Describe the major types of business organizations Class, as to equity accounts, what does the retained...

- Describe the major types of business organizations

- Class, as to equity accounts, what does the retained earnings statement look like?

- How do you find the navigation around Quickbooks? Is it user-friendly.

- What is the source of the opening balance of retained earnings?

- How does the cash flow statement tie together the income statement and balance sheet?

- For a manufacturing firm, what are the three inventory accounts? Using Ford Motor Co. as an example, what would be an example of each kind of inventory

Homework Answers

Answer :

(a) Major Types of Business Organization are :

1. Sole Proprietorship

- It 's simple form of business entity.

- It 's easy to form or create

- It require only few formal accounting requirements.

- No separate tax forms; you file taxes on your own personal income tax return. You can easily exchange personal and business assets. This is how most bloggers and freelancers operate.

- Sole proprietors are personally liable for debts, obligations including lawsuits.

- Personal assets are essentially treated, for liability purposes, as assets of the business.

- Business income is reported on personal return, deductions expenses like medical insurance are limited to the caps and restrictions for individuals. Hence, these deductions are less favorable to take as personal expenses than as business expenses.

2. Partnership

- A partnership (sometimes called a “general partnership”) is also a simple form of business entity.

- All items of income and deductions pass through the partnership to the partners according to percentage of ownership or partnership agreement.

- Items are reported on each partner’s respective personal tax return.

- No income tax is paid at the partnership level (though a partnership may be subject to other state and local taxes).

- Personal and business assets are not separate, subject to the liabilities and obligations of the partnership.

- Availability of certain types of deductions are limited to the tax floors and ceilings on personal income tax return.

3. Limited Liability Partnership

- Similar to a general partnership. .

- each partner is not liable for obligations and liabilities arising from the “negligence, omissions, malpractice, wrongful acts or misconduct” of the other partners. In other words, so long as observance of the proper rules, liability is largely limited to partner own actions.

- Income and losses pass through to the partners either in proportion to ownership or according to your partnership agreement.

- It has limited liability for “negligence, malpractice, omissions, etc.

4. Limited Liability Company

- It’s a hybrid entity that offers the liability protection of a C corporation with the tax option to be treated as a partnership or a corporation.

- It can be structured to provide for added flexibility, including unlimited members.

- It provides ease of operation and possibilities for expansion which makes it attractive for a number of freelancers.

- Governed by an Operating Agreement, which outlines plans for business management. Banks, mortgage companies and other institutions will want to see company agreement when making loans or setting up accounts. The Operating Agreement also allows to set up the “control” of the corporation and limit the transfer of interests.

- keep personal assets separate from your business assets, liability will largely be limited to your business assets.

5. S corporation

- The S corporation is another special form of corporation that operates like a C corporation but is taxed like a partnership. There are strict limitations on the structure of an S corporation including the number and types of shareholders.

- One of the most attractive features of the S corporation is the ability to “slice up” distributions to shareholders and reclassify those distributions.

- Traditionally, compensation to shareholders who also served as owners was taxable as ordinary income. As compensation for services, it was also subject to self-employment tax, which is the self-employed person’s version of FICA (Social Security and Medicare contributions). The rate for self-employment tax is 15.3% of wages (the equivalent of the employer and employee portion of FICA). This tax is on top of the actual income tax on those wages. The result is a painful hit – the same as operating as a sole proprietor.

- It has a number of restrictions relating to ownership . for example, If you lose S status due to a reporting or management violation, the time period is generally ten years before you can regain your status. The default is that you would be treated as a C corporation, which likely not a good thing from a tax perspective.

6. C corporation

- A C corporation is what most people generally think of when they think of corporations – C corporations are the companies usually followed by “Inc” in their names, as in Coca Cola, Inc.

- The advantages of a C corporation are continuous life, clear divisibility of assets between personal and corporate, limited liability among shareholders, freely transferable shares of stock, virtually unlimited options on structuring stock ownership, and favorable tax treatment for certain expenses. All good, right?

- The disadvantages of a corporation are increased administrative expenses, compliance formalities and the potential for “double taxation.” Increased administrative expenses are due to more complicated accounting and tax compliance (i.e. filing corporate returns). “Double taxation” is the result of a C corporation being a separate taxable entity and not a pass through. This means that the C corporation pays a tax on its income for the corporate year and the shareholders pay tax on dividends received from the corporation. Additionally, money that is paid out as salary is reported as ordinary income and is subject to FICA (Social Security and Medicare taxes) on the employer and employee sides; in a one person corporation, this is largely the same result as paying self-employment taxes since it’s the same pot of money.

- In most cases, a C corporation is “overkill” for a freelancer with no immediate plans for expansion, hiring of employees, etc.

(b)

We can classify Equity Accounts in following types :

The main equity accounts are:

#1 Common Stock

Common stock represents the owners’ or shareholder’s investment in the business as a capital contribution. This account represents the shares that entitle the share owners to vote and their residual claim on the company’s assets. The value of common stock is equal to the par value of the shares times the number of shares outstanding. For example, 1 million shares with $1 of par value would result in $1 million of common share capital on the balance sheet.

#2 Preferred Stock

Preferred stock is quite similar to common stock. The preferred stock is a type of share that often has no voting rights, but is guaranteed a cumulative dividend. If the dividend is not paid in one year, then it will accumulate until paid off.

Example: A preferred share of a company is entitled to $5 cumulative dividends in a year. The company has declared a dividend this year but has not paid dividends for the past two years. The shareholder will receive $15 ($5/year x 3 years) in dividends this year.

#3 Contributed Surplus

Contributed Surplus represents any amount paid over the par value paid by investors for stocks purchases that have a par value. This account also holds different types of gains and losses resulting in the sale of shares, or other complex financial instruments.

Example: The company issues 100,000 $1 par value shares for $10 per share. $100,000 (100,000 shares x $1/share) goes to common stock, and the excess $900,000 (100,000 shares x ($10-$1)) goes to Contributed Surplus.

#4 Additional Paid-In Capital

Additional Paid-In Capital is another term for contributed surplus, the same as is described above.

#5 Retained Earnings

Retained Earnings is the portion of net income that is not paid out as dividends to shareholders but retained for reinvesting or to pay off future obligations.

#6 Other Comprehensive Income

Other comprehensive income is excluded from net income on the income statement and consists of income that has not been realized yet. For example, unrealized gains or losses on securities that have not yet been sold would be reflected in other comprehensive income. Once the securities are sold the gain/loss will then move into net income on the income statement.

#7 Treasury Stock (contra-equity account)

Treasury stock is a contra-equity account and represents the amount of common stock that the company has purchased back from the investors. This is reflected in the books as a deduction from total equity.

The retained earning annexure look like :

| Retained Earnings Statement | |||||||||||

| For the Year Ended Mar 31, 2019 | |||||||||||

| Retained earnings, Apr 1 | XXXX | ||||||||||

| Add: | Net Income | XXXX | |||||||||

| XXXX | |||||||||||

| Less: | Dividend Declared and Other | XXXX | |||||||||

| Retained earnings, Mar 31 | XXXX | ||||||||||

(c) Navigation on quickbooks software by following below steps :

Read step-by-step instructions

1.

Your Dashboard

As soon as you log in, you’ll see the most important information about your business on your Dashboard.

2.

Profit and Loss

On the dashboard, QuickBooks shows your profit and loss, how much you spent, your sales summary, and what people owe you.

3.

Create Your First Invoice

And if you need to add something, like a sale or an invoice, you can do that right here.

4.

Add with the Plus Menu

You can also create invoices, and just about anything else, from the plus menu.

5.

Using the Search Bar

Once you’ve created a bunch of invoices and cheques, you might need to find one. Click search and enter the cheque number, date or amount.

6.

The Left Navigation Bar

QuickBooks has lots of good stuff on the left navigation bar. Under Invoicing you can see your customers, sales, and products or services you’re selling for your business.

7.

Reports

You can also get to QuickBooks reports here on the left.

8.

The Gear Menu

One more place you can look for things is the gear icon at the top right. You probably won’t need to use these tools as often, but this is where you’ll find your company settings and profile information.

9.

Advanced Accounting Tools

This is where you can find advanced accounting tools like Reconcile, Budgeting and the Audit Log.

Conclusion -Yes, Its useful as it finds information about supplier and customer. We can fetch also our sales data , purchase data , ratio analysis on finger tips. and any other information we can find very quickly. There are lot of features built on the board like P&L,Income, Sales, Invoices , Bank accounts etc.

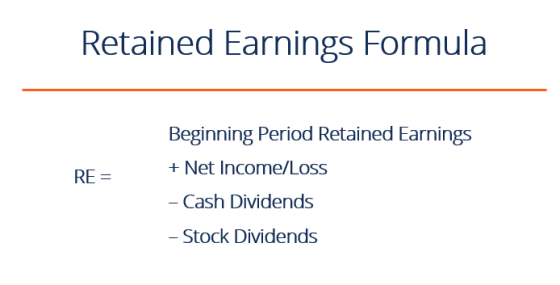

(d) Meaning- Retained Earnings (RE) are the portion of a business’s profits that are not distributed as dividends to shareholders but instead are reserved for reinvestment back into the business. Normally, these funds are used for working capital and fixed asset purchases (capital expenditures) or allotted for paying off debt obligations

Retained Earnings are reported on the balance sheet under the shareholder’s equity section at the end of each accounting period. To calculate RE, the beginning RE balance is added to the net income or loss and then dividend payouts are subtracted. A summary report called a statement of retained earnings is also maintained, outlining the changes in RE for a specific period

At the end of each accounting period, retained earnings are reported on the balance sheet as the accumulated income from the prior year (including the current year’s income), minus dividends paid to shareholders. In the next accounting cycle, the RE ending balance from the previous accounting period will now become the retained earnings beginning balance.

The RE balance may not always be a positive number as it may reflect that the current period’s net loss is greater than that of the RE beginning balance. Alternatively, a large distribution of dividends that exceed the retained earnings balance can cause it to go negative.

At the end of each accounting period, retained earnings are reported on the balance sheet as the accumulated income from the prior year (including the current year’s income), minus dividends paid to shareholders. In the next accounting cycle, the RE ending balance from the previous accounting period will now become the retained earnings beginning balance.

The RE balance may not always be a positive number as it may reflect that the current period’s net loss is greater than that of the RE beginning balance. Alternatively, a large distribution of dividends that exceed the retained earnings balance can cause it to go negative.

At the end of each accounting period, retained earnings are reported on the balance sheet as the accumulated income from the prior year (including the current year’s income), minus dividends paid to shareholders. In the next accounting cycle, the RE ending balance from the previous accounting period will now become the retained earnings beginning balance.

The RE balance may not always be a positive number as it may reflect that the current period’s net loss is greater than that of the RE beginning balance. Alternatively, a large distribution of dividends that exceed the retained earnings balance can cause it to go negative.

At the end of each accounting period, retained earnings are reported on the balance sheet as the accumulated income from the prior year (including the current year’s income), minus dividends paid to shareholders. In the next accounting cycle, the RE ending balance from the previous accounting period will now become the retained earnings beginning balance.

The RE balance may not always be a positive number as it may reflect that the current period’s net loss is greater than that of the RE beginning balance. Alternatively, a large distribution of dividends that exceed the retained earnings balance can cause it to go negative.

(e)

the bottom line of the income statement is net income. Net income links to both the balance sheet and cash flow statement.

In terms of the cash flow statement, net income is the first line as it is used to calculate cash flows from operations. Also, any non-cash expenses or non-cash income from the income statement (i.e., depreciation and amortization) flow into the cash flow statement and adjust net income to arrive at cash flow from operations.

In terms of the balance sheet, net income flows into stockholder’s equity via retained earnings. Retained earnings is equal to the previous period’s retained earnings plus net income from this period less dividends from this period.

Any balance sheet items that have a cash impact (i.e., working capital, financing, PP&E, etc.) are linked to the cash flow statement since it is either a source or use of cash. The net change in cash on the cash flow statement and cash from the previous period’s balance sheet comprise cash for this period.

(f) The three inventory accounts used by manufacturing companies are

- Raw Materials Inventory- Raw Materials Inventory includes materials used to manufacture a product.

- Work-in-Process Inventory- Work-in-Process Inventory includes goods that have been started in the manufacturing process but are not yet complete.

- Finished Goods Inventory- Finished Goods Inventory includes completed goods that have not yet been sold.

Let's take the example of Ford Motors Co., Each type of inventory should be classified In

(1) Raw material - Example are sheet metal, fiber, glasses and any other raw

(2) Work-In-Progress- Processing body, Job order inventory are in process , and assembly inventory

(3) Finished Inventory- New Car , Trucks, SUV and accessories

(4) Waste & Scrap- RM Scrap , WIP scrap etc

(5) Recyclable- RM and Other

Answer :

(a) Major Types of Business Organization are :

1. Sole Proprietorship

- It 's simple form of business entity.

- It 's easy to form or create

- It require only few formal accounting requirements.

- No separate tax forms; you file taxes on your own personal income tax return. You can easily exchange personal and business assets. This is how most bloggers and freelancers operate.

- Sole proprietors are personally liable for debts, obligations including lawsuits.

- Personal assets are essentially treated, for liability purposes, as assets of the business.

- Business income is reported on personal return, deductions expenses like medical insurance are limited to the caps and restrictions for individuals. Hence, these deductions are less favorable to take as personal expenses than as business expenses.

2. Partnership

- A partnership (sometimes called a “general partnership”) is also a simple form of business entity.

- All items of income and deductions pass through the partnership to the partners according to percentage of ownership or partnership agreement.

- Items are reported on each partner’s respective personal tax return.

- No income tax is paid at the partnership level (though a partnership may be subject to other state and local taxes).

- Personal and business assets are not separate, subject to the liabilities and obligations of the partnership.

- Availability of certain types of deductions are limited to the tax floors and ceilings on personal income tax return.

3. Limited Liability Partnership

- Similar to a general partnership. .

- each partner is not liable for obligations and liabilities arising from the “negligence, omissions, malpractice, wrongful acts or misconduct” of the other partners. In other words, so long as observance of the proper rules, liability is largely limited to partner own actions.

- Income and losses pass through to the partners either in proportion to ownership or according to your partnership agreement.

- It has limited liability for “negligence, malpractice, omissions, etc.

4. Limited Liability Company

- It’s a hybrid entity that offers the liability protection of a C corporation with the tax option to be treated as a partnership or a corporation.

- It can be structured to provide for added flexibility, including unlimited members.

- It provides ease of operation and possibilities for expansion which makes it attractive for a number of freelancers.

- Governed by an Operating Agreement, which outlines plans for business management. Banks, mortgage companies and other institutions will want to see company agreement when making loans or setting up accounts. The Operating Agreement also allows to set up the “control” of the corporation and limit the transfer of interests.

- keep personal assets separate from your business assets, liability will largely be limited to your business assets.

5. S corporation

- The S corporation is another special form of corporation that operates like a C corporation but is taxed like a partnership. There are strict limitations on the structure of an S corporation including the number and types of shareholders.

- One of the most attractive features of the S corporation is the ability to “slice up” distributions to shareholders and reclassify those distributions.

- Traditionally, compensation to shareholders who also served as owners was taxable as ordinary income. As compensation for services, it was also subject to self-employment tax, which is the self-employed person’s version of FICA (Social Security and Medicare contributions). The rate for self-employment tax is 15.3% of wages (the equivalent of the employer and employee portion of FICA). This tax is on top of the actual income tax on those wages. The result is a painful hit – the same as operating as a sole proprietor.

- It has a number of restrictions relating to ownership . for example, If you lose S status due to a reporting or management violation, the time period is generally ten years before you can regain your status. The default is that you would be treated as a C corporation, which likely not a good thing from a tax perspective.

6. C corporation

- A C corporation is what most people generally think of when they think of corporations – C corporations are the companies usually followed by “Inc” in their names, as in Coca Cola, Inc.

- The advantages of a C corporation are continuous life, clear divisibility of assets between personal and corporate, limited liability among shareholders, freely transferable shares of stock, virtually unlimited options on structuring stock ownership, and favorable tax treatment for certain expenses. All good, right?

- The disadvantages of a corporation are increased administrative expenses, compliance formalities and the potential for “double taxation.” Increased administrative expenses are due to more complicated accounting and tax compliance (i.e. filing corporate returns). “Double taxation” is the result of a C corporation being a separate taxable entity and not a pass through. This means that the C corporation pays a tax on its income for the corporate year and the shareholders pay tax on dividends received from the corporation. Additionally, money that is paid out as salary is reported as ordinary income and is subject to FICA (Social Security and Medicare taxes) on the employer and employee sides; in a one person corporation, this is largely the same result as paying self-employment taxes since it’s the same pot of money.

- In most cases, a C corporation is “overkill” for a freelancer with no immediate plans for expansion, hiring of employees, etc.

(b)

We can classify Equity Accounts in following types :

The main equity accounts are:

#1 Common Stock

Common stock represents the owners’ or shareholder’s investment in the business as a capital contribution. This account represents the shares that entitle the share owners to vote and their residual claim on the company’s assets. The value of common stock is equal to the par value of the shares times the number of shares outstanding. For example, 1 million shares with $1 of par value would result in $1 million of common share capital on the balance sheet.

#2 Preferred Stock

Preferred stock is quite similar to common stock. The preferred stock is a type of share that often has no voting rights, but is guaranteed a cumulative dividend. If the dividend is not paid in one year, then it will accumulate until paid off.

Example: A preferred share of a company is entitled to $5 cumulative dividends in a year. The company has declared a dividend this year but has not paid dividends for the past two years. The shareholder will receive $15 ($5/year x 3 years) in dividends this year.

#3 Contributed Surplus

Contributed Surplus represents any amount paid over the par value paid by investors for stocks purchases that have a par value. This account also holds different types of gains and losses resulting in the sale of shares, or other complex financial instruments.

Example: The company issues 100,000 $1 par value shares for $10 per share. $100,000 (100,000 shares x $1/share) goes to common stock, and the excess $900,000 (100,000 shares x ($10-$1)) goes to Contributed Surplus.

#4 Additional Paid-In Capital

Additional Paid-In Capital is another term for contributed surplus, the same as is described above.

#5 Retained Earnings

Retained Earnings is the portion of net income that is not paid out as dividends to shareholders but retained for reinvesting or to pay off future obligations.

#6 Other Comprehensive Income

Other comprehensive income is excluded from net income on the income statement and consists of income that has not been realized yet. For example, unrealized gains or losses on securities that have not yet been sold would be reflected in other comprehensive income. Once the securities are sold the gain/loss will then move into net income on the income statement.

#7 Treasury Stock (contra-equity account)

Treasury stock is a contra-equity account and represents the amount of common stock that the company has purchased back from the investors. This is reflected in the books as a deduction from total equity.

The retained earning annexure look like :

| Retained Earnings Statement | |||||||||||

| For the Year Ended Mar 31, 2019 | |||||||||||

| Retained earnings, Apr 1 | XXXX | ||||||||||

| Add: | Net Income | XXXX | |||||||||

| XXXX | |||||||||||

| Less: | Dividend Declared and Other | XXXX | |||||||||

| Retained earnings, Mar 31 | XXXX | ||||||||||

(c) Navigation on quickbooks software by following below steps :

Read step-by-step instructions

1.

Your Dashboard

As soon as you log in, you’ll see the most important information about your business on your Dashboard.

2.

Profit and Loss

On the dashboard, QuickBooks shows your profit and loss, how much you spent, your sales summary, and what people owe you.

3.

Create Your First Invoice

And if you need to add something, like a sale or an invoice, you can do that right here.

4.

Add with the Plus Menu

You can also create invoices, and just about anything else, from the plus menu.

5.

Using the Search Bar

Once you’ve created a bunch of invoices and cheques, you might need to find one. Click search and enter the cheque number, date or amount.

6.

The Left Navigation Bar

QuickBooks has lots of good stuff on the left navigation bar. Under Invoicing you can see your customers, sales, and products or services you’re selling for your business.

7.

Reports

You can also get to QuickBooks reports here on the left.

8.

The Gear Menu

One more place you can look for things is the gear icon at the top right. You probably won’t need to use these tools as often, but this is where you’ll find your company settings and profile information.

9.

Advanced Accounting Tools

This is where you can find advanced accounting tools like Reconcile, Budgeting and the Audit Log.

Conclusion -Yes, Its useful as it finds information about supplier and customer. We can fetch also our sales data , purchase data , ratio analysis on finger tips. and any other information we can find very quickly. There are lot of features built on the board like P&L,Income, Sales, Invoices , Bank accounts etc.

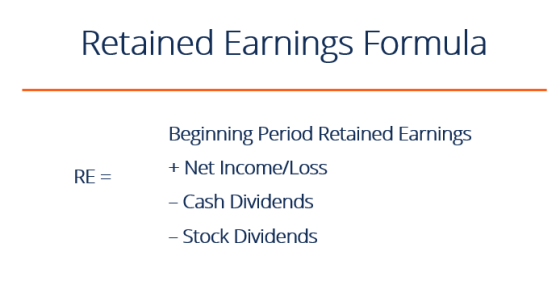

(d) Meaning- Retained Earnings (RE) are the portion of a business’s profits that are not distributed as dividends to shareholders but instead are reserved for reinvestment back into the business. Normally, these funds are used for working capital and fixed asset purchases (capital expenditures) or allotted for paying off debt obligations

Retained Earnings are reported on the balance sheet under the shareholder’s equity section at the end of each accounting period. To calculate RE, the beginning RE balance is added to the net income or loss and then dividend payouts are subtracted. A summary report called a statement of retained earnings is also maintained, outlining the changes in RE for a specific period

At the end of each accounting period, retained earnings are reported on the balance sheet as the accumulated income from the prior year (including the current year’s income), minus dividends paid to shareholders. In the next accounting cycle, the RE ending balance from the previous accounting period will now become the retained earnings beginning balance.

The RE balance may not always be a positive number as it may reflect that the current period’s net loss is greater than that of the RE beginning balance. Alternatively, a large distribution of dividends that exceed the retained earnings balance can cause it to go negative.

At the end of each accounting period, retained earnings are reported on the balance sheet as the accumulated income from the prior year (including the current year’s income), minus dividends paid to shareholders. In the next accounting cycle, the RE ending balance from the previous accounting period will now become the retained earnings beginning balance.

The RE balance may not always be a positive number as it may reflect that the current period’s net loss is greater than that of the RE beginning balance. Alternatively, a large distribution of dividends that exceed the retained earnings balance can cause it to go negative.

At the end of each accounting period, retained earnings are reported on the balance sheet as the accumulated income from the prior year (including the current year’s income), minus dividends paid to shareholders. In the next accounting cycle, the RE ending balance from the previous accounting period will now become the retained earnings beginning balance.

The RE balance may not always be a positive number as it may reflect that the current period’s net loss is greater than that of the RE beginning balance. Alternatively, a large distribution of dividends that exceed the retained earnings balance can cause it to go negative.

At the end of each accounting period, retained earnings are reported on the balance sheet as the accumulated income from the prior year (including the current year’s income), minus dividends paid to shareholders. In the next accounting cycle, the RE ending balance from the previous accounting period will now become the retained earnings beginning balance.

The RE balance may not always be a positive number as it may reflect that the current period’s net loss is greater than that of the RE beginning balance. Alternatively, a large distribution of dividends that exceed the retained earnings balance can cause it to go negative.

(e)

the bottom line of the income statement is net income. Net income links to both the balance sheet and cash flow statement.

In terms of the cash flow statement, net income is the first line as it is used to calculate cash flows from operations. Also, any non-cash expenses or non-cash income from the income statement (i.e., depreciation and amortization) flow into the cash flow statement and adjust net income to arrive at cash flow from operations.

In terms of the balance sheet, net income flows into stockholder’s equity via retained earnings. Retained earnings is equal to the previous period’s retained earnings plus net income from this period less dividends from this period.

Any balance sheet items that have a cash impact (i.e., working capital, financing, PP&E, etc.) are linked to the cash flow statement since it is either a source or use of cash. The net change in cash on the cash flow statement and cash from the previous period’s balance sheet comprise cash for this period.

(f) The three inventory accounts used by manufacturing companies are

- Raw Materials Inventory- Raw Materials Inventory includes materials used to manufacture a product.

- Work-in-Process Inventory- Work-in-Process Inventory includes goods that have been started in the manufacturing process but are not yet complete.

- Finished Goods Inventory- Finished Goods Inventory includes completed goods that have not yet been sold.

Let's take the example of Ford Motors Co., Each type of inventory should be classified In

(1) Raw material - Example are sheet metal, fiber, glasses and any other raw

(2) Work-In-Progress- Processing body, Job order inventory are in process , and assembly inventory

(3) Finished Inventory- New Car , Trucks, SUV and accessories

(4) Waste & Scrap- RM Scrap , WIP scrap etc

(5) Recyclable- RM and Other

Answer :

(a) Major Types of Business Organization are :

1. Sole Proprietorship

- It 's simple form of business entity.

- It 's easy to form or create

- It require only few formal accounting requirements.

- No separate tax forms; you file taxes on your own personal income tax return. You can easily exchange personal and business assets. This is how most bloggers and freelancers operate.

- Sole proprietors are personally liable for debts, obligations including lawsuits.

- Personal assets are essentially treated, for liability purposes, as assets of the business.

- Business income is reported on personal return, deductions expenses like medical insurance are limited to the caps and restrictions for individuals. Hence, these deductions are less favorable to take as personal expenses than as business expenses.

2. Partnership

- A partnership (sometimes called a “general partnership”) is also a simple form of business entity.

- All items of income and deductions pass through the partnership to the partners according to percentage of ownership or partnership agreement.

- Items are reported on each partner’s respective personal tax return.

- No income tax is paid at the partnership level (though a partnership may be subject to other state and local taxes).

- Personal and business assets are not separate, subject to the liabilities and obligations of the partnership.

- Availability of certain types of deductions are limited to the tax floors and ceilings on personal income tax return.

3. Limited Liability Partnership

- Similar to a general partnership. .

- each partner is not liable for obligations and liabilities arising from the “negligence, omissions, malpractice, wrongful acts or misconduct” of the other partners. In other words, so long as observance of the proper rules, liability is largely limited to partner own actions.

- Income and losses pass through to the partners either in proportion to ownership or according to your partnership agreement.

- It has limited liability for “negligence, malpractice, omissions, etc.

4. Limited Liability Company

- It’s a hybrid entity that offers the liability protection of a C corporation with the tax option to be treated as a partnership or a corporation.

- It can be structured to provide for added flexibility, including unlimited members.

- It provides ease of operation and possibilities for expansion which makes it attractive for a number of freelancers.

- Governed by an Operating Agreement, which outlines plans for business management. Banks, mortgage companies and other institutions will want to see company agreement when making loans or setting up accounts. The Operating Agreement also allows to set up the “control” of the corporation and limit the transfer of interests.

- keep personal assets separate from your business assets, liability will largely be limited to your business assets.

5. S corporation

- The S corporation is another special form of corporation that operates like a C corporation but is taxed like a partnership. There are strict limitations on the structure of an S corporation including the number and types of shareholders.

- One of the most attractive features of the S corporation is the ability to “slice up” distributions to shareholders and reclassify those distributions.

- Traditionally, compensation to shareholders who also served as owners was taxable as ordinary income. As compensation for services, it was also subject to self-employment tax, which is the self-employed person’s version of FICA (Social Security and Medicare contributions). The rate for self-employment tax is 15.3% of wages (the equivalent of the employer and employee portion of FICA). This tax is on top of the actual income tax on those wages. The result is a painful hit – the same as operating as a sole proprietor.

- It has a number of restrictions relating to ownership . for example, If you lose S status due to a reporting or management violation, the time period is generally ten years before you can regain your status. The default is that you would be treated as a C corporation, which likely not a good thing from a tax perspective.

6. C corporation

- A C corporation is what most people generally think of when they think of corporations – C corporations are the companies usually followed by “Inc” in their names, as in Coca Cola, Inc.

- The advantages of a C corporation are continuous life, clear divisibility of assets between personal and corporate, limited liability among shareholders, freely transferable shares of stock, virtually unlimited options on structuring stock ownership, and favorable tax treatment for certain expenses. All good, right?

- The disadvantages of a corporation are increased administrative expenses, compliance formalities and the potential for “double taxation.” Increased administrative expenses are due to more complicated accounting and tax compliance (i.e. filing corporate returns). “Double taxation” is the result of a C corporation being a separate taxable entity and not a pass through. This means that the C corporation pays a tax on its income for the corporate year and the shareholders pay tax on dividends received from the corporation. Additionally, money that is paid out as salary is reported as ordinary income and is subject to FICA (Social Security and Medicare taxes) on the employer and employee sides; in a one person corporation, this is largely the same result as paying self-employment taxes since it’s the same pot of money.

- In most cases, a C corporation is “overkill” for a freelancer with no immediate plans for expansion, hiring of employees, etc.

(b)

We can classify Equity Accounts in following types :

The main equity accounts are:

#1 Common Stock

Common stock represents the owners’ or shareholder’s investment in the business as a capital contribution. This account represents the shares that entitle the share owners to vote and their residual claim on the company’s assets. The value of common stock is equal to the par value of the shares times the number of shares outstanding. For example, 1 million shares with $1 of par value would result in $1 million of common share capital on the balance sheet.

#2 Preferred Stock

Preferred stock is quite similar to common stock. The preferred stock is a type of share that often has no voting rights, but is guaranteed a cumulative dividend. If the dividend is not paid in one year, then it will accumulate until paid off.

Example: A preferred share of a company is entitled to $5 cumulative dividends in a year. The company has declared a dividend this year but has not paid dividends for the past two years. The shareholder will receive $15 ($5/year x 3 years) in dividends this year.

#3 Contributed Surplus

Contributed Surplus represents any amount paid over the par value paid by investors for stocks purchases that have a par value. This account also holds different types of gains and losses resulting in the sale of shares, or other complex financial instruments.

Example: The company issues 100,000 $1 par value shares for $10 per share. $100,000 (100,000 shares x $1/share) goes to common stock, and the excess $900,000 (100,000 shares x ($10-$1)) goes to Contributed Surplus.

#4 Additional Paid-In Capital

Additional Paid-In Capital is another term for contributed surplus, the same as is described above.

#5 Retained Earnings

Retained Earnings is the portion of net income that is not paid out as dividends to shareholders but retained for reinvesting or to pay off future obligations.

#6 Other Comprehensive Income

Other comprehensive income is excluded from net income on the income statement and consists of income that has not been realized yet. For example, unrealized gains or losses on securities that have not yet been sold would be reflected in other comprehensive income. Once the securities are sold the gain/loss will then move into net income on the income statement.

#7 Treasury Stock (contra-equity account)

Treasury stock is a contra-equity account and represents the amount of common stock that the company has purchased back from the investors. This is reflected in the books as a deduction from total equity.

The retained earning annexure look like :

| Retained Earnings Statement | |||||||||||

| For the Year Ended Mar 31, 2019 | |||||||||||

| Retained earnings, Apr 1 | XXXX | ||||||||||

| Add: | Net Income | XXXX | |||||||||

| XXXX | |||||||||||

| Less: | Dividend Declared and Other | XXXX | |||||||||

| Retained earnings, Mar 31 | XXXX | ||||||||||

(c) Navigation on quickbooks software by following below steps :

Read step-by-step instructions

1.

Your Dashboard

As soon as you log in, you’ll see the most important information about your business on your Dashboard.

2.

Profit and Loss

On the dashboard, QuickBooks shows your profit and loss, how much you spent, your sales summary, and what people owe you.

3.

Create Your First Invoice

And if you need to add something, like a sale or an invoice, you can do that right here.

4.

Add with the Plus Menu

You can also create invoices, and just about anything else, from the plus menu.

5.

Using the Search Bar

Once you’ve created a bunch of invoices and cheques, you might need to find one. Click search and enter the cheque number, date or amount.

6.

The Left Navigation Bar

QuickBooks has lots of good stuff on the left navigation bar. Under Invoicing you can see your customers, sales, and products or services you’re selling for your business.

7.

Reports

You can also get to QuickBooks reports here on the left.

8.

The Gear Menu

One more place you can look for things is the gear icon at the top right. You probably won’t need to use these tools as often, but this is where you’ll find your company settings and profile information.

9.

Advanced Accounting Tools

This is where you can find advanced accounting tools like Reconcile, Budgeting and the Audit Log.

Conclusion -Yes, Its useful as it finds information about supplier and customer. We can fetch also our sales data , purchase data , ratio analysis on finger tips. and any other information we can find very quickly. There are lot of features built on the board like P&L,Income, Sales, Invoices , Bank accounts etc.

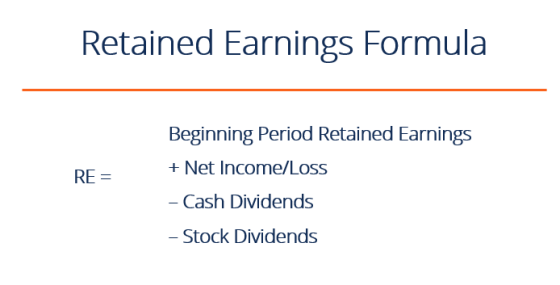

(d) Meaning- Retained Earnings (RE) are the portion of a business’s profits that are not distributed as dividends to shareholders but instead are reserved for reinvestment back into the business. Normally, these funds are used for working capital and fixed asset purchases (capital expenditures) or allotted for paying off debt obligations

Retained Earnings are reported on the balance sheet under the shareholder’s equity section at the end of each accounting period. To calculate RE, the beginning RE balance is added to the net income or loss and then dividend payouts are subtracted. A summary report called a statement of retained earnings is also maintained, outlining the changes in RE for a specific period

At the end of each accounting period, retained earnings are reported on the balance sheet as the accumulated income from the prior year (including the current year’s income), minus dividends paid to shareholders. In the next accounting cycle, the RE ending balance from the previous accounting period will now become the retained earnings beginning balance.

The RE balance may not always be a positive number as it may reflect that the current period’s net loss is greater than that of the RE beginning balance. Alternatively, a large distribution of dividends that exceed the retained earnings balance can cause it to go negative.

At the end of each accounting period, retained earnings are reported on the balance sheet as the accumulated income from the prior year (including the current year’s income), minus dividends paid to shareholders. In the next accounting cycle, the RE ending balance from the previous accounting period will now become the retained earnings beginning balance.

The RE balance may not always be a positive number as it may reflect that the current period’s net loss is greater than that of the RE beginning balance. Alternatively, a large distribution of dividends that exceed the retained earnings balance can cause it to go negative.

At the end of each accounting period, retained earnings are reported on the balance sheet as the accumulated income from the prior year (including the current year’s income), minus dividends paid to shareholders. In the next accounting cycle, the RE ending balance from the previous accounting period will now become the retained earnings beginning balance.

The RE balance may not always be a positive number as it may reflect that the current period’s net loss is greater than that of the RE beginning balance. Alternatively, a large distribution of dividends that exceed the retained earnings balance can cause it to go negative.

At the end of each accounting period, retained earnings are reported on the balance sheet as the accumulated income from the prior year (including the current year’s income), minus dividends paid to shareholders. In the next accounting cycle, the RE ending balance from the previous accounting period will now become the retained earnings beginning balance.

The RE balance may not always be a positive number as it may reflect that the current period’s net loss is greater than that of the RE beginning balance. Alternatively, a large distribution of dividends that exceed the retained earnings balance can cause it to go negative.

(e)

the bottom line of the income statement is net income. Net income links to both the balance sheet and cash flow statement.

In terms of the cash flow statement, net income is the first line as it is used to calculate cash flows from operations. Also, any non-cash expenses or non-cash income from the income statement (i.e., depreciation and amortization) flow into the cash flow statement and adjust net income to arrive at cash flow from operations.

In terms of the balance sheet, net income flows into stockholder’s equity via retained earnings. Retained earnings is equal to the previous period’s retained earnings plus net income from this period less dividends from this period.

Any balance sheet items that have a cash impact (i.e., working capital, financing, PP&E, etc.) are linked to the cash flow statement since it is either a source or use of cash. The net change in cash on the cash flow statement and cash from the previous period’s balance sheet comprise cash for this period.

(f) The three inventory accounts used by manufacturing companies are

- Raw Materials Inventory- Raw Materials Inventory includes materials used to manufacture a product.

- Work-in-Process Inventory- Work-in-Process Inventory includes goods that have been started in the manufacturing process but are not yet complete.

- Finished Goods Inventory- Finished Goods Inventory includes completed goods that have not yet been sold.

Let's take the example of Ford Motors Co., Each type of inventory should be classified In

(1) Raw material - Example are sheet metal, fiber, glasses and any other raw

(2) Work-In-Progress- Processing body, Job order inventory are in process , and assembly inventory

(3) Finished Inventory- New Car , Trucks, SUV and accessories

(4) Waste & Scrap- RM Scrap , WIP scrap etc

(5) Recyclable- RM and Other

Answer :

(a) Major Types of Business Organization are :

1. Sole Proprietorship

- It 's simple form of business entity.

- It 's easy to form or create

- It require only few formal accounting requirements.

- No separate tax forms; you file taxes on your own personal income tax return. You can easily exchange personal and business assets. This is how most bloggers and freelancers operate.

- Sole proprietors are personally liable for debts, obligations including lawsuits.

- Personal assets are essentially treated, for liability purposes, as assets of the business.

- Business income is reported on personal return, deductions expenses like medical insurance are limited to the caps and restrictions for individuals. Hence, these deductions are less favorable to take as personal expenses than as business expenses.

2. Partnership

- A partnership (sometimes called a “general partnership”) is also a simple form of business entity.

- All items of income and deductions pass through the partnership to the partners according to percentage of ownership or partnership agreement.

- Items are reported on each partner’s respective personal tax return.

- No income tax is paid at the partnership level (though a partnership may be subject to other state and local taxes).

- Personal and business assets are not separate, subject to the liabilities and obligations of the partnership.

- Availability of certain types of deductions are limited to the tax floors and ceilings on personal income tax return.

3. Limited Liability Partnership

- Similar to a general partnership. .

- each partner is not liable for obligations and liabilities arising from the “negligence, omissions, malpractice, wrongful acts or misconduct” of the other partners. In other words, so long as observance of the proper rules, liability is largely limited to partner own actions.

- Income and losses pass through to the partners either in proportion to ownership or according to your partnership agreement.

- It has limited liability for “negligence, malpractice, omissions, etc.

4. Limited Liability Company

- It’s a hybrid entity that offers the liability protection of a C corporation with the tax option to be treated as a partnership or a corporation.

- It can be structured to provide for added flexibility, including unlimited members.

- It provides ease of operation and possibilities for expansion which makes it attractive for a number of freelancers.

- Governed by an Operating Agreement, which outlines plans for business management. Banks, mortgage companies and other institutions will want to see company agreement when making loans or setting up accounts. The Operating Agreement also allows to set up the “control” of the corporation and limit the transfer of interests.

- keep personal assets separate from your business assets, liability will largely be limited to your business assets.

5. S corporation

- The S corporation is another special form of corporation that operates like a C corporation but is taxed like a partnership. There are strict limitations on the structure of an S corporation including the number and types of shareholders.

- One of the most attractive features of the S corporation is the ability to “slice up” distributions to shareholders and reclassify those distributions.

- Traditionally, compensation to shareholders who also served as owners was taxable as ordinary income. As compensation for services, it was also subject to self-employment tax, which is the self-employed person’s version of FICA (Social Security and Medicare contributions). The rate for self-employment tax is 15.3% of wages (the equivalent of the employer and employee portion of FICA). This tax is on top of the actual income tax on those wages. The result is a painful hit – the same as operating as a sole proprietor.

- It has a number of restrictions relating to ownership . for example, If you lose S status due to a reporting or management violation, the time period is generally ten years before you can regain your status. The default is that you would be treated as a C corporation, which likely not a good thing from a tax perspective.

6. C corporation

- A C corporation is what most people generally think of when they think of corporations – C corporations are the companies usually followed by “Inc” in their names, as in Coca Cola, Inc.

- The advantages of a C corporation are continuous life, clear divisibility of assets between personal and corporate, limited liability among shareholders, freely transferable shares of stock, virtually unlimited options on structuring stock ownership, and favorable tax treatment for certain expenses. All good, right?

- The disadvantages of a corporation are increased administrative expenses, compliance formalities and the potential for “double taxation.” Increased administrative expenses are due to more complicated accounting and tax compliance (i.e. filing corporate returns). “Double taxation” is the result of a C corporation being a separate taxable entity and not a pass through. This means that the C corporation pays a tax on its income for the corporate year and the shareholders pay tax on dividends received from the corporation. Additionally, money that is paid out as salary is reported as ordinary income and is subject to FICA (Social Security and Medicare taxes) on the employer and employee sides; in a one person corporation, this is largely the same result as paying self-employment taxes since it’s the same pot of money.

- In most cases, a C corporation is “overkill” for a freelancer with no immediate plans for expansion, hiring of employees, etc.

(b)

We can classify Equity Accounts in following types :

The main equity accounts are:

#1 Common Stock

Common stock represents the owners’ or shareholder’s investment in the business as a capital contribution. This account represents the shares that entitle the share owners to vote and their residual claim on the company’s assets. The value of common stock is equal to the par value of the shares times the number of shares outstanding. For example, 1 million shares with $1 of par value would result in $1 million of common share capital on the balance sheet.

#2 Preferred Stock

Preferred stock is quite similar to common stock. The preferred stock is a type of share that often has no voting rights, but is guaranteed a cumulative dividend. If the dividend is not paid in one year, then it will accumulate until paid off.

Example: A preferred share of a company is entitled to $5 cumulative dividends in a year. The company has declared a dividend this year but has not paid dividends for the past two years. The shareholder will receive $15 ($5/year x 3 years) in dividends this year.

#3 Contributed Surplus

Contributed Surplus represents any amount paid over the par value paid by investors for stocks purchases that have a par value. This account also holds different types of gains and losses resulting in the sale of shares, or other complex financial instruments.

Example: The company issues 100,000 $1 par value shares for $10 per share. $100,000 (100,000 shares x $1/share) goes to common stock, and the excess $900,000 (100,000 shares x ($10-$1)) goes to Contributed Surplus.

#4 Additional Paid-In Capital

Additional Paid-In Capital is another term for contributed surplus, the same as is described above.

#5 Retained Earnings

Retained Earnings is the portion of net income that is not paid out as dividends to shareholders but retained for reinvesting or to pay off future obligations.

#6 Other Comprehensive Income

Other comprehensive income is excluded from net income on the income statement and consists of income that has not been realized yet. For example, unrealized gains or losses on securities that have not yet been sold would be reflected in other comprehensive income. Once the securities are sold the gain/loss will then move into net income on the income statement.

#7 Treasury Stock (contra-equity account)

Treasury stock is a contra-equity account and represents the amount of common stock that the company has purchased back from the investors. This is reflected in the books as a deduction from total equity.

The retained earning annexure look like :

| Retained Earnings Statement | |||||||||||

| For the Year Ended Mar 31, 2019 | |||||||||||

| Retained earnings, Apr 1 | XXXX | ||||||||||

| Add: | Net Income | XXXX | |||||||||

| XXXX | |||||||||||

| Less: | Dividend Declared and Other | XXXX | |||||||||

| Retained earnings, Mar 31 | XXXX | ||||||||||

(c) Navigation on quickbooks software by following below steps :

Read step-by-step instructions

1.

Your Dashboard

As soon as you log in, you’ll see the most important information about your business on your Dashboard.

2.

Profit and Loss

On the dashboard, QuickBooks shows your profit and loss, how much you spent, your sales summary, and what people owe you.

3.

Create Your First Invoice

And if you need to add something, like a sale or an invoice, you can do that right here.

4.

Add with the Plus Menu

You can also create invoices, and just about anything else, from the plus menu.

5.

Using the Search Bar

Once you’ve created a bunch of invoices and cheques, you might need to find one. Click search and enter the cheque number, date or amount.

6.

The Left Navigation Bar

QuickBooks has lots of good stuff on the left navigation bar. Under Invoicing you can see your customers, sales, and products or services you’re selling for your business.

7.

Reports

You can also get to QuickBooks reports here on the left.

8.

The Gear Menu

One more place you can look for things is the gear icon at the top right. You probably won’t need to use these tools as often, but this is where you’ll find your company settings and profile information.

9.

Advanced Accounting Tools

This is where you can find advanced accounting tools like Reconcile, Budgeting and the Audit Log.

Conclusion -Yes, Its useful as it finds information about supplier and customer. We can fetch also our sales data , purchase data , ratio analysis on finger tips. and any other information we can find very quickly. There are lot of features built on the board like P&L,Income, Sales, Invoices , Bank accounts etc.

(d) Meaning- Retained Earnings (RE) are the portion of a business’s profits that are not distributed as dividends to shareholders but instead are reserved for reinvestment back into the business. Normally, these funds are used for working capital and fixed asset purchases (capital expenditures) or allotted for paying off debt obligations

Retained Earnings are reported on the balance sheet under the shareholder’s equity section at the end of each accounting period. To calculate RE, the beginning RE balance is added to the net income or loss and then dividend payouts are subtracted. A summary report called a statement of retained earnings is also maintained, outlining the changes in RE for a specific period

At the end of each accounting period, retained earnings are reported on the balance sheet as the accumulated income from the prior year (including the current year’s income), minus dividends paid to shareholders. In the next accounting cycle, the RE ending balance from the previous accounting period will now become the retained earnings beginning balance.

The RE balance may not always be a positive number as it may reflect that the current period’s net loss is greater than that of the RE beginning balance. Alternatively, a large distribution of dividends that exceed the retained earnings balance can cause it to go negative.

At the end of each accounting period, retained earnings are reported on the balance sheet as the accumulated income from the prior year (including the current year’s income), minus dividends paid to shareholders. In the next accounting cycle, the RE ending balance from the previous accounting period will now become the retained earnings beginning balance.

The RE balance may not always be a positive number as it may reflect that the current period’s net loss is greater than that of the RE beginning balance. Alternatively, a large distribution of dividends that exceed the retained earnings balance can cause it to go negative.

At the end of each accounting period, retained earnings are reported on the balance sheet as the accumulated income from the prior year (including the current year’s income), minus dividends paid to shareholders. In the next accounting cycle, the RE ending balance from the previous accounting period will now become the retained earnings beginning balance.

The RE balance may not always be a positive number as it may reflect that the current period’s net loss is greater than that of the RE beginning balance. Alternatively, a large distribution of dividends that exceed the retained earnings balance can cause it to go negative.

At the end of each accounting period, retained earnings are reported on the balance sheet as the accumulated income from the prior year (including the current year’s income), minus dividends paid to shareholders. In the next accounting cycle, the RE ending balance from the previous accounting period will now become the retained earnings beginning balance.

The RE balance may not always be a positive number as it may reflect that the current period’s net loss is greater than that of the RE beginning balance. Alternatively, a large distribution of dividends that exceed the retained earnings balance can cause it to go negative.

(e)

the bottom line of the income statement is net income. Net income links to both the balance sheet and cash flow statement.

In terms of the cash flow statement, net income is the first line as it is used to calculate cash flows from operations. Also, any non-cash expenses or non-cash income from the income statement (i.e., depreciation and amortization) flow into the cash flow statement and adjust net income to arrive at cash flow from operations.

In terms of the balance sheet, net income flows into stockholder’s equity via retained earnings. Retained earnings is equal to the previous period’s retained earnings plus net income from this period less dividends from this period.

Any balance sheet items that have a cash impact (i.e., working capital, financing, PP&E, etc.) are linked to the cash flow statement since it is either a source or use of cash. The net change in cash on the cash flow statement and cash from the previous period’s balance sheet comprise cash for this period.

(f) The three inventory accounts used by manufacturing companies are

- Raw Materials Inventory- Raw Materials Inventory includes materials used to manufacture a product.

- Work-in-Process Inventory- Work-in-Process Inventory includes goods that have been started in the manufacturing process but are not yet complete.

- Finished Goods Inventory- Finished Goods Inventory includes completed goods that have not yet been sold.

Let's take the example of Ford Motors Co., Each type of inventory should be classified In

(1) Raw material - Example are sheet metal, fiber, glasses and any other raw

(2) Work-In-Progress- Processing body, Job order inventory are in process , and assembly inventory

(3) Finished Inventory- New Car , Trucks, SUV and accessories

(4) Waste & Scrap- RM Scrap , WIP scrap etc

(5) Recyclable- RM and Other

Answer :

(a) Major Types of Business Organization are :

1. Sole Proprietorship

- It 's simple form of business entity.

- It 's easy to form or create

- It require only few formal accounting requirements.

- No separate tax forms; you file taxes on your own personal income tax return. You can easily exchange personal and business assets. This is how most bloggers and freelancers operate.

- Sole proprietors are personally liable for debts, obligations including lawsuits.

- Personal assets are essentially treated, for liability purposes, as assets of the business.

- Business income is reported on personal return, deductions expenses like medical insurance are limited to the caps and restrictions for individuals. Hence, these deductions are less favorable to take as personal expenses than as business expenses.

2. Partnership

- A partnership (sometimes called a “general partnership”) is also a simple form of business entity.

- All items of income and deductions pass through the partnership to the partners according to percentage of ownership or partnership agreement.

- Items are reported on each partner’s respective personal tax return.

- No income tax is paid at the partnership level (though a partnership may be subject to other state and local taxes).

- Personal and business assets are not separate, subject to the liabilities and obligations of the partnership.

- Availability of certain types of deductions are limited to the tax floors and ceilings on personal income tax return.

3. Limited Liability Partnership

- Similar to a general partnership. .

- each partner is not liable for obligations and liabilities arising from the “negligence, omissions, malpractice, wrongful acts or misconduct” of the other partners. In other words, so long as observance of the proper rules, liability is largely limited to partner own actions.

- Income and losses pass through to the partners either in proportion to ownership or according to your partnership agreement.

- It has limited liability for “negligence, malpractice, omissions, etc.

4. Limited Liability Company

- It’s a hybrid entity that offers the liability protection of a C corporation with the tax option to be treated as a partnership or a corporation.

- It can be structured to provide for added flexibility, including unlimited members.

- It provides ease of operation and possibilities for expansion which makes it attractive for a number of freelancers.

- Governed by an Operating Agreement, which outlines plans for business management. Banks, mortgage companies and other institutions will want to see company agreement when making loans or setting up accounts. The Operating Agreement also allows to set up the “control” of the corporation and limit the transfer of interests.

- keep personal assets separate from your business assets, liability will largely be limited to your business assets.

5. S corporation

- The S corporation is another special form of corporation that operates like a C corporation but is taxed like a partnership. There are strict limitations on the structure of an S corporation including the number and types of shareholders.

- One of the most attractive features of the S corporation is the ability to “slice up” distributions to shareholders and reclassify those distributions.

- Traditionally, compensation to shareholders who also served as owners was taxable as ordinary income. As compensation for services, it was also subject to self-employment tax, which is the self-employed person’s version of FICA (Social Security and Medicare contributions). The rate for self-employment tax is 15.3% of wages (the equivalent of the employer and employee portion of FICA). This tax is on top of the actual income tax on those wages. The result is a painful hit – the same as operating as a sole proprietor.

- It has a number of restrictions relating to ownership . for example, If you lose S status due to a reporting or management violation, the time period is generally ten years before you can regain your status. The default is that you would be treated as a C corporation, which likely not a good thing from a tax perspective.

6. C corporation

- A C corporation is what most people generally think of when they think of corporations – C corporations are the companies usually followed by “Inc” in their names, as in Coca Cola, Inc.

- The advantages of a C corporation are continuous life, clear divisibility of assets between personal and corporate, limited liability among shareholders, freely transferable shares of stock, virtually unlimited options on structuring stock ownership, and favorable tax treatment for certain expenses. All good, right?

- The disadvantages of a corporation are increased administrative expenses, compliance formalities and the potential for “double taxation.” Increased administrative expenses are due to more complicated accounting and tax compliance (i.e. filing corporate returns). “Double taxation” is the result of a C corporation being a separate taxable entity and not a pass through. This means that the C corporation pays a tax on its income for the corporate year and the shareholders pay tax on dividends received from the corporation. Additionally, money that is paid out as salary is reported as ordinary income and is subject to FICA (Social Security and Medicare taxes) on the employer and employee sides; in a one person corporation, this is largely the same result as paying self-employment taxes since it’s the same pot of money.

- In most cases, a C corporation is “overkill” for a freelancer with no immediate plans for expansion, hiring of employees, etc.

(b)

We can classify Equity Accounts in following types :

The main equity accounts are:

#1 Common Stock

Common stock represents the owners’ or shareholder’s investment in the business as a capital contribution. This account represents the shares that entitle the share owners to vote and their residual claim on the company’s assets. The value of common stock is equal to the par value of the shares times the number of shares outstanding. For example, 1 million shares with $1 of par value would result in $1 million of common share capital on the balance sheet.

#2 Preferred Stock

Preferred stock is quite similar to common stock. The preferred stock is a type of share that often has no voting rights, but is guaranteed a cumulative dividend. If the dividend is not paid in one year, then it will accumulate until paid off.

Example: A preferred share of a company is entitled to $5 cumulative dividends in a year. The company has declared a dividend this year but has not paid dividends for the past two years. The shareholder will receive $15 ($5/year x 3 years) in dividends this year.

#3 Contributed Surplus

Contributed Surplus represents any amount paid over the par value paid by investors for stocks purchases that have a par value. This account also holds different types of gains and losses resulting in the sale of shares, or other complex financial instruments.

Example: The company issues 100,000 $1 par value shares for $10 per share. $100,000 (100,000 shares x $1/share) goes to common stock, and the excess $900,000 (100,000 shares x ($10-$1)) goes to Contributed Surplus.

#4 Additional Paid-In Capital

Additional Paid-In Capital is another term for contributed surplus, the same as is described above.

#5 Retained Earnings

Retained Earnings is the portion of net income that is not paid out as dividends to shareholders but retained for reinvesting or to pay off future obligations.

#6 Other Comprehensive Income

Other comprehensive income is excluded from net income on the income statement and consists of income that has not been realized yet. For example, unrealized gains or losses on securities that have not yet been sold would be reflected in other comprehensive income. Once the securities are sold the gain/loss will then move into net income on the income statement.

#7 Treasury Stock (contra-equity account)

Treasury stock is a contra-equity account and represents the amount of common stock that the company has purchased back from the investors. This is reflected in the books as a deduction from total equity.

The retained earning annexure look like :

| Retained Earnings Statement | |||||||||||

| For the Year Ended Mar 31, 2019 | |||||||||||

| Retained earnings, Apr 1 | XXXX | ||||||||||

| Add: | Net Income | XXXX | |||||||||

| XXXX | |||||||||||

| Less: | Dividend Declared and Other | XXXX | |||||||||

| Retained earnings, Mar 31 | XXXX | ||||||||||

(c) Navigation on quickbooks software by following below steps :

Read step-by-step instructions

1.

Your Dashboard

As soon as you log in, you’ll see the most important information about your business on your Dashboard.

2.

Profit and Loss

On the dashboard, QuickBooks shows your profit and loss, how much you spent, your sales summary, and what people owe you.

3.

Create Your First Invoice

And if you need to add something, like a sale or an invoice, you can do that right here.

4.

Add with the Plus Menu

You can also create invoices, and just about anything else, from the plus menu.

5.

Using the Search Bar

Once you’ve created a bunch of invoices and cheques, you might need to find one. Click search and enter the cheque number, date or amount.

6.

The Left Navigation Bar

QuickBooks has lots of good stuff on the left navigation bar. Under Invoicing you can see your customers, sales, and products or services you’re selling for your business.

7.

Reports

You can also get to QuickBooks reports here on the left.

8.

The Gear Menu

One more place you can look for things is the gear icon at the top right. You probably won’t need to use these tools as often, but this is where you’ll find your company settings and profile information.

9.

Advanced Accounting Tools

This is where you can find advanced accounting tools like Reconcile, Budgeting and the Audit Log.

Conclusion -Yes, Its useful as it finds information about supplier and customer. We can fetch also our sales data , purchase data , ratio analysis on finger tips. and any other information we can find very quickly. There are lot of features built on the board like P&L,Income, Sales, Invoices , Bank accounts etc.

(d) Meaning- Retained Earnings (RE) are the portion of a business’s profits that are not distributed as dividends to shareholders but instead are reserved for reinvestment back into the business. Normally, these funds are used for working capital and fixed asset purchases (capital expenditures) or allotted for paying off debt obligations

Retained Earnings are reported on the balance sheet under the shareholder’s equity section at the end of each accounting period. To calculate RE, the beginning RE balance is added to the net income or loss and then dividend payouts are subtracted. A summary report called a statement of retained earnings is also maintained, outlining the changes in RE for a specific period

At the end of each accounting period, retained earnings are reported on the balance sheet as the accumulated income from the prior year (including the current year’s income), minus dividends paid to shareholders. In the next accounting cycle, the RE ending balance from the previous accounting period will now become the retained earnings beginning balance.

The RE balance may not always be a positive number as it may reflect that the current period’s net loss is greater than that of the RE beginning balance. Alternatively, a large distribution of dividends that exceed the retained earnings balance can cause it to go negative.

At the end of each accounting period, retained earnings are reported on the balance sheet as the accumulated income from the prior year (including the current year’s income), minus dividends paid to shareholders. In the next accounting cycle, the RE ending balance from the previous accounting period will now become the retained earnings beginning balance.

The RE balance may not always be a positive number as it may reflect that the current period’s net loss is greater than that of the RE beginning balance. Alternatively, a large distribution of dividends that exceed the retained earnings balance can cause it to go negative.

At the end of each accounting period, retained earnings are reported on the balance sheet as the accumulated income from the prior year (including the current year’s income), minus dividends paid to shareholders. In the next accounting cycle, the RE ending balance from the previous accounting period will now become the retained earnings beginning balance.

The RE balance may not always be a positive number as it may reflect that the current period’s net loss is greater than that of the RE beginning balance. Alternatively, a large distribution of dividends that exceed the retained earnings balance can cause it to go negative.

At the end of each accounting period, retained earnings are reported on the balance sheet as the accumulated income from the prior year (including the current year’s income), minus dividends paid to shareholders. In the next accounting cycle, the RE ending balance from the previous accounting period will now become the retained earnings beginning balance.

The RE balance may not always be a positive number as it may reflect that the current period’s net loss is greater than that of the RE beginning balance. Alternatively, a large distribution of dividends that exceed the retained earnings balance can cause it to go negative.

(e)

the bottom line of the income statement is net income. Net income links to both the balance sheet and cash flow statement.

In terms of the cash flow statement, net income is the first line as it is used to calculate cash flows from operations. Also, any non-cash expenses or non-cash income from the income statement (i.e., depreciation and amortization) flow into the cash flow statement and adjust net income to arrive at cash flow from operations.

In terms of the balance sheet, net income flows into stockholder’s equity via retained earnings. Retained earnings is equal to the previous period’s retained earnings plus net income from this period less dividends from this period.

Any balance sheet items that have a cash impact (i.e., working capital, financing, PP&E, etc.) are linked to the cash flow statement since it is either a source or use of cash. The net change in cash on the cash flow statement and cash from the previous period’s balance sheet comprise cash for this period.

(f) The three inventory accounts used by manufacturing companies are

- Raw Materials Inventory- Raw Materials Inventory includes materials used to manufacture a product.

- Work-in-Process Inventory- Work-in-Process Inventory includes goods that have been started in the manufacturing process but are not yet complete.

- Finished Goods Inventory- Finished Goods Inventory includes completed goods that have not yet been sold.