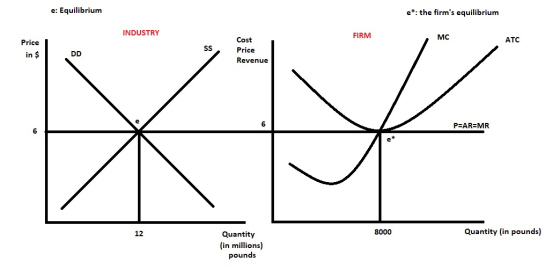

1.The turkey industry is perfectly competitive. Gobbler’s Turkey Farm is one of 1,500 turkey farms in...

1.The turkey industry is perfectly competitive. Gobbler’s Turkey Farm is one of 1,500 turkey farms in the industry. Each firm has the same cost curves. The market is currently in long-run equilibrium with a market price of $6 per pound and a total market production of 12,000,000 pounds.

a. How many pounds of turkey is Gobbler’s Turkey Farm currently producing?

b.What is Gobbler’s Turkey Farm’s ATC at this output level?

c.What is the Economic Profit of Gobbler’s Turkey Farm?

d.Draw two graphs: 1) Gobbler’s Turkey Farm MR, MC, and ATC curves and 2) the market supply and demand curves for turkey.

Be sure to correctly label all axes and indicate equilibrium.

2.Suppose the American Medical Association (AMA) reports that consumption of turkey reduces the chances of a heart attack.

Indicate on your graphs the expected short-run effects from this type of news on the market for turkeys and Gobbler’s Turkey Farm.

3. Given your answer in 2, what do you expect to happen in the long-run in the turkey market?

a. Show on your graphs the expected changes that will occur?

b. What will be the long-run market price in the turkey market?

c.What is the Economic Profit of Gobbler’s Turkey Farm?

Homework Answers

Answer to Question No. 1

Pounds of turkey is Gobbler’s Turkey Farm currently producing is 12000000/1500 = 8000 pounds (Total output/number of firms)

Firm's ATC is equal to the price of the product when the firm is in long run equilibrium. So ATC=P =$6.

Economic Profits in a situation when firm is in long run equilibrium is ZERO. The formula for profits = (P-ATC)*Q = (6-6)*8000 = 0

Add Answer to:

1.The turkey industry is perfectly competitive. Gobbler’s Turkey

Farm is one of 1,500 turkey farms in...

Consider a perfectly competitive market for titanium. Assume that all firms in the industry are identical and...

Consider a perfectly competitive market for titanium. Assume that all firms in the industry are identical and have the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. Assume also that it does not matter how many firms are in the industry Tool Tip: Place the mouse cursor over orange square points on the MC curve to see coordinates. COST PER UNIT IDollars per pound) 10 MC ATC AVC 0 5...

Consider a perfectly competitive market for titanium. Assume that all firms in the industry are identical and have the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. Assume also that it does not matter how many firms are in the industry Tool Tip: Place the mouse cursor over orange square points on the MC curve to see coordinates. COST PER UNIT IDollars per pound) 10 MC ATC AVC 0 5...

Consider the market for turkey, which is a perfectly competitive market. The long-run equallibrium price is...

Consider the market for turkey, which is a perfectly competitive market. The long-run equallibrium price is $3 per pound of turkey, and the long-run equillibrium quantity is 600 million pounds per years. Suppose the Surgeon General issues a report saying that eating turkey is bad for your health. The Surgeon General's report will cause consumers to demand MORE/LESS turkey at every price. In the short run, firms will respond by 1. producing less turkey and running at a loss 2....

The market for cashews is perfectly competitive and comprised of fifty (50) firms with identical cost...

The market for cashews is perfectly competitive and comprised of fifty (50) firms with identical cost structures and U-shaped ATC curves. The market demand curve for cashews is downward-sloping. The industry is initially in long run equilibrium at the following market price and quantity P* = $4/pound Q* = 50 pounds of cashews In TWO, well-labeled graphs (side by side), depict this long run equilibrium for both the cashew market and for the individual cashew firm. Be sure to calculate...

The market for cashews is perfectly competitive and comprised of fifty (50) firms with identical cost structures and U-shaped ATC curves. The market demand curve for cashews is downward-sloping. The industry is initially in long run equilibrium at the following market price and quantity P* = $4/pound Q* = 50 pounds of cashews In TWO, well-labeled graphs (side by side), depict this long run equilibrium for both the cashew market and for the individual cashew firm. Be sure to calculate...

1. Draw two graphs. On the first, show the short-run profit maximizing output of an individual...

1. Draw two graphs. On the first, show the short-run profit maximizing output of an individual firm earning an economic profit, including MR, MC, AVC, and ATC. On the second, show the short-run market equilibrium price and quantity. Explain how the industry supply curve and the market equilibrium price and quantity are determined. 2. What is the relationship between the price on the two graphs? Why does this relationship exist? 3. Explain why a firm in a perfectly competitive industry...

2. A perfectly competitive potato farm is currently in long run equilibrium. a. Graph the firm...

2. A perfectly competitive potato farm is currently in long run equilibrium. a. Graph the firm in long run equilibrium. Be sure to label all of the curves and the profit maximizing price and quantity. b. The demand for potatoes increases. Draw a new graph that shows the impact on an individual firm. Be sure to shade the area of loss or profit. c. Draw a new graph that shows how the firm and the industry adjusts to a new...

Аа Аа Consider a perfectly competitive market for titanium. Assume that all firms in the industry...

Аа Аа Consider a perfectly competitive market for titanium. Assume that all firms in the industry are identical and have the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. Assume also that it does not matter how many firms are in the industry. Tool Tip: Place the mouse cursor over orange square points on the MC curve to see coordinates. COSTS Dollars per pound) 10 MC 9 8 7 ATC...

Аа Аа Consider a perfectly competitive market for titanium. Assume that all firms in the industry are identical and have the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. Assume also that it does not matter how many firms are in the industry. Tool Tip: Place the mouse cursor over orange square points on the MC curve to see coordinates. COSTS Dollars per pound) 10 MC 9 8 7 ATC...

The U-pick berry market is perfectly competitive. Suppose that all U-pick blueberry farms have the same...

The U-pick berry market is perfectly competitive. Suppose that all U-pick blueberry farms have the same cost curves and all are making an economic profit. What happens as time passes? What is the long-run equilibrium outcome chegg

32. Ina sells her homegrown pumpkins at a roadside stand. Assume that the industry is perfectly competitive. The graph below represents the short run cost curves for Ina's pumpkins farm Part 1: I...

32. Ina sells her homegrown pumpkins at a roadside stand. Assume that the industry is perfectly competitive. The graph below represents the short run cost curves for Ina's pumpkins farm Part 1: In a separate model, draw the graph for the entire pumpkins market when the market price of pumpkins is S10. Part 2: (a) On Ina's pumpkins farm graph, label the ATC, AVC and MC curves. (b) Given the price in the pumpkins market, draw and label the market...

32. Ina sells her homegrown pumpkins at a roadside stand. Assume that the industry is perfectly competitive. The graph below represents the short run cost curves for Ina's pumpkins farm Part 1: In a separate model, draw the graph for the entire pumpkins market when the market price of pumpkins is S10. Part 2: (a) On Ina's pumpkins farm graph, label the ATC, AVC and MC curves. (b) Given the price in the pumpkins market, draw and label the market...

Problem 1. (13 points) Markets: Perfect Competition. Assume that a perfectly competitive, constant cost industry is...

Problem 1. (13 points) Markets: Perfect Competition. Assume that a perfectly competitive, constant cost industry is in a long run equilibrium with 35 firms. Each firm is producing 90 units of output which it sells at the price of $39 per unit; out of this amount each firm is paying $5 tax per unit of the output. The government decides to decrease the tax, so the firms will be paying $3 tax per unit. a) Explain what would happen in...

Consider the following two graphs for a product produced in a perfectly competitive market (think, for...

Consider the following two graphs for a product produced in a perfectly competitive market (think, for example, corn or oats). The graph on top shows the market supply and demand functions for this product. The one at the bottom is the cost curves for a typical firm in the industry producing this product. These cost curves pertain to long run. As you know, in the long run firms can change the amounts of invested capital, new firms can enter the...

Consider the following two graphs for a product produced in a perfectly competitive market (think, for example, corn or oats). The graph on top shows the market supply and demand functions for this product. The one at the bottom is the cost curves for a typical firm in the industry producing this product. These cost curves pertain to long run. As you know, in the long run firms can change the amounts of invested capital, new firms can enter the...

Consider a perfectly competitive market for titanium. Assume that all firms in the industry are identical and have the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. Assume also that it does not matter how many firms are in the industry Tool Tip: Place the mouse cursor over orange square points on the MC curve to see coordinates. COST PER UNIT IDollars per pound) 10 MC ATC AVC 0 5...

Consider a perfectly competitive market for titanium. Assume that all firms in the industry are identical and have the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. Assume also that it does not matter how many firms are in the industry Tool Tip: Place the mouse cursor over orange square points on the MC curve to see coordinates. COST PER UNIT IDollars per pound) 10 MC ATC AVC 0 5...

The market for cashews is perfectly competitive and comprised of fifty (50) firms with identical cost structures and U-shaped ATC curves. The market demand curve for cashews is downward-sloping. The industry is initially in long run equilibrium at the following market price and quantity P* = $4/pound Q* = 50 pounds of cashews In TWO, well-labeled graphs (side by side), depict this long run equilibrium for both the cashew market and for the individual cashew firm. Be sure to calculate...

The market for cashews is perfectly competitive and comprised of fifty (50) firms with identical cost structures and U-shaped ATC curves. The market demand curve for cashews is downward-sloping. The industry is initially in long run equilibrium at the following market price and quantity P* = $4/pound Q* = 50 pounds of cashews In TWO, well-labeled graphs (side by side), depict this long run equilibrium for both the cashew market and for the individual cashew firm. Be sure to calculate...

Аа Аа Consider a perfectly competitive market for titanium. Assume that all firms in the industry are identical and have the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. Assume also that it does not matter how many firms are in the industry. Tool Tip: Place the mouse cursor over orange square points on the MC curve to see coordinates. COSTS Dollars per pound) 10 MC 9 8 7 ATC...

Аа Аа Consider a perfectly competitive market for titanium. Assume that all firms in the industry are identical and have the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. Assume also that it does not matter how many firms are in the industry. Tool Tip: Place the mouse cursor over orange square points on the MC curve to see coordinates. COSTS Dollars per pound) 10 MC 9 8 7 ATC...

32. Ina sells her homegrown pumpkins at a roadside stand. Assume that the industry is perfectly competitive. The graph below represents the short run cost curves for Ina's pumpkins farm Part 1: In a separate model, draw the graph for the entire pumpkins market when the market price of pumpkins is S10. Part 2: (a) On Ina's pumpkins farm graph, label the ATC, AVC and MC curves. (b) Given the price in the pumpkins market, draw and label the market...

32. Ina sells her homegrown pumpkins at a roadside stand. Assume that the industry is perfectly competitive. The graph below represents the short run cost curves for Ina's pumpkins farm Part 1: In a separate model, draw the graph for the entire pumpkins market when the market price of pumpkins is S10. Part 2: (a) On Ina's pumpkins farm graph, label the ATC, AVC and MC curves. (b) Given the price in the pumpkins market, draw and label the market...

Consider the following two graphs for a product produced in a perfectly competitive market (think, for example, corn or oats). The graph on top shows the market supply and demand functions for this product. The one at the bottom is the cost curves for a typical firm in the industry producing this product. These cost curves pertain to long run. As you know, in the long run firms can change the amounts of invested capital, new firms can enter the...

Consider the following two graphs for a product produced in a perfectly competitive market (think, for example, corn or oats). The graph on top shows the market supply and demand functions for this product. The one at the bottom is the cost curves for a typical firm in the industry producing this product. These cost curves pertain to long run. As you know, in the long run firms can change the amounts of invested capital, new firms can enter the...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago