Explain how to account for held-to-maturity debt securities at and after acquisition and how they are...

Explain how to account for held-to-maturity debt securities at and after acquisition and how they are reported in the financial statements.

Homework Answers

Held to maturity securities are securities that companies purchase and intend to hold until they mature. Unlike with trading securities or available for sale securities, companies don’t usually hold on to securities until they reach maturity to realize a large capital gain. Rather, companies mostly use the investments to protect themselves against interest rate fluctuations, diversify their investment portfolios, and realize a small, low-risk capital gain over a longer period of time. Held to maturity securities are usually debt instruments such as government or corporate bonds.

Accounting Treatment

The biggest difference between held to maturity securities and the other security types mentioned above is in their accounting treatment. As opposed to being recorded and updated on the company’s balance sheet according to the security’s fair market value, held to maturity securities are recorded at their original purchase cost. It means that from one accounting period to another, the value of the securities on the company’s balance sheet will remain constant.

Any gains or losses resulting from changes in interest rates (for bonds and other debt instruments) will be recorded when the securities reach maturity. Below is an example of how a 2-year bond will appear on a company’s balance sheet:

Upon purchase, the offsetting account will likely be cash, as the company likely bought the securities with cash. Here, we can see that no changes are recorded in the 2017 accounting period, despite any changes in the fair value of the security during that time period. For instance, if interest rates fell sharply in 2016, which would cause a rise in the market value of the bond, there would be no account of this in the company’s balance sheet.

In 2018, when the bond matured, we see that a capital gain of $500 million has occurred as a result of sliding interest rates. This is the only time that any changes in the price of the security will be recorded.

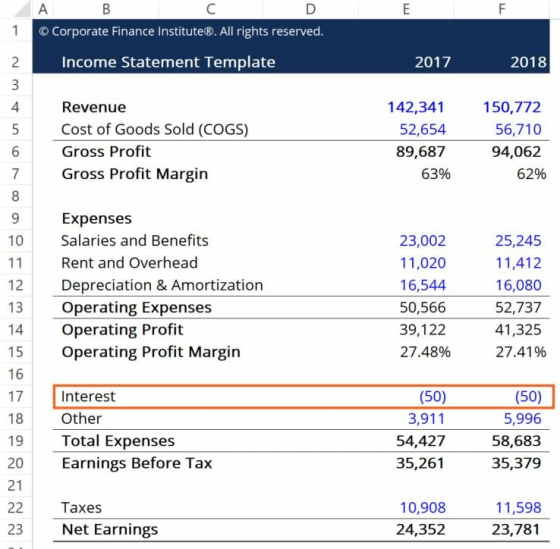

Interest payments made to the debt-holding company will appear in the company’s income statement on a periodic basis. Let’s assume that the bonds pay a 10% annual coupon rate, which equates to $50 million in additional income each year. Here’s how this would look on a company’s income statemepayments

Here, we can see how the 10% coupon is captured in the interest line item. For simplicity, it is assumed that the company does not have any other interest revenues or obligations to its financiers. Thus, the interest from coupon payments is recorded as a negative number since the “interest” account assumes that companies will usually have to make more interest payments than receive coupon payments

Add Answer to:

Explain how to account for held-to-maturity debt securities at

and after acquisition and how they are...

In footnotes to its 2016 annual report, Bancfirst Corp. reported that held-to-maturity debt securities with an...

In footnotes to its 2016 annual report, Bancfirst Corp. reported that held-to-maturity debt securities with an amortized cost of $4,365 thousand had an estimated fair value of $4,403 thousand. a. What amount does Bancfirst report on its 2016 balance sheet for these held-to-maturity securities? b. If these debt securities had instead been classified as available-for-sale securities, how would Bancfirst’s pretax income have been affected

Which of the following statement(s) is (are) true about reporting held to maturity securities? I. Investments...

Which of the following statement(s) is (are) true about reporting held to maturity securities? I. Investments in debt securities that are classified as held to maturity are reported at amortized cost. II. Interest revenue on debt securities that are classified as held to maturity are recognized as other comprehensive income. III. The market value of investments in debt securities that are classified as held to maturity must be disclosed. a. I and II b. I and III c. I, II,...

Long-term investments cannot include: Multiple Choice Held-to-maturity debt securities. Securities with maturity dates within three months....

Long-term investments cannot include: Multiple Choice Held-to-maturity debt securities. Securities with maturity dates within three months. Equity securities giving an investor insignificant influence over an investee. Equity securities giving an investor significant influence over an investee. Available-for-sale debt securities.

Chapter 1 Intercorporate Investments: An Overview Held-to-maturity securities are recorded at amortized cost which approximates fair...

Chapter 1 Intercorporate Investments: An Overview Held-to-maturity securities are recorded at amortized cost which approximates fair market value. The Company evaluates whether the decline in fair value of its investments is other-than-temporary at each quarter-end. This evaluation consists of a review by management, and includes market pri information and maturity dates for the securities held, market and economic trends in the industry and information on the issuer's financial condition and, if applicable, information on the guarantors financial condition. Factors considered...

Chapter 1 Intercorporate Investments: An Overview Held-to-maturity securities are recorded at amortized cost which approximates fair market value. The Company evaluates whether the decline in fair value of its investments is other-than-temporary at each quarter-end. This evaluation consists of a review by management, and includes market pri information and maturity dates for the securities held, market and economic trends in the industry and information on the issuer's financial condition and, if applicable, information on the guarantors financial condition. Factors considered...

Accounting for Debt Securities- Held-to-Maturity Kurl Company had the following transactuons and adjustments related to a...

Accounting for Debt Securities- Held-to-Maturity

Kurl Company had the following transactuons and adjustments

related to a bond investment:

Accounting for Debt Securities-Held-to-Maturity Kurl Company had the following transactions and adjustments related to a bond investment: 2016 Jan. Purchased $600,000 face value of Sphere, Inc.'s 9 percent bonds at 102 plus a brokerage commission of $900. The bonds pay interest on June 30 1 and December 31 and mature in 10 years. Kuri expects to hold the bonds to maturity. June...

Accounting for Debt Securities- Held-to-Maturity

Kurl Company had the following transactuons and adjustments

related to a bond investment:

Accounting for Debt Securities-Held-to-Maturity Kurl Company had the following transactions and adjustments related to a bond investment: 2016 Jan. Purchased $600,000 face value of Sphere, Inc.'s 9 percent bonds at 102 plus a brokerage commission of $900. The bonds pay interest on June 30 1 and December 31 and mature in 10 years. Kuri expects to hold the bonds to maturity. June...

14. An example of securities which could be classified as held-to-maturity are A) preferred stock B)...

14. An example of securities which could be classified as held-to-maturity are A) preferred stock B) warrants. C) municipal bonds D) treasury stock 15. Which set of accounting principles require use of the equity method if a company owns between 20% and 50% A) GAAP B) IFRS. C) Neither A nor B. D) Both A and B. 16. A requirement for a security to be classified as held-to-maturity is A) ability to hold the security to maturity. B) positive intent....

14. An example of securities which could be classified as held-to-maturity are A) preferred stock B) warrants. C) municipal bonds D) treasury stock 15. Which set of accounting principles require use of the equity method if a company owns between 20% and 50% A) GAAP B) IFRS. C) Neither A nor B. D) Both A and B. 16. A requirement for a security to be classified as held-to-maturity is A) ability to hold the security to maturity. B) positive intent....

When selecting the appropriate accounting for held-to-maturity securities, a company must never sell the equity instrum...

When selecting the appropriate accounting for held-to-maturity securities, a company must never sell the equity instrument before maturity never sell the debt instrument before maturity intend and be able to hold the equity investment to maturity have the intent and ability to hold the debt instrument to maturity

When selecting the appropriate accounting for held-to-maturity securities, a company must never sell the equity instrument before maturity never sell the debt instrument before maturity intend and be able to hold the...

When selecting the appropriate accounting for held-to-maturity securities, a company must never sell the equity instrument before maturity never sell the debt instrument before maturity intend and be able to hold the equity investment to maturity have the intent and ability to hold the debt instrument to maturity

When selecting the appropriate accounting for held-to-maturity securities, a company must never sell the equity instrument before maturity never sell the debt instrument before maturity intend and be able to hold the...

What are the differences between trading securities, Held to Maturity Securities and Available for Sale securities?...

What are the differences between trading securities, Held to Maturity Securities and Available for Sale securities? Can you give examples of each?

A held-to-maturity debt investment with a book value of $6,000,000 is determined to be impaired due...

A held-to-maturity debt investment with a book value of $6,000,000 is determined to be impaired due to concerns about the investee's ability to pay principal and interest. The investment's current market value is $4,000,000. Assume the bonds were originally sold at par. Which statement is true? A. $2,000,000 loss is reported in income. B. $2,000,000 loss is reported in OCI. C. No loss is reported. D. The investment account is directly reduced by $2,000,000.

Aviation Inc. purchased securities on 1/1/2019 that would initially be accounted for in the financial statements...

Aviation Inc. purchased securities on 1/1/2019 that would initially be accounted for in the financial statements as an investment held-to-maturity. Held to Maturity Securities: Cost 1/1/2019 Fair Market Value 12/31/2019 Bronx Co. Bonds $ 300,000 $ 278,000 At 12/31/2019, Aviation Inc. decided that they would sale the bond within 90 days. Assume that Aviation now has to adjust their financial statements and account for the investment as available for sale. Write a memo detailing the impact that the change will...

Chapter 1 Intercorporate Investments: An Overview Held-to-maturity securities are recorded at amortized cost which approximates fair market value. The Company evaluates whether the decline in fair value of its investments is other-than-temporary at each quarter-end. This evaluation consists of a review by management, and includes market pri information and maturity dates for the securities held, market and economic trends in the industry and information on the issuer's financial condition and, if applicable, information on the guarantors financial condition. Factors considered...

Chapter 1 Intercorporate Investments: An Overview Held-to-maturity securities are recorded at amortized cost which approximates fair market value. The Company evaluates whether the decline in fair value of its investments is other-than-temporary at each quarter-end. This evaluation consists of a review by management, and includes market pri information and maturity dates for the securities held, market and economic trends in the industry and information on the issuer's financial condition and, if applicable, information on the guarantors financial condition. Factors considered...

Accounting for Debt Securities- Held-to-Maturity

Kurl Company had the following transactuons and adjustments

related to a bond investment:

Accounting for Debt Securities-Held-to-Maturity Kurl Company had the following transactions and adjustments related to a bond investment: 2016 Jan. Purchased $600,000 face value of Sphere, Inc.'s 9 percent bonds at 102 plus a brokerage commission of $900. The bonds pay interest on June 30 1 and December 31 and mature in 10 years. Kuri expects to hold the bonds to maturity. June...

Accounting for Debt Securities- Held-to-Maturity

Kurl Company had the following transactuons and adjustments

related to a bond investment:

Accounting for Debt Securities-Held-to-Maturity Kurl Company had the following transactions and adjustments related to a bond investment: 2016 Jan. Purchased $600,000 face value of Sphere, Inc.'s 9 percent bonds at 102 plus a brokerage commission of $900. The bonds pay interest on June 30 1 and December 31 and mature in 10 years. Kuri expects to hold the bonds to maturity. June...

14. An example of securities which could be classified as held-to-maturity are A) preferred stock B) warrants. C) municipal bonds D) treasury stock 15. Which set of accounting principles require use of the equity method if a company owns between 20% and 50% A) GAAP B) IFRS. C) Neither A nor B. D) Both A and B. 16. A requirement for a security to be classified as held-to-maturity is A) ability to hold the security to maturity. B) positive intent....

14. An example of securities which could be classified as held-to-maturity are A) preferred stock B) warrants. C) municipal bonds D) treasury stock 15. Which set of accounting principles require use of the equity method if a company owns between 20% and 50% A) GAAP B) IFRS. C) Neither A nor B. D) Both A and B. 16. A requirement for a security to be classified as held-to-maturity is A) ability to hold the security to maturity. B) positive intent....

When selecting the appropriate accounting for held-to-maturity securities, a company must never sell the equity instrument before maturity never sell the debt instrument before maturity intend and be able to hold the equity investment to maturity have the intent and ability to hold the debt instrument to maturity

When selecting the appropriate accounting for held-to-maturity securities, a company must never sell the equity instrument before maturity never sell the debt instrument before maturity intend and be able to hold the...

When selecting the appropriate accounting for held-to-maturity securities, a company must never sell the equity instrument before maturity never sell the debt instrument before maturity intend and be able to hold the equity investment to maturity have the intent and ability to hold the debt instrument to maturity

When selecting the appropriate accounting for held-to-maturity securities, a company must never sell the equity instrument before maturity never sell the debt instrument before maturity intend and be able to hold the...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 10 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 10 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 10 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 10 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 10 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 10 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 10 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 10 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 10 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 10 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 10 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 10 months ago