability? If so, to what value? 3) Does Tn converge in probability? If so, to what value? (4) Does An converge...

2. Let Xi, X2, . Xn be a random sample from a distribution with the probability density function f(x; θ-829-1, 0 < x < 1,0 < θ < oo. Find the MLE θ

2. Let Xi, X2, . Xn be a random sample from a distribution with the probability density function f(x; θ-829-1, 0 < x < 1,0 < θ < oo. Find the MLE θ

Let Xi,X2, , Xn be independent and identically distributed (ii.d.) Exponential(1) random variables. 14] [41 (a) Find the method of moments estimator for X (b) Find the method of moments estimator for (c) Find the bias, variance and MSE (mean square erop) for the essimator in part () Total: [16]

Let Xi,X2, , Xn be independent and identically distributed (ii.d.) Exponential(1) random variables. 14] [41 (a) Find the method of moments estimator for X (b) Find the method of moments...

Let Xi,X2, , Xn be independent and identically distributed (ii.d.) Exponential(1) random variables. 14] [41 (a) Find the method of moments estimator for X (b) Find the method of moments estimator for (c) Find the bias, variance and MSE (mean square erop) for the essimator in part () Total: [16]

Let Xi,X2, , Xn be independent and identically distributed (ii.d.) Exponential(1) random variables. 14] [41 (a) Find the method of moments estimator for X (b) Find the method of moments...

5. (8 marks) Let X1, X2, ..., X6 be identically and independently distributed standard nor- mal random variables. Let X = Lit. What is the distribution of the random variable (a) W = L X}; (b) U = L-1(X; – ); (e) 230; and (d) 265x4+x3) ? You need to provide the answer as well as justification.

5. (8 marks) Let X1, X2, ..., X6 be identically and independently distributed standard nor- mal random variables. Let X = Lit. What is the distribution of the random variable (a) W = L X}; (b) U = L-1(X; – ); (e) 230; and (d) 265x4+x3) ? You need to provide the answer as well as justification.

D. Let Xi, X2,. be independent random variables from a uniform distribution over the interval [0, 1]. Prove that the sequence X+XX. converges in probability and find the limit

D. Let Xi, X2,. be independent random variables from a uniform distribution over the interval [0, 1]. Prove that the sequence X+XX. converges in probability and find the limit

1. The random variables Xi, X2,.. are independent and identically distributed (iid), each with pdf f given in Assignment 4, Question 1. Let Sn- Xi+.+X Using the Central Limit Theorem and the graph of the standard normal distribution in Figure 1, approximate the probability P(S100 >600). Express your answer in the format x.x-10-x. Verify your answer by simulating 10,000 outcomes of Si00 and counting how many of them are > 600. Show the code 1.00 0.95 0.90 0.85 1.2 1.4...

1. The random variables Xi, X2,.. are independent and identically distributed (iid), each with pdf f given in Assignment 4, Question 1. Let Sn- Xi+.+X Using the Central Limit Theorem and the graph of the standard normal distribution in Figure 1, approximate the probability P(S100 >600). Express your answer in the format x.x-10-x. Verify your answer by simulating 10,000 outcomes of Si00 and counting how many of them are > 600. Show the code 1.00 0.95 0.90 0.85 1.2 1.4...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago