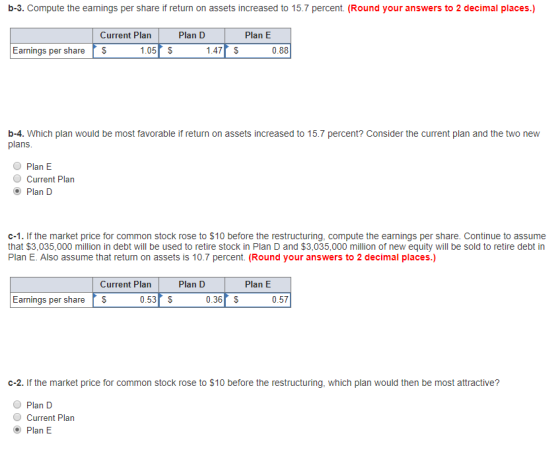

b-3. Compute the earnings per share if return on assets increased to 15.7 percent. Round your answers to 2 decimal places.) Plan D Plan E Current Plan Earnings per share$ 1.05 $ 1.47 $ 0.88 b-4. Which plan would be most favorable if return on assets increased to 15.7 percent? Consider the current plan and the two new plans O Plan E Current Plan O Plan D c-1. If the market price for common stock rose to $10 before the restructuring, compute the earnings per share. Continue to assume that $3,035,000 million in debt will be used to retire stock in Plan D and $3,035,000 million of new equity will be sold to retire debt in Plan E. Also assume that return on assets is 10.7 percent. (Round your answers to 2 decimal places.) Plan D Current Plan Plan E Earnings per share$ 0.53$ 0.36S 0.57 c-2. If the market price for common stock rose to $10 before the restructuring, which plan would then be most attractive? Plan D O Current Plan Plan E

Homework Answers

| a | How would each of the plans affect the earnings per share ? Consider the current plan and two new plans | |||||||

| Dickinson Company | ||||||||

| Income Statement | ||||||||

| Particulars | Current Plan | Plan D | Plan E | |||||

| EBIT-12140000*10.7% | 1298980 | 1298980 | 1298980 | |||||

| Less Interest -Old-12140000/2*10.7% | 649490 | 649490 | 324745 | |||||

| New-3035000*12.7% | 385445 | |||||||

| EBT | 649490 | 264045 | 974235 | |||||

| Less Taxes -40% | 259796 | 105618 | 389694 | |||||

| EAT | 389694 | 158427 | 584541 | |||||

| Common Shares | 758750 | 379375 | 1138125 | |||||

| EPS | 0.5136 | 0.4176 | 0.5136 | |||||

| Calculation of Common Shares | ||||||||

| Existing | 12140000/2 | |||||||

| Equity | 6070000 | |||||||

| Par value of share | $8 | |||||||

| No of common shares | 758,750 | |||||||

| Plan D | 758750-379375 | |||||||

| 379375 | ||||||||

| Plan E | 758750+379375 | |||||||

| 1138125 | ||||||||

| b-1 | Compute the EPS If the return to assets fells to 5.35 Percent | |||||||

| Particulars | Current Plan | Plan D | Plan E | |||||

| EBIT-12140000*5.35% | 649490 | 649490 | 649490 | |||||

| Less Interest -Old-12140000/2*10.7% | 649490 | 649490 | 324745 | |||||

| New-3035000*12.7% | 385445 | |||||||

| EBT | 0 | -385445 | 324745 | |||||

| Less Taxes -40% | 0 | -154178 | 129898 | |||||

| EAT | 0 | -231267 | 194847 | |||||

| Common Shares | 758750 | 379375 | 1138125 | |||||

| EPS | 0 | -0.6096 | 0.1712 | |||||

| b-2 | Which Plan would be most favorable if return on assets fell to 5.35% | |||||||

| Plan E will be favorable | ||||||||

| b-3 | Compute the EPS if the return to assets rises to 15.7% | |||||||

| Particulars | Current Plan | Plan D | Plan E | |||||

| EBIT-12140000*15.7% | 1905980 | 1905980 | 1905980 | |||||

| Less Interest -Old-12140000/2*10.7% | 649490 | 649490 | 324745 | |||||

| New-3035000*12.7% | 385445 | |||||||

| EBT | 1256490 | 871045 | 1581235 | |||||

| Less Taxes -40% | 502596 | 348418 | 632494 | |||||

| EAT | 753894 | 522627 | 948741 | |||||

| Common Shares | 758750 | 379375 | 1138125 | |||||

| EPS | 0.9936 | 1.3776 | 0.8336 | |||||

| b-4 | which plan would be most favorable if return on assets rises to 15.7% | |||||||

| Plan D | ||||||||

| C-1 | Dickinson Company | |||||||

| Income Statement | ||||||||

| Particulars | Current Plan | Plan D | Plan E | |||||

| EBIT | 1298980 | 1298980 | 1298980 | |||||

| Less Interest -Old-12140000/2*10.7% | 649490 | 649490 | 324745 | |||||

| New-3035000*12.7% | 385445 | |||||||

| EBIT | 649490 | 264045 | 974235 | |||||

| Less Taxes -40% | 259796 | 105618 | 389694 | |||||

| EAT | 389694 | 158427 | 584541 | |||||

| Common Shares | 758750 | 455250 | 1062250 | |||||

| EPS | 0.5136 | 0.3480 | 0.5503 | |||||

| Calculation of Common Shares | ||||||||

| Existing | 12140000/2 | |||||||

| Equity | 6070000 | |||||||

| Par value of share | $8 | |||||||

| No of common shares | 758,750 | |||||||

| Plan D | 758750-3035000/10 | |||||||

| 455250 | ||||||||

| Plan E | 758750+3035000/10 | |||||||

| 1062250 | ||||||||

| c-2 | If the market price for common stock rose to $10 before restructuring which plan would be most attractive | |||||||

| Plan E | ||||||||

Add Answer to:

Dickinson Company has $12,140,000 million in assets. Currently half of these assets are financed with long-term debt at...

Dickinson Company has $12,140,000 million in assets. Currently half of these assets are financed with long-term...

Dickinson Company has $12,140,000 million in assets. Currently half of these assets are financed with long-term debt at 10.7 percent and half with common stock having a par value of $8. Ms. Smith, Vice President of Finance, wishes to analyze two refinancing plans, one with more debt (D) and one with more equity (E). The company earns a return on assets before interest and taxes of 10.7 percent. The tax rate is 40 percent. Tax loss carryover provisions apply, so...

Dickinson Company has $12,140,000 million in assets. Currently half of these assets are financed with long-term debt at 10.7 percent and half with common stock having a par value of $8. Ms. Smith, Vice President of Finance, wishes to analyze two refinancing plans, one with more debt (D) and one with more equity (E). The company earns a return on assets before interest and taxes of 10.7 percent. The tax rate is 40 percent. Tax loss carryover provisions apply, so...

Dickinson Company has $11,940,000 million in assets. Currently half of these assets are financed with long-term...

Dickinson Company has $11,940,000 million in assets. Currently half of these assets are financed with long-term debt at 9.7 percent and half with common stock having a par value of $8. Ms. Smith, Vice President of Finance, wishes to analyze two refinancing plans, one with more debt (D) and one with more equity (E). The company earns a return on assets before interest and taxes of 9.7 percent. The tax rate is 40 percent. Tax loss carryover provisions apply, so...

Dickinson Company has $12,020,000 million in assets. Currently half of these assets are financed with long-term...

Dickinson Company has $12,020,000 million in assets. Currently

half of these assets are financed with long-term debt at 10.1

percent and half with common stock having a par value of $8. Ms.

Smith, Vice President of Finance, wishes to analyze two refinancing

plans, one with more debt (D) and one with more equity (E). The

company earns a return on assets before interest and taxes of 10.1

percent. The tax rate is 40 percent. Tax loss carryover provisions

apply, so...

Dickinson Company has $12,020,000 million in assets. Currently

half of these assets are financed with long-term debt at 10.1

percent and half with common stock having a par value of $8. Ms.

Smith, Vice President of Finance, wishes to analyze two refinancing

plans, one with more debt (D) and one with more equity (E). The

company earns a return on assets before interest and taxes of 10.1

percent. The tax rate is 40 percent. Tax loss carryover provisions

apply, so...

Dickinson Company has $12,120,000 million in assets. Currently half of these assets are financed with long-term...

Dickinson Company has $12,120,000 million in assets. Currently half of these assets are financed with long-term debt at 10.6 percent and half with common stock having a par value of $8. Ms. Smith, Vice President of Finance, wishes to analyze two refinancing plans, one with more debt (D) and one with more equity (E). The company earns a return on assets before interest and taxes of 10.6 percent. The tax rate is 45 percent. Tax loss carryover provisions apply, so...

Dickinson Company has $12,080,000 million in assets. Currently half of these assets are financed with long-term...

Dickinson Company has $12,080,000 million in assets. Currently half of these assets are financed with long-term debt at 10.4 percent and half with common stock having a par value of $8. Ms. Smith, Vice President of Finance, wishes to analyze two refinancing plans, one with more debt (D) and one with more equity (E). The company earns a return on assets before interest and taxes of 10.4 percent. The tax rate is 40 percent. Tax loss carryover provisions apply, so...

Dickinson Company has $12,080,000 million in assets. Currently half of these assets are financed with long-term debt at 10.4 percent and half with common stock having a par value of $8. Ms. Smith, Vice President of Finance, wishes to analyze two refinancing plans, one with more debt (D) and one with more equity (E). The company earns a return on assets before interest and taxes of 10.4 percent. The tax rate is 40 percent. Tax loss carryover provisions apply, so...

Dickinson Company has $12,060,000 million in assets. Currently half of these assets are financed with long-term...

Dickinson Company has $12,060,000 million in assets. Currently half of these assets are financed with long-term debt at 10.3 percent and half with common stock having a par value of $8. Ms. Smith, Vice President of Finance, wishes to analyze two refinancing plans, one with more debt (D) and one with more equity (E). The company earns a return on assets before interest and taxes of 10.3 percent. The tax rate is 40 percent. Tax loss carryover provisions apply, so...

Dickinson Company has $11,860,000 million in assets. Currently half of these assets are financed with long-term...

Dickinson Company has $11,860,000 million in assets. Currently half of these assets are financed with long-term debt at 9.3 percent and half with common stock having a par value of $8. Ms. Smith, Vice President of Finance, wishes to analyze two refinancing plans, one with more debt (D) and one with more equity (E). The company earns a return on assets before interest and taxes of 9.3 percent. The tax rate is 40 percent. Tax loss carryover provisions apply, so...

Dickinson Company has $11,860,000 million in assets. Currently half of these assets are financed with long-term debt at 9.3 percent and half with common stock having a par value of $8. Ms. Smith, Vice President of Finance, wishes to analyze two refinancing plans, one with more debt (D) and one with more equity (E). The company earns a return on assets before interest and taxes of 9.3 percent. The tax rate is 40 percent. Tax loss carryover provisions apply, so...

Dickinson Company has $12,020,000 million in assets. Currently half of these assets are financed ...

Dickinson Company has $12,020,000 million in assets. Currently

half of these assets are financed with long-term debt at 10.1

percent and half with common stock having a par value of $8. Ms.

Smith, Vice President of Finance, wishes to analyze two refinancing

plans, one with more debt (D) and one with more equity (E). The

company earns a return on assets before interest and taxes of 10.1

percent. The tax rate is 40 percent. Tax loss carryover provisions

apply, so...

Dickinson Company has $12,020,000 million in assets. Currently

half of these assets are financed with long-term debt at 10.1

percent and half with common stock having a par value of $8. Ms.

Smith, Vice President of Finance, wishes to analyze two refinancing

plans, one with more debt (D) and one with more equity (E). The

company earns a return on assets before interest and taxes of 10.1

percent. The tax rate is 40 percent. Tax loss carryover provisions

apply, so...

17. Dickinson Company has $11,820,000 million in assets. Currently half of these assets are financed with...

17. Dickinson Company has $11,820,000 million in assets. Currently half of these assets are financed with long-term debt at 9.1 percent and half with common stock having a par value of $8. Ms. Smith, Vice President of Finance, wishes to analyze two refinancing plans, one with more debt (D) and one with more equity (E). The company earns a return on assets before interest and taxes of 9.1 percent. The tax rate is 40 percent. Tax loss carryover provisions apply,...

Dickinson Company has $12,020,000 million in assets. Currently half of these assets are financed with long-...

Dickinson Company has $12,020,000 million in assets. Currently half of these assets are financed with long- erm debt at 10.1 percent and half with common stock having a par value of $8. Ms. Smith, Vice President of Finance, wishes to analyze two refinancing plans, one with more debt (D) and one with more equity (E). The company eams a return on assets before interest and taxes of 10.1 percent. The tax rate is 40 percent. Tax loss carryover provisions apply,...

Dickinson Company has $12,020,000 million in assets. Currently half of these assets are financed with long- erm debt at 10.1 percent and half with common stock having a par value of $8. Ms. Smith, Vice President of Finance, wishes to analyze two refinancing plans, one with more debt (D) and one with more equity (E). The company eams a return on assets before interest and taxes of 10.1 percent. The tax rate is 40 percent. Tax loss carryover provisions apply,...

Dickinson Company has $12,140,000 million in assets. Currently half of these assets are financed with long-term debt at 10.7 percent and half with common stock having a par value of $8. Ms. Smith, Vice President of Finance, wishes to analyze two refinancing plans, one with more debt (D) and one with more equity (E). The company earns a return on assets before interest and taxes of 10.7 percent. The tax rate is 40 percent. Tax loss carryover provisions apply, so...

Dickinson Company has $12,140,000 million in assets. Currently half of these assets are financed with long-term debt at 10.7 percent and half with common stock having a par value of $8. Ms. Smith, Vice President of Finance, wishes to analyze two refinancing plans, one with more debt (D) and one with more equity (E). The company earns a return on assets before interest and taxes of 10.7 percent. The tax rate is 40 percent. Tax loss carryover provisions apply, so...

Dickinson Company has $12,020,000 million in assets. Currently

half of these assets are financed with long-term debt at 10.1

percent and half with common stock having a par value of $8. Ms.

Smith, Vice President of Finance, wishes to analyze two refinancing

plans, one with more debt (D) and one with more equity (E). The

company earns a return on assets before interest and taxes of 10.1

percent. The tax rate is 40 percent. Tax loss carryover provisions

apply, so...

Dickinson Company has $12,020,000 million in assets. Currently

half of these assets are financed with long-term debt at 10.1

percent and half with common stock having a par value of $8. Ms.

Smith, Vice President of Finance, wishes to analyze two refinancing

plans, one with more debt (D) and one with more equity (E). The

company earns a return on assets before interest and taxes of 10.1

percent. The tax rate is 40 percent. Tax loss carryover provisions

apply, so...

Dickinson Company has $12,080,000 million in assets. Currently half of these assets are financed with long-term debt at 10.4 percent and half with common stock having a par value of $8. Ms. Smith, Vice President of Finance, wishes to analyze two refinancing plans, one with more debt (D) and one with more equity (E). The company earns a return on assets before interest and taxes of 10.4 percent. The tax rate is 40 percent. Tax loss carryover provisions apply, so...

Dickinson Company has $12,080,000 million in assets. Currently half of these assets are financed with long-term debt at 10.4 percent and half with common stock having a par value of $8. Ms. Smith, Vice President of Finance, wishes to analyze two refinancing plans, one with more debt (D) and one with more equity (E). The company earns a return on assets before interest and taxes of 10.4 percent. The tax rate is 40 percent. Tax loss carryover provisions apply, so...

Dickinson Company has $11,860,000 million in assets. Currently half of these assets are financed with long-term debt at 9.3 percent and half with common stock having a par value of $8. Ms. Smith, Vice President of Finance, wishes to analyze two refinancing plans, one with more debt (D) and one with more equity (E). The company earns a return on assets before interest and taxes of 9.3 percent. The tax rate is 40 percent. Tax loss carryover provisions apply, so...

Dickinson Company has $11,860,000 million in assets. Currently half of these assets are financed with long-term debt at 9.3 percent and half with common stock having a par value of $8. Ms. Smith, Vice President of Finance, wishes to analyze two refinancing plans, one with more debt (D) and one with more equity (E). The company earns a return on assets before interest and taxes of 9.3 percent. The tax rate is 40 percent. Tax loss carryover provisions apply, so...

Dickinson Company has $12,020,000 million in assets. Currently

half of these assets are financed with long-term debt at 10.1

percent and half with common stock having a par value of $8. Ms.

Smith, Vice President of Finance, wishes to analyze two refinancing

plans, one with more debt (D) and one with more equity (E). The

company earns a return on assets before interest and taxes of 10.1

percent. The tax rate is 40 percent. Tax loss carryover provisions

apply, so...

Dickinson Company has $12,020,000 million in assets. Currently

half of these assets are financed with long-term debt at 10.1

percent and half with common stock having a par value of $8. Ms.

Smith, Vice President of Finance, wishes to analyze two refinancing

plans, one with more debt (D) and one with more equity (E). The

company earns a return on assets before interest and taxes of 10.1

percent. The tax rate is 40 percent. Tax loss carryover provisions

apply, so...

Dickinson Company has $12,020,000 million in assets. Currently half of these assets are financed with long- erm debt at 10.1 percent and half with common stock having a par value of $8. Ms. Smith, Vice President of Finance, wishes to analyze two refinancing plans, one with more debt (D) and one with more equity (E). The company eams a return on assets before interest and taxes of 10.1 percent. The tax rate is 40 percent. Tax loss carryover provisions apply,...

Dickinson Company has $12,020,000 million in assets. Currently half of these assets are financed with long- erm debt at 10.1 percent and half with common stock having a par value of $8. Ms. Smith, Vice President of Finance, wishes to analyze two refinancing plans, one with more debt (D) and one with more equity (E). The company eams a return on assets before interest and taxes of 10.1 percent. The tax rate is 40 percent. Tax loss carryover provisions apply,...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago