Is X and Y from a pair of random variables such that : summation of X=5...

Is X and Y from a pair of random variables such that :

summation of X=5 Summation of Y=3 Summation of X2 = 30 Summation of Y2 =15 Summation of XY=20

if the variable has 10 observed values then the estimated value of Y when X = 3.1?

Homework Answers

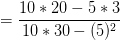

The estimated equation of line of regression of y on x is

where

= - 0.0364

=0.6727

Thus estimated line of regression is

For x = 3.1

Thus for x=3.1 estimated value of y = 2.05

Add Answer to:

Is X and Y from a pair of random variables such that :

summation of X=5...

14. Random variables X and Y have a density function f(x, y). Find the indicated expected...

14. Random variables X and Y have a density function f(x, y). Find the indicated expected value. f(x, y) = (xy + y2) 0<x< 1,0 <y<1 0 Elsewhere {$(wyty E(x2y) = 15. The means, standard deviations, and covariance for random variables X, Y. and Z are given below. LIX = 3. HY = 5. Az = 7 Ox= 1, = 3, oz = 4 cov(X,Y) = 1, cov (X, Z) = 3, and cov (Y,Z) = -3 T = X-2...

14. Random variables X and Y have a density function f(x, y). Find the indicated expected value. f(x, y) = (xy + y2) 0<x< 1,0 <y<1 0 Elsewhere {$(wyty E(x2y) = 15. The means, standard deviations, and covariance for random variables X, Y. and Z are given below. LIX = 3. HY = 5. Az = 7 Ox= 1, = 3, oz = 4 cov(X,Y) = 1, cov (X, Z) = 3, and cov (Y,Z) = -3 T = X-2...

5. (10 pts )The random variables X and Y have joint density function 1 f(x,y) x2...

5. (10 pts )The random variables X and Y have joint density function 1 f(x,y) x2 + y2 <1. 3 7T Compute the joint density function of R= x2 + y2 and = tan-'(Y/X).

5. (10 pts )The random variables X and Y have joint density function 1 f(x,y) x2 + y2 <1. 3 7T Compute the joint density function of R= x2 + y2 and = tan-'(Y/X).

Consider a pair of random variables X and Y, each of which take on values on...

Consider a pair of random variables X and Y, each of which take on values on the set A (1.2,3,4,5). The joint distribution of X and Y is a constant: Pxyx,y)-1/25 for all(x.y) pairs coming from the set A above. Let the random variable Z be given as the minimum of X and Y. Find the probability that Z is equal to 5.

Consider a pair of random variables X and Y, each of which take on values on the set A (1.2,3,4,5). The joint distribution of X and Y is a constant: Pxyx,y)-1/25 for all(x.y) pairs coming from the set A above. Let the random variable Z be given as the minimum of X and Y. Find the probability that Z is equal to 5.

The following relates to Problems 26 - 27. Let X, Y be random variables and b...

The following relates to Problems 26 - 27. Let X, Y be random variables and b a number. Problem 26: Find E (Y – bX)21 [1] E(X)b2 – 2E(XY)b+E(Y2); [2] E(X2)62 – E(Y); [3] -2E(XY)b+E(Y); [4] E(Y2); 151 E(X2)62 [6] Problem 27: Find b that minimizes E [(Y – bx)2] [1] E(YP); [2] E(X) – E(Y); [3] –2E(XY) + E(Y2); [4] ; [5]

The following relates to Problems 26 - 27. Let X, Y be random variables and b a number. Problem 26: Find E (Y – bX)21 [1] E(X)b2 – 2E(XY)b+E(Y2); [2] E(X2)62 – E(Y); [3] -2E(XY)b+E(Y); [4] E(Y2); 151 E(X2)62 [6] Problem 27: Find b that minimizes E [(Y – bx)2] [1] E(YP); [2] E(X) – E(Y); [3] –2E(XY) + E(Y2); [4] ; [5]

6. (a) Given that X and Y are continuous random variables, prove from first principles that:...

6. (a) Given that X and Y are continuous random variables, prove from first principles that: (b) The random variable X has a gamma distribution with parameters-: 3 and A-2 . Y is a related variable with conditional mean and variance of =x)= Calculate the unconditional mean and standard deviation of Y. (c) Suppose that a random variable X has a standard normal distribution, and the conditional distribution of a Poisson random variable Y, given the value ol XOx, has...

6. (a) Given that X and Y are continuous random variables, prove from first principles that: (b) The random variable X has a gamma distribution with parameters-: 3 and A-2 . Y is a related variable with conditional mean and variance of =x)= Calculate the unconditional mean and standard deviation of Y. (c) Suppose that a random variable X has a standard normal distribution, and the conditional distribution of a Poisson random variable Y, given the value ol XOx, has...

(a) For the random variable X, show that E[(x – a)?] is minimized when a =...

(a) For the random variable X, show that E[(x – a)?] is minimized when a = E(X). (b) For random variables X and Y, show that Var(X + Y) < Var(x) + Var(Y), that is, the standard deviation of the sum is less than or equal to the sum of standard deviations. (c) For random variables X and Y, prove the Cauchy-Schwartz Inequality: [E(XY)]? 5 E(X2) E(Y2)

(a) For the random variable X, show that E[(x – a)?] is minimized when a = E(X). (b) For random variables X and Y, show that Var(X + Y) < Var(x) + Var(Y), that is, the standard deviation of the sum is less than or equal to the sum of standard deviations. (c) For random variables X and Y, prove the Cauchy-Schwartz Inequality: [E(XY)]? 5 E(X2) E(Y2)

1) Let X and Y be random variables. Show that Cov( X + Y, X-Y) Var(X)--Var(Y)...

1) Let X and Y be random variables. Show that Cov( X + Y, X-Y) Var(X)--Var(Y) without appealing to the general formulas for the covariance of the linear combinations of sets of random variables; use the basic identity Cov(Z1,22)-E[Z1Z2]- E[Z1 E[Z2, valid for any two random variables, and the properties of the expected value 2) Let X be the normal random variable with zero mean and standard deviation Let ?(t) be the distribution function of the standard normal random variable....

1) Let X and Y be random variables. Show that Cov( X + Y, X-Y) Var(X)--Var(Y) without appealing to the general formulas for the covariance of the linear combinations of sets of random variables; use the basic identity Cov(Z1,22)-E[Z1Z2]- E[Z1 E[Z2, valid for any two random variables, and the properties of the expected value 2) Let X be the normal random variable with zero mean and standard deviation Let ?(t) be the distribution function of the standard normal random variable....

4. Suppose that X and Y are random variables with E(X) = 2, E(Y) = 1....

4. Suppose that X and Y are random variables with E(X) = 2, E(Y) = 1. E(X*) = 5, E(Y2-10, and E(XY) = 1 (a) Compute Corr(X,Y) (b) Choose a number c so that X and X +cY are uncorrelated

4. Suppose that X and Y are random variables with E(X) = 2, E(Y) = 1. E(X*) = 5, E(Y2-10, and E(XY) = 1 (a) Compute Corr(X,Y) (b) Choose a number c so that X and X +cY are uncorrelated

number2 how to solve it? Are x1 and x2 independent - yes, they are independent. Random variables X and Y having t...

number2 how to solve it?

Are x1 and x2 independent

- yes, they are independent.

Random variables X and Y having the joint density 1. 8 2)u(y 1)xy2 exp(4 2xy) fxy (x, y) ux- _ 3 1 1 Undergo a transformation T: 1 to generate new random variables Y -1. and Y2. Find the joint density of Y and Y2 X3)1/2 when X1 and X2 (XR 2. Determine the density of Y are joint Gaussian random variables with zero means...

number2 how to solve it?

Are x1 and x2 independent

- yes, they are independent.

Random variables X and Y having the joint density 1. 8 2)u(y 1)xy2 exp(4 2xy) fxy (x, y) ux- _ 3 1 1 Undergo a transformation T: 1 to generate new random variables Y -1. and Y2. Find the joint density of Y and Y2 X3)1/2 when X1 and X2 (XR 2. Determine the density of Y are joint Gaussian random variables with zero means...

2. Let R be the region R = {(X,Y)|X2 + y2 < 2} and let (X,Y)...

2. Let R be the region R = {(X,Y)|X2 + y2 < 2} and let (X,Y) be a pair of random variables that is distributed uniformly on this region. That is fx,y(x, y) is constant in this region and 0 elsewhere. State the sample space and find the probability that the random variable x2 + y2 is less than 1, P[X2 +Y? < 1].

2. Let R be the region R = {(X,Y)|X2 + y2 < 2} and let (X,Y) be a pair of random variables that is distributed uniformly on this region. That is fx,y(x, y) is constant in this region and 0 elsewhere. State the sample space and find the probability that the random variable x2 + y2 is less than 1, P[X2 +Y? < 1].

14. Random variables X and Y have a density function f(x, y). Find the indicated expected value. f(x, y) = (xy + y2) 0<x< 1,0 <y<1 0 Elsewhere {$(wyty E(x2y) = 15. The means, standard deviations, and covariance for random variables X, Y. and Z are given below. LIX = 3. HY = 5. Az = 7 Ox= 1, = 3, oz = 4 cov(X,Y) = 1, cov (X, Z) = 3, and cov (Y,Z) = -3 T = X-2...

14. Random variables X and Y have a density function f(x, y). Find the indicated expected value. f(x, y) = (xy + y2) 0<x< 1,0 <y<1 0 Elsewhere {$(wyty E(x2y) = 15. The means, standard deviations, and covariance for random variables X, Y. and Z are given below. LIX = 3. HY = 5. Az = 7 Ox= 1, = 3, oz = 4 cov(X,Y) = 1, cov (X, Z) = 3, and cov (Y,Z) = -3 T = X-2...

5. (10 pts )The random variables X and Y have joint density function 1 f(x,y) x2 + y2 <1. 3 7T Compute the joint density function of R= x2 + y2 and = tan-'(Y/X).

5. (10 pts )The random variables X and Y have joint density function 1 f(x,y) x2 + y2 <1. 3 7T Compute the joint density function of R= x2 + y2 and = tan-'(Y/X).

Consider a pair of random variables X and Y, each of which take on values on the set A (1.2,3,4,5). The joint distribution of X and Y is a constant: Pxyx,y)-1/25 for all(x.y) pairs coming from the set A above. Let the random variable Z be given as the minimum of X and Y. Find the probability that Z is equal to 5.

Consider a pair of random variables X and Y, each of which take on values on the set A (1.2,3,4,5). The joint distribution of X and Y is a constant: Pxyx,y)-1/25 for all(x.y) pairs coming from the set A above. Let the random variable Z be given as the minimum of X and Y. Find the probability that Z is equal to 5.

The following relates to Problems 26 - 27. Let X, Y be random variables and b a number. Problem 26: Find E (Y – bX)21 [1] E(X)b2 – 2E(XY)b+E(Y2); [2] E(X2)62 – E(Y); [3] -2E(XY)b+E(Y); [4] E(Y2); 151 E(X2)62 [6] Problem 27: Find b that minimizes E [(Y – bx)2] [1] E(YP); [2] E(X) – E(Y); [3] –2E(XY) + E(Y2); [4] ; [5]

The following relates to Problems 26 - 27. Let X, Y be random variables and b a number. Problem 26: Find E (Y – bX)21 [1] E(X)b2 – 2E(XY)b+E(Y2); [2] E(X2)62 – E(Y); [3] -2E(XY)b+E(Y); [4] E(Y2); 151 E(X2)62 [6] Problem 27: Find b that minimizes E [(Y – bx)2] [1] E(YP); [2] E(X) – E(Y); [3] –2E(XY) + E(Y2); [4] ; [5]

6. (a) Given that X and Y are continuous random variables, prove from first principles that: (b) The random variable X has a gamma distribution with parameters-: 3 and A-2 . Y is a related variable with conditional mean and variance of =x)= Calculate the unconditional mean and standard deviation of Y. (c) Suppose that a random variable X has a standard normal distribution, and the conditional distribution of a Poisson random variable Y, given the value ol XOx, has...

6. (a) Given that X and Y are continuous random variables, prove from first principles that: (b) The random variable X has a gamma distribution with parameters-: 3 and A-2 . Y is a related variable with conditional mean and variance of =x)= Calculate the unconditional mean and standard deviation of Y. (c) Suppose that a random variable X has a standard normal distribution, and the conditional distribution of a Poisson random variable Y, given the value ol XOx, has...

(a) For the random variable X, show that E[(x – a)?] is minimized when a = E(X). (b) For random variables X and Y, show that Var(X + Y) < Var(x) + Var(Y), that is, the standard deviation of the sum is less than or equal to the sum of standard deviations. (c) For random variables X and Y, prove the Cauchy-Schwartz Inequality: [E(XY)]? 5 E(X2) E(Y2)

(a) For the random variable X, show that E[(x – a)?] is minimized when a = E(X). (b) For random variables X and Y, show that Var(X + Y) < Var(x) + Var(Y), that is, the standard deviation of the sum is less than or equal to the sum of standard deviations. (c) For random variables X and Y, prove the Cauchy-Schwartz Inequality: [E(XY)]? 5 E(X2) E(Y2)

1) Let X and Y be random variables. Show that Cov( X + Y, X-Y) Var(X)--Var(Y) without appealing to the general formulas for the covariance of the linear combinations of sets of random variables; use the basic identity Cov(Z1,22)-E[Z1Z2]- E[Z1 E[Z2, valid for any two random variables, and the properties of the expected value 2) Let X be the normal random variable with zero mean and standard deviation Let ?(t) be the distribution function of the standard normal random variable....

1) Let X and Y be random variables. Show that Cov( X + Y, X-Y) Var(X)--Var(Y) without appealing to the general formulas for the covariance of the linear combinations of sets of random variables; use the basic identity Cov(Z1,22)-E[Z1Z2]- E[Z1 E[Z2, valid for any two random variables, and the properties of the expected value 2) Let X be the normal random variable with zero mean and standard deviation Let ?(t) be the distribution function of the standard normal random variable....

4. Suppose that X and Y are random variables with E(X) = 2, E(Y) = 1. E(X*) = 5, E(Y2-10, and E(XY) = 1 (a) Compute Corr(X,Y) (b) Choose a number c so that X and X +cY are uncorrelated

4. Suppose that X and Y are random variables with E(X) = 2, E(Y) = 1. E(X*) = 5, E(Y2-10, and E(XY) = 1 (a) Compute Corr(X,Y) (b) Choose a number c so that X and X +cY are uncorrelated

number2 how to solve it?

Are x1 and x2 independent

- yes, they are independent.

Random variables X and Y having the joint density 1. 8 2)u(y 1)xy2 exp(4 2xy) fxy (x, y) ux- _ 3 1 1 Undergo a transformation T: 1 to generate new random variables Y -1. and Y2. Find the joint density of Y and Y2 X3)1/2 when X1 and X2 (XR 2. Determine the density of Y are joint Gaussian random variables with zero means...

number2 how to solve it?

Are x1 and x2 independent

- yes, they are independent.

Random variables X and Y having the joint density 1. 8 2)u(y 1)xy2 exp(4 2xy) fxy (x, y) ux- _ 3 1 1 Undergo a transformation T: 1 to generate new random variables Y -1. and Y2. Find the joint density of Y and Y2 X3)1/2 when X1 and X2 (XR 2. Determine the density of Y are joint Gaussian random variables with zero means...

2. Let R be the region R = {(X,Y)|X2 + y2 < 2} and let (X,Y) be a pair of random variables that is distributed uniformly on this region. That is fx,y(x, y) is constant in this region and 0 elsewhere. State the sample space and find the probability that the random variable x2 + y2 is less than 1, P[X2 +Y? < 1].

2. Let R be the region R = {(X,Y)|X2 + y2 < 2} and let (X,Y) be a pair of random variables that is distributed uniformly on this region. That is fx,y(x, y) is constant in this region and 0 elsewhere. State the sample space and find the probability that the random variable x2 + y2 is less than 1, P[X2 +Y? < 1].

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago