Delta IBM Jan-83 0.04 0.027 Feb-83 0.027 0.01 Mar-83 -0.016 0.028 Apr-83 -0.043 0.15 May-83 -0.045...

| Delta | IBM | |

| Jan-83 | 0.04 | 0.027 |

| Feb-83 | 0.027 | 0.01 |

| Mar-83 | -0.016 | 0.028 |

| Apr-83 | -0.043 | 0.15 |

| May-83 | -0.045 | -0.041 |

| Jun-83 | 0.012 | 0.081 |

| Jul-83 | -0.259 | 0.001 |

| Aug-83 | 0.08 | 0.001 |

| Sep-83 | 0.041 | 0.062 |

| Oct-83 | 0.039 | -0.001 |

| Nov-83 | 0.12 | -0.066 |

| Dec-83 | -0.028 | 0.039 |

| Jan-84 | -0.013 | -0.065 |

| Feb-84 | -0.117 | -0.026 |

| Mar-84 | 0.065 | 0.034 |

| Apr-84 | -0.085 | -0.002 |

| May-84 | -0.07 | -0.044 |

| Jun-84 | -0.012 | -0.019 |

| Jul-84 | 0.045 | 0.047 |

| Aug-84 | 0.04 | 0.127 |

| Sep-84 | 0.008 | 0.004 |

| Oct-84 | 0.161 | 0.012 |

| Nov-84 | -0.026 | -0.023 |

| Dec-84 | 0.156 | 0.011 |

| Jan-85 | -0.01 | 0.108 |

| Feb-85 | 0.087 | -0.009 |

| Mar-85 | -0.003 | -0.052 |

| Apr-85 | -0.123 | -0.004 |

| May-85 | 0.179 | 0.025 |

| Jun-85 | 0.021 | -0.038 |

| Jul-85 | 0.008 | 0.062 |

| Aug-85 | -0.066 | -0.028 |

| Sep-85 | -0.112 | -0.022 |

| Oct-85 | -0.083 | 0.048 |

| Nov-85 | 0.02 | 0.085 |

| Dec-85 | 0.03 | 0.113 |

| Jan-86 | 0.122 | -0.026 |

| Feb-86 | -0.055 | 0.003 |

| Mar-86 | 0.076 | 0.004 |

| Apr-86 | 0.059 | 0.031 |

| May-86 | -0.043 | -0.018 |

| Jun-86 | -0.07 | -0.039 |

| Jul-86 | 0.018 | -0.096 |

| Aug-86 | 0.018 | 0.055 |

| Sep-86 | 0.026 | -0.031 |

| Oct-86 | 0.134 | -0.081 |

| Nov-86 | -0.018 | 0.037 |

| Dec-86 | -0.01 | -0.056 |

| Jan-87 | 0.161 | 0.073 |

| Feb-87 | 0.133 | 0.092 |

| Mar-87 | -0.129 | 0.076 |

| Apr-87 | -0.121 | 0.067 |

| May-87 | 0.151 | 0.006 |

| Jun-87 | 0.014 | 0.016 |

| Jul-87 | 0.043 | -0.009 |

| Aug-87 | -0.037 | 0.053 |

| Sep-87 | -0.067 | -0.105 |

| Oct-87 | -0.26 | -0.187 |

| Nov-87 | -0.137 | -0.087 |

| Dec-87 | 0.121 | 0.043 |

-

Above is the monthly returns of Delta and IBM. Assume that the risk free (monthly) rate is 0.0015. Using the calculations (the mean for each stock is the expected return) plot (i) Return-Standard Deviation diagram and (ii) Sharpe ratio across different weights.) The weight for one asset ranges from -1 to 2. Comment. What is the weight of the optimal risky portfolio? Comment.

Homework Answers

Calculation of Mean and Standard deviation of Both Stock Delta and IBM. On the basis of details given in table:

| Delta | IBM |

| {D- M(D)}^2 | {I- M(I)}^2 |

| 0.001348138 | 0.000729 |

| 0.000562496 | 0.198916 |

| 0.000371834 | 0.183184 |

| 0.002142116 | 0.093636 |

| 0.002331248 | 0.247009 |

| 7.59861E-05 | 0.140625 |

| 0.068792372 | 0.207025 |

| 0.005885498 | 0.207025 |

| 0.001422572 | 0.155236 |

| 0.001275704 | 0.208849 |

| 0.013622858 | 0.272484 |

| 0.000978626 | 0.173889 |

| 0.000265136 | 0.271441 |

| 0.014468 | 0.232324 |

| 0.003808988 | 0.178084 |

| 0.007793888 | 0.209764 |

| 0.005370398 | 0.25 |

| 0.00023357 | 0.225625 |

| 0.001740308 | 0.167281 |

| 0.001348138 | 0.108241 |

| 2.22501E-05 | 0.204304 |

| 0.024874652 | 0.197136 |

| 0.000857494 | 0.229441 |

| 0.023322482 | 0.198025 |

| 0.000176438 | 0.121104 |

| 0.007008536 | 0.216225 |

| 3.94761E-05 | 0.258064 |

| 0.015947396 | 0.2116 |

| 0.030876464 | 0.185761 |

| 0.000313892 | 0.244036 |

| 2.22501E-05 | 0.155236 |

| 0.004800134 | 0.234256 |

| 0.01329017 | 0.228484 |

| 0.007444756 | 0.166464 |

| 0.000279458 | 0.137641 |

| 0.000713798 | 0.117649 |

| 0.014093726 | 0.232324 |

| 0.003396908 | 0.205209 |

| 0.005287762 | 0.204304 |

| 0.003104384 | 0.180625 |

| 0.002142116 | 0.224676 |

| 0.005370398 | 0.245025 |

| 0.00021659 | 0.304704 |

| 0.00021659 | 0.160801 |

| 0.000516062 | 0.237169 |

| 0.017086934 | 0.288369 |

| 0.000452966 | 0.175561 |

| 0.000176438 | 0.262144 |

| 0.024874652 | 0.146689 |

| 0.0168265 | 0.132496 |

| 0.017498792 | 0.1444 |

| 0.015446264 | 0.151321 |

| 0.021820312 | 0.2025 |

| 0.000114854 | 0.1936 |

| 0.00157744 | 0.216225 |

| 0.00162272 | 0.162409 |

| 0.0049397 | 0.314721 |

| 0.069317938 | 0.413449 |

| 0.01967932 | 0.294849 |

| 0.013857292 | 0.170569 |

| 0.523464183 | 12.100932 |

| Mean (Stock Delta) | Sum of Return | |||

| Total No. of Month | ||||

| Mean (D) | = | 0.197/60 | ||

| 0.003283333 | ||||

| Standard Deviation (Delta) | ||||

| SD (D) | = | Square Root of | Sum of {D- M(D)}^2 | |

| Total No. of Month -1 | ||||

| = | 0.523464183 | |||

| 60-1 | ||||

| = | 0.523464183 | |||

| 59 | ||||

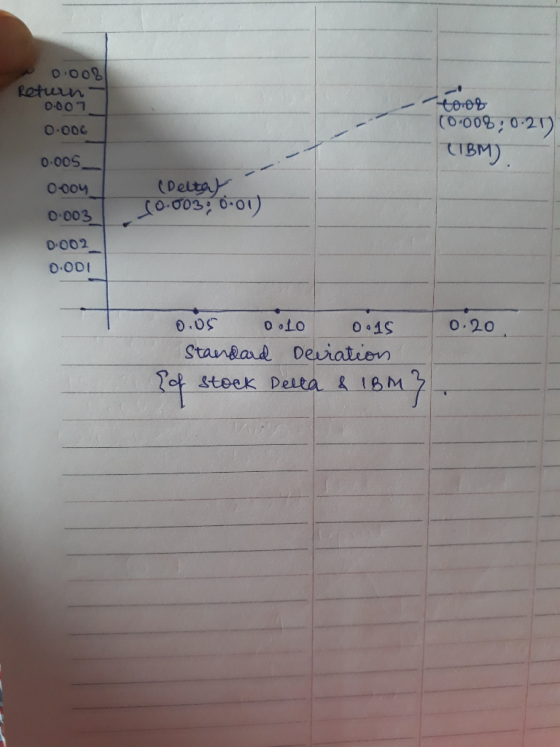

| = | 0.008872274 | |||

| Mean (Stock IBM) | Sum of Return | |||

| Total No. of Month | ||||

| Mean (I) | = | 0.456/60 | ||

| 0.0076 | ||||

| Standard Deviation (IBM) | ||||

| SD (I) | = | Square Root of | Sum of {I- M(I)}^2 | |

| Total No. of Month -1 | ||||

| = | 12.284244 | |||

| 60-1 | ||||

| = | 12.284244 | |||

| 59 | ||||

| = | 0.208207525 | |||

On the basis of above values, diagram of Mean and Standard deviation is as follows:

Now, lets do calculation of sharpe ratio.

For sharpe ratio it is informed that weights can be between -1 to 2. So all the possible portfolio mixes are here under:

| Delta | IBM | |||

| Mean | 0.0033 | 0.0076 | ||

| Standard Deviation (SD) | 0.0089 | 0.2082 | ||

| Case 1: Portfolio 1 | Sell one stock of Delta and Buy Two stock of IBM | |||

| Weights | -1 | 2 | ||

| Therefore, | ||||

| Delta | IBM | Total | ||

| Weighted Mean | -0.003283333 | 0.0152 | 0.011916667 | |

| Weighted SD | -0.008872274 | 0.416415051 | 0.407542777 | |

| Sharp Ratio | Weighted Mean- Risk Free Interest Rate | |||

| Weighted SD | ||||

| = | 0.01191-0.0015 | |||

| 0.4075 | ||||

| = | 0.0104 | |||

| 0.4075 | ||||

| = | 0.0255 | 2nd Rank | ||

| Case 2: Portfolio 2 | Buy One stock of IBM only | |||

| Weights | 0 | 1 | ||

| Therefore, | ||||

| Delta | IBM | Total | ||

| Weighted Mean | 0 | 0.0076 | 0.0076 | |

| Weighted SD | 0 | 0.2082 | 0.2082 | |

| Sharp Ratio | W(M)- Rf | |||

| W( SD) | ||||

| = | 0.0076-0.0015 | |||

| 0.2082 | ||||

| = | 0.0061 | |||

| 0.2082 | ||||

| = | 0.0292 | 1st Rank | ||

| Case 3: Portfolio 3 | Buy One stock of Delta only | |||

| Weights | 1 | 0 | ||

| Therefore, | ||||

| Delta | IBM | Total | ||

| Weighted Mean (W(M)) | 0.00328 | 0 | 0.00328 | |

| Weighted SD(W(SD)) | 0.0088 | 0 | 0.0088 | |

| Sharp Ratio | W (Mean)- Risk Free Interest Rate(Rf) | |||

| W (SD) | ||||

| = | 0.00328-0.0015 | |||

| 0.0088 | ||||

| = | 0.00178 | |||

| 0.0088 | ||||

| = | 0.2009 | 3rd Rank | ||

| Case 4: Portfolio 4 | Buy Two stock of Delta and Sell one stock of IBM | |||

| Weights | 2 | -1 | ||

| Therefore, | ||||

| Delta | IBM | Total | ||

| Weighted Mean | 0.00656 | -0.0076 | -0.00103 | |

| Weighted SD | 0.0177 | -0.2082 | -0.1904 | |

| Sharp Ratio | W (M)- Rf | |||

| W(SD) | ||||

| = | -0.0025 | |||

| -0.1904 | ||||

| = | -0.0025 | |||

| -0.1904 | ||||

| = | 0.01330 | 4th Rank | ||

Conclusion: on the basis of above calculation we can conclude that if purchase of only one stock is possible then investor should go for Portfolio 2 i.e. invest all his funds in IBM stock only as it will provide highest Sharpe Ratio.

Otherwise, if it is mandatory to invest in both funds then investor should go for Portfolio 1 i.e. sell 1 stock of Delta and buy two stock of IBM.

Add Answer to:

Delta

IBM

Jan-83

0.04

0.027

Feb-83

0.027

0.01

Mar-83

-0.016

0.028

Apr-83

-0.043

0.15

May-83

-0.045...

Evaluating Epidemiological Trends US Annual Epidemiological Trends-Infectious Diseases Jan Feb Mar Apr May Jun Jul Aug...

Evaluating Epidemiological Trends US Annual Epidemiological Trends-Infectious Diseases Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Evaluate the annual epidemiological data for five infectious diseases in US populations. Answer the following questions, paying attention to the seasonal trends and the relative number of patients affected. We were unable to transcribe this imageWe were unable to transcribe this image

Evaluating Epidemiological Trends US Annual Epidemiological Trends-Infectious Diseases Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Evaluate the annual epidemiological data for five infectious diseases in US populations. Answer the following questions, paying attention to the seasonal trends and the relative number of patients affected. We were unable to transcribe this imageWe were unable to transcribe this image

please explain the answer. ocaut Coipany Jan Feb Mar Apr May Jun Jul Aug Sep Oct...

please explain the answer.

ocaut Coipany Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Month Seasonal index 1.2 1.3 1.1 1.0 1.0 0.9 0.8 0.7 0.9 1 L Sales (S '000s) 9.6 10.5 8.6 1 The seasonal index for December is: 1.0 1.1 6.4 7.2 8.3 7.4 7.1 6.0 5.4 A 0.8 B 0.9 C 1.0 D 1.1 E 1.2

please explain the answer.

ocaut Coipany Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Month Seasonal index 1.2 1.3 1.1 1.0 1.0 0.9 0.8 0.7 0.9 1 L Sales (S '000s) 9.6 10.5 8.6 1 The seasonal index for December is: 1.0 1.1 6.4 7.2 8.3 7.4 7.1 6.0 5.4 A 0.8 B 0.9 C 1.0 D 1.1 E 1.2

Date Gasoline Crude Oil Jan 01, 2010 2.031 79.07 Jan 08, 2010 2.124 82.34 Jan 15,...

Date Gasoline Crude Oil

Jan 01, 2010 2.031 79.07

Jan 08, 2010 2.124 82.34

Jan 15, 2010 2.079 80.06

Jan 22, 2010 2.010 76.62

Jan 29, 2010 1.942 73.94

Feb 05, 2010 1.885 74.57

Feb 12, 2010 1.908 73.88

Feb 19, 2010 2.031 78.25

Feb 26, 2010 2.042 79.22

Mar 05, 2010 2.127 80.19

Mar 12, 2010 2.154 81.76

Mar 19, 2010 2.150 81.44

Mar 26, 2010 2.118 80.65

Apr 02, 2010 2.191 83.01

Apr 09, 2010 2.238 85.66

Apr...

Date Gasoline Crude Oil

Jan 01, 2010 2.031 79.07

Jan 08, 2010 2.124 82.34

Jan 15, 2010 2.079 80.06

Jan 22, 2010 2.010 76.62

Jan 29, 2010 1.942 73.94

Feb 05, 2010 1.885 74.57

Feb 12, 2010 1.908 73.88

Feb 19, 2010 2.031 78.25

Feb 26, 2010 2.042 79.22

Mar 05, 2010 2.127 80.19

Mar 12, 2010 2.154 81.76

Mar 19, 2010 2.150 81.44

Mar 26, 2010 2.118 80.65

Apr 02, 2010 2.191 83.01

Apr 09, 2010 2.238 85.66

Apr...

Jan Feb Mar Apr May June $172,180 $171,965 $169,100 $170,048 $168,204 $17...

Jan Feb Mar Apr May June $172,180 $171,965 $169,100 $170,048 $168,204 $172,003 July Aug Sep Oct Nov Dec $172,938 $172,709 $171,500 $170,677 $170,732 $170,206 If the monthly staffing budget was $171,022 for all months last year, and one standard deviation equals $1,458, are any of these variances beyond the expected range of variation for the 2007 budget year? Illustrate this with a control chart that shows the actual budget by month, a mean line, +2 and -2 Standard deviations.

How to make a bar chart in R Studio using data below? ANNUAL JAN FEB MAR...

How to make a bar chart in R Studio using data below? ANNUAL JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC YEARS # CITIES Average Temperature (F) 76.5 73.5 74.2 75.5 76.7 77.8 79.2 79.7 80 79.8 78.7 76.6 74.6 22 37 Average High Temperature (F) 84.8 81.8 82.1 83 83.8 85.1 86.7 86.9 87.1 87.1 86.4 84.3 82.4 24 15 Average Low Temperature (F) 71.1 67.1 67 68.3 69.6 71.7 72.6 73.4 73.3 72.7 72.2...

PLEASE HELP... NO ONE WILL ANSWER THIS QUESTION. home / study / business / finance / finance questions and answers / con...

PLEASE HELP... NO ONE WILL ANSWER THIS QUESTION. home / study / business / finance / finance questions and answers / consider the monthly returns of ford motor company and general electric shown on the next page. ... Question: Consider the monthly returns of Ford Motor Company and General Electric shown on the next page. A... Consider the monthly returns of Ford Motor Company and General Electric shown on the next page. An Excel spreadsheet with the data is also...

Physical Geography Laboratory Manal Annual: 21 C (70 F); 161.8 cm (63.6" 3. New Orleans, Louisiana (30 N, 90 w FEB MAR JAN 3.7 14.7em 9.4 m 10.2 om11.9 4.0 46 u. Caroline Islands (SN, 137E) A...

Physical Geography Laboratory Manal Annual: 21 C (70 F); 161.8 cm (63.6" 3. New Orleans, Louisiana (30 N, 90 w FEB MAR JAN 3.7 14.7em 9.4 m 10.2 om11.9 4.0 46 u. Caroline Islands (SN, 137E) Average Annual: 27-C (51℉: 3962 cmus JAN FEB | MARI APR | MAY | JUN | JUL | AUG | SEP | (OT 14.8" l i1.8-1127 m) 30,0 сн" | 32.3 cm | 19.9. | .14.0. |15.7- 50.5 crn | 35.6 cm | |...

Physical Geography Laboratory Manal Annual: 21 C (70 F); 161.8 cm (63.6" 3. New Orleans, Louisiana (30 N, 90 w FEB MAR JAN 3.7 14.7em 9.4 m 10.2 om11.9 4.0 46 u. Caroline Islands (SN, 137E) Average Annual: 27-C (51℉: 3962 cmus JAN FEB | MARI APR | MAY | JUN | JUL | AUG | SEP | (OT 14.8" l i1.8-1127 m) 30,0 сн" | 32.3 cm | 19.9. | .14.0. |15.7- 50.5 crn | 35.6 cm | |...

Energy Healthcare May-11 Sep-11 Oct-11 Jun-12 Sep-12 Oct-12 Nov-12 Dec-12 Mar-13 May-13 Oct-13 De...

Energy Healthcare May-11 Sep-11 Oct-11 Jun-12 Sep-12 Oct-12 Nov-12 Dec-12 Mar-13 May-13 Oct-13 Dec-13 6 Mar-14 un-14 Jul-14 14 ep-14 ct-14 4.67 9.05 8.57 Feb-15 5.02 4.8 Apr-15 0.58 7.79 Aug-15 4.83 5.81 Dec-15 11.81 1.5 8.84 1.8 12.42 Apr-16 May-16 2.62 2.75 0.04 5.2 4.95 0.59 7.67 Jul-16 Aug-16 Dec-16 0.2 5.23 The following table shows a portion of the monthly returns data (in percent) for 2010-2016 for two of Vanguard's mutual funds: the Vanguard Energy Fund and the...

Energy Healthcare May-11 Sep-11 Oct-11 Jun-12 Sep-12 Oct-12 Nov-12 Dec-12 Mar-13 May-13 Oct-13 Dec-13 6 Mar-14 un-14 Jul-14 14 ep-14 ct-14 4.67 9.05 8.57 Feb-15 5.02 4.8 Apr-15 0.58 7.79 Aug-15 4.83 5.81 Dec-15 11.81 1.5 8.84 1.8 12.42 Apr-16 May-16 2.62 2.75 0.04 5.2 4.95 0.59 7.67 Jul-16 Aug-16 Dec-16 0.2 5.23 The following table shows a portion of the monthly returns data (in percent) for 2010-2016 for two of Vanguard's mutual funds: the Vanguard Energy Fund and the...

Day Demand Avg Jan 88 Fab 89.06666667 Mar 88.375 Apr 88.03225806 Ma...

Day Demand Avg Jan 88 Fab 89.06666667 Mar 88.375 Apr 88.03225806 May 86.53125 Jun 81.87096774 Jul 79 Aug 80.125 Sep 83.61290323 Oct 88.5 Nov 89.29032258 Dec 90.21052632 Estimate the January forecast using Seasonal forecast. 12-month moving average forecast. Exponential smoothing (for an alpha of your choosing) Calculate the Mean Forecast Error (MFE), Mean Absolute Deviation (MAD) and Mean Squared Error (MSE) and compare the results. Write a line or two explaining the superior model(s) for this particular data set including...

Consider the following data: Monthly Profit of a Gym Month Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12...

Consider the following data: Monthly Profit of a Gym Month Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Profit ($) 5,650 5,403 5,004 4,677 5,170 5,598 6,419 6,169 5,903 Determine the three-period moving average for the next time period. If necessary, round your answer to one decimal place.

Evaluating Epidemiological Trends US Annual Epidemiological Trends-Infectious Diseases Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Evaluate the annual epidemiological data for five infectious diseases in US populations. Answer the following questions, paying attention to the seasonal trends and the relative number of patients affected. We were unable to transcribe this imageWe were unable to transcribe this image

Evaluating Epidemiological Trends US Annual Epidemiological Trends-Infectious Diseases Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Evaluate the annual epidemiological data for five infectious diseases in US populations. Answer the following questions, paying attention to the seasonal trends and the relative number of patients affected. We were unable to transcribe this imageWe were unable to transcribe this image

please explain the answer.

ocaut Coipany Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Month Seasonal index 1.2 1.3 1.1 1.0 1.0 0.9 0.8 0.7 0.9 1 L Sales (S '000s) 9.6 10.5 8.6 1 The seasonal index for December is: 1.0 1.1 6.4 7.2 8.3 7.4 7.1 6.0 5.4 A 0.8 B 0.9 C 1.0 D 1.1 E 1.2

please explain the answer.

ocaut Coipany Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Month Seasonal index 1.2 1.3 1.1 1.0 1.0 0.9 0.8 0.7 0.9 1 L Sales (S '000s) 9.6 10.5 8.6 1 The seasonal index for December is: 1.0 1.1 6.4 7.2 8.3 7.4 7.1 6.0 5.4 A 0.8 B 0.9 C 1.0 D 1.1 E 1.2

Date Gasoline Crude Oil

Jan 01, 2010 2.031 79.07

Jan 08, 2010 2.124 82.34

Jan 15, 2010 2.079 80.06

Jan 22, 2010 2.010 76.62

Jan 29, 2010 1.942 73.94

Feb 05, 2010 1.885 74.57

Feb 12, 2010 1.908 73.88

Feb 19, 2010 2.031 78.25

Feb 26, 2010 2.042 79.22

Mar 05, 2010 2.127 80.19

Mar 12, 2010 2.154 81.76

Mar 19, 2010 2.150 81.44

Mar 26, 2010 2.118 80.65

Apr 02, 2010 2.191 83.01

Apr 09, 2010 2.238 85.66

Apr...

Date Gasoline Crude Oil

Jan 01, 2010 2.031 79.07

Jan 08, 2010 2.124 82.34

Jan 15, 2010 2.079 80.06

Jan 22, 2010 2.010 76.62

Jan 29, 2010 1.942 73.94

Feb 05, 2010 1.885 74.57

Feb 12, 2010 1.908 73.88

Feb 19, 2010 2.031 78.25

Feb 26, 2010 2.042 79.22

Mar 05, 2010 2.127 80.19

Mar 12, 2010 2.154 81.76

Mar 19, 2010 2.150 81.44

Mar 26, 2010 2.118 80.65

Apr 02, 2010 2.191 83.01

Apr 09, 2010 2.238 85.66

Apr...

Physical Geography Laboratory Manal Annual: 21 C (70 F); 161.8 cm (63.6" 3. New Orleans, Louisiana (30 N, 90 w FEB MAR JAN 3.7 14.7em 9.4 m 10.2 om11.9 4.0 46 u. Caroline Islands (SN, 137E) Average Annual: 27-C (51℉: 3962 cmus JAN FEB | MARI APR | MAY | JUN | JUL | AUG | SEP | (OT 14.8" l i1.8-1127 m) 30,0 сн" | 32.3 cm | 19.9. | .14.0. |15.7- 50.5 crn | 35.6 cm | |...

Physical Geography Laboratory Manal Annual: 21 C (70 F); 161.8 cm (63.6" 3. New Orleans, Louisiana (30 N, 90 w FEB MAR JAN 3.7 14.7em 9.4 m 10.2 om11.9 4.0 46 u. Caroline Islands (SN, 137E) Average Annual: 27-C (51℉: 3962 cmus JAN FEB | MARI APR | MAY | JUN | JUL | AUG | SEP | (OT 14.8" l i1.8-1127 m) 30,0 сн" | 32.3 cm | 19.9. | .14.0. |15.7- 50.5 crn | 35.6 cm | |...

Energy Healthcare May-11 Sep-11 Oct-11 Jun-12 Sep-12 Oct-12 Nov-12 Dec-12 Mar-13 May-13 Oct-13 Dec-13 6 Mar-14 un-14 Jul-14 14 ep-14 ct-14 4.67 9.05 8.57 Feb-15 5.02 4.8 Apr-15 0.58 7.79 Aug-15 4.83 5.81 Dec-15 11.81 1.5 8.84 1.8 12.42 Apr-16 May-16 2.62 2.75 0.04 5.2 4.95 0.59 7.67 Jul-16 Aug-16 Dec-16 0.2 5.23 The following table shows a portion of the monthly returns data (in percent) for 2010-2016 for two of Vanguard's mutual funds: the Vanguard Energy Fund and the...

Energy Healthcare May-11 Sep-11 Oct-11 Jun-12 Sep-12 Oct-12 Nov-12 Dec-12 Mar-13 May-13 Oct-13 Dec-13 6 Mar-14 un-14 Jul-14 14 ep-14 ct-14 4.67 9.05 8.57 Feb-15 5.02 4.8 Apr-15 0.58 7.79 Aug-15 4.83 5.81 Dec-15 11.81 1.5 8.84 1.8 12.42 Apr-16 May-16 2.62 2.75 0.04 5.2 4.95 0.59 7.67 Jul-16 Aug-16 Dec-16 0.2 5.23 The following table shows a portion of the monthly returns data (in percent) for 2010-2016 for two of Vanguard's mutual funds: the Vanguard Energy Fund and the...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago