Preparing a consolidated income statement—Equity method with noncontrolling interest, AAP and upstream and downstream intercompany inventory...

Preparing a consolidated income statement—Equity method

with noncontrolling interest, AAP and upstream and downstream

intercompany inventory profits

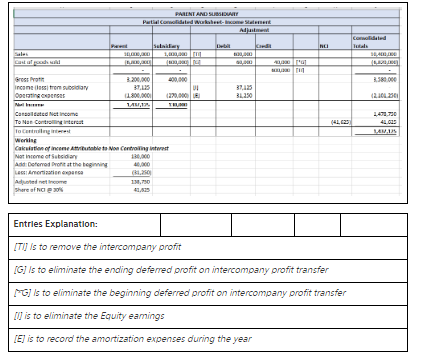

A parent company purchased a 70% controlling interest in its

subsidiary several years ago. The aggregate fair value of the

controlling and noncontrolling interest was $350,000 in excess of

the subsidiary’s Stockholders’ Equity on the acquisition date. This

excess was assigned to a building that was estimated to be

undervalued by $200,000 and to an unrecorded patent valued at

$150,000. The building asset is being depreciated over a 16-year

period and the patent is being amortized over an 8-year period,

both on the straight-line basis with no salvage value. During the

current year, the parent and subsidiary reported a total of

$600,000 of intercompany sales. At the beginning of the current

year, there were $40,000 of upstream intercompany profits in the

parent’s inventory. At the end of the current year, there were

$60,000 of downstream intercompany profits in the subsidiary’s

inventory. During the current year, the subsidiary declared and

paid $80,000 of dividends. The parent company uses the equity

method of pre-consolidation investment bookkeeping. Each company

reports the following income statement for the current year:

| Parent | Subsidiary | |

|---|---|---|

| Income statement: | ||

| Sales | $10,000,000 | $1,000,000 |

| Cost of goods sold | (6,800,000) | (600,000) |

| Gross profit | 3,200,000 | 400,000 |

| Income (loss) from subsidiary | 37,125 | - |

| Operating expenses | (1,800,000) | (270,000) |

| Net income | $1,437,125 | $130,000 |

a. Compute the Income (loss) from subsidiary of $37,125 reported by

the parent company in its preconsolidation income statement.

Do not use negative signs with your answers below.

| Subsidiary's net income | $Answer | ||

| AAP | Answer | ||

| Upstream sales | Answer | ||

| Adjusted subsidiary income | $Answer | ||

| P % of interest | X | Answer | % |

| Answer | |||

| Downstream sales | Answer | ||

| Income (loss) from subsidiary | $Answer | ||

b. Prepare the consolidated income statement for the current

year.

Do not use negative signs with your answers below.

| Consolidated Income Statement | |

|---|---|

| Sales | $Answer |

| Cost of goods sold | Answer |

| Gross profit | Answer |

| Operating expenses | Answer |

| Answer | |

| Net income | Answer |

| Net income attribute to non controlling interests |

| Net income attributes to parent |

Homework Answers

ANSWER:

Preparing a consolidated income statement—Equity method with noncontrolling interest, AAP and upstream and downstream intercompany inventory profits

Add Answer to:

Preparing a consolidated income statement—Equity method

with noncontrolling interest, AAP and upstream and downstream

intercompany inventory...

Preparing a consolidated income statement—Cost method with noncontrolling interest, AAP and upstream and downstream intercompany inventory...

Preparing a consolidated income statement—Cost method

with noncontrolling interest, AAP and upstream and downstream

intercompany inventory profits

A parent company purchased a 70% controlling interest in its

subsidiary several years ago. The aggregate fair value of the

controlling and noncontrolling interest was $300,000 in excess of

the subsidiary’s Stockholders’ Equity on the acquisition date. This

excess was assigned to a building that was estimated to be

undervalued by $180,000 and to an unrecorded Trademark valued at

$120,000. The building asset...

Preparing a consolidated income statement—Cost method

with noncontrolling interest, AAP and upstream and downstream

intercompany inventory profits

A parent company purchased a 70% controlling interest in its

subsidiary several years ago. The aggregate fair value of the

controlling and noncontrolling interest was $300,000 in excess of

the subsidiary’s Stockholders’ Equity on the acquisition date. This

excess was assigned to a building that was estimated to be

undervalued by $180,000 and to an unrecorded Trademark valued at

$120,000. The building asset...

Preparing a consolidated income statement-Cost method with noncontrolling interest, AAP and upstream and downstream intercompany inventory...

Preparing a consolidated income statement-Cost method with noncontrolling interest, AAP and upstream and downstream intercompany inventory profits A parent company purchased a 70% controlling interest in its subsidiary several years ago. The aggregate fair value of the controlling and noncontrolling interest was $300,000 in excess of the subsidiary's Stockholders' Equity on the acquisition date. This excess was assigned to a building that was estimated to be undervalued by $180,000 and to an unrecorded Trademark valued at $120,000. The building asset...

Preparing a consolidated income statement-Cost method with noncontrolling interest, AAP and upstream and downstream intercompany inventory profits A parent company purchased a 70% controlling interest in its subsidiary several years ago. The aggregate fair value of the controlling and noncontrolling interest was $300,000 in excess of the subsidiary's Stockholders' Equity on the acquisition date. This excess was assigned to a building that was estimated to be undervalued by $180,000 and to an unrecorded Trademark valued at $120,000. The building asset...

Preparing a consolidated income statement Equity method with noncontrolling interest, AAP and upstream intercompany depreciable asset...

Preparing a consolidated income statement Equity method with noncontrolling interest, AAP and upstream intercompany depreciable asset profits A parent company purchased an 80% controlling interest in its subsidiary several years ago. The aggregate fair value of the controlling and noncontrolling interest was $460,000 in excess of the subsidiary's Stockholders' Equity on the acquisition date. This excess was assigned to a building that was estimated to be undervalued by $300,000 and to an unrecorded Customer List valued at $160,000. The building...

Preparing a consolidated income statement Equity method with noncontrolling interest, AAP and upstream intercompany depreciable asset profits A parent company purchased an 80% controlling interest in its subsidiary several years ago. The aggregate fair value of the controlling and noncontrolling interest was $460,000 in excess of the subsidiary's Stockholders' Equity on the acquisition date. This excess was assigned to a building that was estimated to be undervalued by $300,000 and to an unrecorded Customer List valued at $160,000. The building...

Question 2Partially correctMark 5.00 out of 15.00 Not flaggedFlag question Question text Preparing a consolidated income...

Question 2Partially correctMark 5.00 out of 15.00 Not flaggedFlag question Question text Preparing a consolidated income statement—Equity method with noncontrolling interest, AAP and upstream and downstream intercompany inventory profits A parent company purchased a 70% controlling interest in its subsidiary several years ago. The aggregate fair value of the controlling and noncontrolling interest was $350,000 in excess of the subsidiary’s Stockholders’ Equity on the acquisition date. This excess was assigned to a building that was estimated to be undervalued by...

Upstream versus downstream inventory profits and net income attributable to the noncontrolling interest Assume that on...

Upstream versus downstream inventory profits and net income attributable to the noncontrolling interest Assume that on January 1, 2012, a parent company acquired a 90% interest in a subsidiary's voting common stock. On the date of acquisition, the fair value of the subsidiary's net assets equaled their reported book values. There were no intercompany sales during 2012. During the year ended December 31, 2013, the companies made $300,000 of intercompany sales. All intercompany sales include profits of 30% of selling...

Upstream versus downstream inventory profits and net income attributable to the noncontrolling interest Assume that on January 1, 2012, a parent company acquired a 90% interest in a subsidiary's voting common stock. On the date of acquisition, the fair value of the subsidiary's net assets equaled their reported book values. There were no intercompany sales during 2012. During the year ended December 31, 2013, the companies made $300,000 of intercompany sales. All intercompany sales include profits of 30% of selling...

Consolidation subsequent to date of acquisition - Equity method with noncontrolling interest and ...

Consolidation subsequent to date of acquisition - Equity method with noncontrolling interest and AAP Assume that, on January 1, 2009, a parent company acquired an 80% interest in its subsidiary. The total fair value of the controlling and noncontrolling interests was $500,000 over the book value of the subsidiary’s Stockholders’ Equity on the acquisition date. The parent assigned the excess to the following [A] assets: [A] Asset Initial Fair Value Useful Life (years) [A] Asset Initial Fair Value Useful Life...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume a parent...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume a parent company acquires a 75% interest in its subsidiary for a purchase price of $924,000. The excess of the total fair value of the controlling and noncontrolling Interests over the book value of the subsidiary's Stockholders' Equity is assigned to a building in PPE, net) that is worth $88,000 more than its book value, an unrecorded patent with a fair value of $144,000, and Goodwill...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume a parent company acquires a 75% interest in its subsidiary for a purchase price of $924,000. The excess of the total fair value of the controlling and noncontrolling Interests over the book value of the subsidiary's Stockholders' Equity is assigned to a building in PPE, net) that is worth $88,000 more than its book value, an unrecorded patent with a fair value of $144,000, and Goodwill...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume ...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume that a parent company acquires an 80% interest in its subsidiary for a purchase price of $620,800. The excess of the total fair value of the controlling and noncontrolling interests over the book value of the subsidiary's Stockholders' Equity is assigned to a building (in PPE, net) that the parent believes is worth $50,000 more than its book value, an: unrecorded Patent that the parent valued...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume that a parent company acquires an 80% interest in its subsidiary for a purchase price of $620,800. The excess of the total fair value of the controlling and noncontrolling interests over the book value of the subsidiary's Stockholders' Equity is assigned to a building (in PPE, net) that the parent believes is worth $50,000 more than its book value, an: unrecorded Patent that the parent valued...

E6.11 Help Please!! E6.11 Consolidated Income Statement, Intercompany Transactions Condensed income state- ments for...

E6.11 Help Please!!

E6.11 Consolidated Income Statement, Intercompany Transactions Condensed income state- ments for Pon and its 80 percent-owned subsidiary, Star, appear below Condensed Income Statements Pon Star Sales . $9,000,000 $4,000,000 439,000 . Equity in net income of Star Cost of goods sold. Other expenses . .. . ...(6,000,000) (2,500,000) (600,000) .. (2,000,000) Net income... $1,439,000 900,000 Intercompany sales are $1500,000. Unconfirmed intercompany profit in Pon's beginning inventory is $100,000, and unconfirmed intercompany profit in Pon's ending inventory is...

E6.11 Help Please!!

E6.11 Consolidated Income Statement, Intercompany Transactions Condensed income state- ments for Pon and its 80 percent-owned subsidiary, Star, appear below Condensed Income Statements Pon Star Sales . $9,000,000 $4,000,000 439,000 . Equity in net income of Star Cost of goods sold. Other expenses . .. . ...(6,000,000) (2,500,000) (600,000) .. (2,000,000) Net income... $1,439,000 900,000 Intercompany sales are $1500,000. Unconfirmed intercompany profit in Pon's beginning inventory is $100,000, and unconfirmed intercompany profit in Pon's ending inventory is...

Peat Company owns a 90% interest in Seaton Company. The consolidated income statement drafted by the...

Peat Company owns a 90% interest in Seaton Company. The

consolidated income statement drafted by the controller of Peat

Company appeared as follows:

Peat

Company and Subsidiary

Consolidated Income Statement

for Year Ended December 31, 2015

Sales

$14,098,400

Cost of Sales

9,191,200

Operating Expense

1,784,000

10,975,200

Consolidated Income

3,123,200

Less Noncontrolling Interest

in Consolidated Income

212,320

Controlling Interest in

Consolidated Net Income

$2,910,880

During your audit you discover that intercompany sales transactions

were not reflected in the controller’s draft of...

Peat Company owns a 90% interest in Seaton Company. The

consolidated income statement drafted by the controller of Peat

Company appeared as follows:

Peat

Company and Subsidiary

Consolidated Income Statement

for Year Ended December 31, 2015

Sales

$14,098,400

Cost of Sales

9,191,200

Operating Expense

1,784,000

10,975,200

Consolidated Income

3,123,200

Less Noncontrolling Interest

in Consolidated Income

212,320

Controlling Interest in

Consolidated Net Income

$2,910,880

During your audit you discover that intercompany sales transactions

were not reflected in the controller’s draft of...

Preparing a consolidated income statement—Cost method

with noncontrolling interest, AAP and upstream and downstream

intercompany inventory profits

A parent company purchased a 70% controlling interest in its

subsidiary several years ago. The aggregate fair value of the

controlling and noncontrolling interest was $300,000 in excess of

the subsidiary’s Stockholders’ Equity on the acquisition date. This

excess was assigned to a building that was estimated to be

undervalued by $180,000 and to an unrecorded Trademark valued at

$120,000. The building asset...

Preparing a consolidated income statement—Cost method

with noncontrolling interest, AAP and upstream and downstream

intercompany inventory profits

A parent company purchased a 70% controlling interest in its

subsidiary several years ago. The aggregate fair value of the

controlling and noncontrolling interest was $300,000 in excess of

the subsidiary’s Stockholders’ Equity on the acquisition date. This

excess was assigned to a building that was estimated to be

undervalued by $180,000 and to an unrecorded Trademark valued at

$120,000. The building asset...

Preparing a consolidated income statement-Cost method with noncontrolling interest, AAP and upstream and downstream intercompany inventory profits A parent company purchased a 70% controlling interest in its subsidiary several years ago. The aggregate fair value of the controlling and noncontrolling interest was $300,000 in excess of the subsidiary's Stockholders' Equity on the acquisition date. This excess was assigned to a building that was estimated to be undervalued by $180,000 and to an unrecorded Trademark valued at $120,000. The building asset...

Preparing a consolidated income statement-Cost method with noncontrolling interest, AAP and upstream and downstream intercompany inventory profits A parent company purchased a 70% controlling interest in its subsidiary several years ago. The aggregate fair value of the controlling and noncontrolling interest was $300,000 in excess of the subsidiary's Stockholders' Equity on the acquisition date. This excess was assigned to a building that was estimated to be undervalued by $180,000 and to an unrecorded Trademark valued at $120,000. The building asset...

Preparing a consolidated income statement Equity method with noncontrolling interest, AAP and upstream intercompany depreciable asset profits A parent company purchased an 80% controlling interest in its subsidiary several years ago. The aggregate fair value of the controlling and noncontrolling interest was $460,000 in excess of the subsidiary's Stockholders' Equity on the acquisition date. This excess was assigned to a building that was estimated to be undervalued by $300,000 and to an unrecorded Customer List valued at $160,000. The building...

Preparing a consolidated income statement Equity method with noncontrolling interest, AAP and upstream intercompany depreciable asset profits A parent company purchased an 80% controlling interest in its subsidiary several years ago. The aggregate fair value of the controlling and noncontrolling interest was $460,000 in excess of the subsidiary's Stockholders' Equity on the acquisition date. This excess was assigned to a building that was estimated to be undervalued by $300,000 and to an unrecorded Customer List valued at $160,000. The building...

Upstream versus downstream inventory profits and net income attributable to the noncontrolling interest Assume that on January 1, 2012, a parent company acquired a 90% interest in a subsidiary's voting common stock. On the date of acquisition, the fair value of the subsidiary's net assets equaled their reported book values. There were no intercompany sales during 2012. During the year ended December 31, 2013, the companies made $300,000 of intercompany sales. All intercompany sales include profits of 30% of selling...

Upstream versus downstream inventory profits and net income attributable to the noncontrolling interest Assume that on January 1, 2012, a parent company acquired a 90% interest in a subsidiary's voting common stock. On the date of acquisition, the fair value of the subsidiary's net assets equaled their reported book values. There were no intercompany sales during 2012. During the year ended December 31, 2013, the companies made $300,000 of intercompany sales. All intercompany sales include profits of 30% of selling...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume a parent company acquires a 75% interest in its subsidiary for a purchase price of $924,000. The excess of the total fair value of the controlling and noncontrolling Interests over the book value of the subsidiary's Stockholders' Equity is assigned to a building in PPE, net) that is worth $88,000 more than its book value, an unrecorded patent with a fair value of $144,000, and Goodwill...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume a parent company acquires a 75% interest in its subsidiary for a purchase price of $924,000. The excess of the total fair value of the controlling and noncontrolling Interests over the book value of the subsidiary's Stockholders' Equity is assigned to a building in PPE, net) that is worth $88,000 more than its book value, an unrecorded patent with a fair value of $144,000, and Goodwill...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume that a parent company acquires an 80% interest in its subsidiary for a purchase price of $620,800. The excess of the total fair value of the controlling and noncontrolling interests over the book value of the subsidiary's Stockholders' Equity is assigned to a building (in PPE, net) that the parent believes is worth $50,000 more than its book value, an: unrecorded Patent that the parent valued...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume that a parent company acquires an 80% interest in its subsidiary for a purchase price of $620,800. The excess of the total fair value of the controlling and noncontrolling interests over the book value of the subsidiary's Stockholders' Equity is assigned to a building (in PPE, net) that the parent believes is worth $50,000 more than its book value, an: unrecorded Patent that the parent valued...

E6.11 Help Please!!

E6.11 Consolidated Income Statement, Intercompany Transactions Condensed income state- ments for Pon and its 80 percent-owned subsidiary, Star, appear below Condensed Income Statements Pon Star Sales . $9,000,000 $4,000,000 439,000 . Equity in net income of Star Cost of goods sold. Other expenses . .. . ...(6,000,000) (2,500,000) (600,000) .. (2,000,000) Net income... $1,439,000 900,000 Intercompany sales are $1500,000. Unconfirmed intercompany profit in Pon's beginning inventory is $100,000, and unconfirmed intercompany profit in Pon's ending inventory is...

E6.11 Help Please!!

E6.11 Consolidated Income Statement, Intercompany Transactions Condensed income state- ments for Pon and its 80 percent-owned subsidiary, Star, appear below Condensed Income Statements Pon Star Sales . $9,000,000 $4,000,000 439,000 . Equity in net income of Star Cost of goods sold. Other expenses . .. . ...(6,000,000) (2,500,000) (600,000) .. (2,000,000) Net income... $1,439,000 900,000 Intercompany sales are $1500,000. Unconfirmed intercompany profit in Pon's beginning inventory is $100,000, and unconfirmed intercompany profit in Pon's ending inventory is...

Peat Company owns a 90% interest in Seaton Company. The

consolidated income statement drafted by the controller of Peat

Company appeared as follows:

Peat

Company and Subsidiary

Consolidated Income Statement

for Year Ended December 31, 2015

Sales

$14,098,400

Cost of Sales

9,191,200

Operating Expense

1,784,000

10,975,200

Consolidated Income

3,123,200

Less Noncontrolling Interest

in Consolidated Income

212,320

Controlling Interest in

Consolidated Net Income

$2,910,880

During your audit you discover that intercompany sales transactions

were not reflected in the controller’s draft of...

Peat Company owns a 90% interest in Seaton Company. The

consolidated income statement drafted by the controller of Peat

Company appeared as follows:

Peat

Company and Subsidiary

Consolidated Income Statement

for Year Ended December 31, 2015

Sales

$14,098,400

Cost of Sales

9,191,200

Operating Expense

1,784,000

10,975,200

Consolidated Income

3,123,200

Less Noncontrolling Interest

in Consolidated Income

212,320

Controlling Interest in

Consolidated Net Income

$2,910,880

During your audit you discover that intercompany sales transactions

were not reflected in the controller’s draft of...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago