Homework Answers

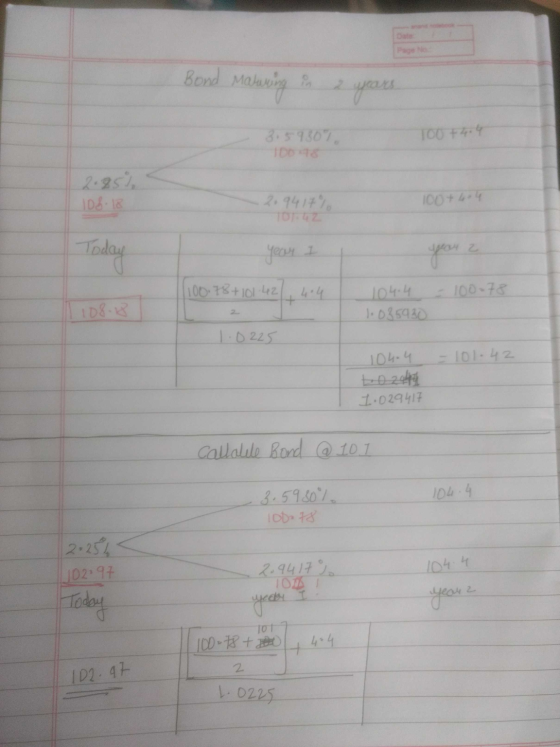

1.) $ 103.18

2.) $ 102.97

3.) If Bond is callable at Par then Value at Node 1 & 2 for Year 1 will be capped at $100 + $4.4. Thus value at Node 0 will be $102.10

4.) If Volatality is lowered to 5% instead of 10% then the value of a callable bond would increase. This happens due to the value of call option embedded in the bond is affected the value of straight bond remains unaffected. Thus is volatality is lowered call option woul gain thus increasing the calue of a callable bond.

Add Answer to:

1. You observe the following set of spot rates: Time Period Oyly Oy2y Оузу Rate 2.25%...

Use the following information for questions 6-11. A BB+ rated firm (0.8., a high yield or...

Use the following information for questions 6-11. A BB+ rated firm (0.8., a high yield or non-investment grade) has issued a callable bond with the following features: • Exactly 2 years to maturity • 9% annual coupon • $100 par value • The bond is callable in exactly one year for par value. 6. Relative to a non-callable bond with identical features, the price of the callable bond will be a. Lower, because the buyer of the bond is also...

Use the following information for questions 6-11. A BB+ rated firm (0.8., a high yield or non-investment grade) has issued a callable bond with the following features: • Exactly 2 years to maturity • 9% annual coupon • $100 par value • The bond is callable in exactly one year for par value. 6. Relative to a non-callable bond with identical features, the price of the callable bond will be a. Lower, because the buyer of the bond is also...

Debt & Bonds 1. The table below presents the spot rates an investor faces. Year Spot...

Debt & Bonds

1. The table below presents the spot rates an investor

faces.

Year

Spot Rate

1

2%

2

3%

3

4%

4

5%

Assume that, for each maturity, there is a zero-coupon bond

traded in the market. These zeros pay $1,000 at their respective

maturity.

a. Is the term structure positive, inverted, or flat?

b. What is the forward rate from t=1 to t=2?

c. Suppose that the investor is expecting to receive $1 million

at t=1. This...

Debt & Bonds

1. The table below presents the spot rates an investor

faces.

Year

Spot Rate

1

2%

2

3%

3

4%

4

5%

Assume that, for each maturity, there is a zero-coupon bond

traded in the market. These zeros pay $1,000 at their respective

maturity.

a. Is the term structure positive, inverted, or flat?

b. What is the forward rate from t=1 to t=2?

c. Suppose that the investor is expecting to receive $1 million

at t=1. This...

Please answer the following time value of money questions below. Charting out each of the problem...

Please answer the following time value of money questions below. Charting out each of the problem elements (ex. N = 10, PV = 500, etc.) will not only help you in answering the questions but will also assist me in following your calculations. 1. Calculate the value of a bond with a coupon rate of 7.5% and market interest rate of 9% that matures in 12 years. 2. What is the value of the bond in question 1 if the...

Please answer the following time value of money questions below. Charting out each of the problem elements (ex. N = 10, PV = 500, etc.) will not only help you in answering the questions but will also assist me in following your calculations. 1. Calculate the value of a bond with a coupon rate of 7.5% and market interest rate of 9% that matures in 12 years. 2. What is the value of the bond in question 1 if the...

Please answer the following time value of money questions below. Charting out each of the problem...

Please answer the following time value of money questions below. Charting out each of the problem elements (ex. N = 10, PV = 500, etc.) will not only help you in answering the questions but will also assist me in following your calculations. 1. Calculate the value of a bond with a coupon rate of 7.5% and market interest rate of 9% that matures in 12 years. 2. What is the value of the bond in question 1 if the...

Please answer the following time value of money questions below. Charting out each of the problem elements (ex. N = 10, PV = 500, etc.) will not only help you in answering the questions but will also assist me in following your calculations. 1. Calculate the value of a bond with a coupon rate of 7.5% and market interest rate of 9% that matures in 12 years. 2. What is the value of the bond in question 1 if the...

1.a. Calculate the price and duration for the following bond when the going rate of interest...

1.a. Calculate the price and duration for the following bond when the going rate of interest is 3%. The bond offers 2.75% coupon rate, matures in 3 years and has a par value of $1,000. Show full calculations in the table below. YR PV of $ 1 at 3% Bond Cash Flows PV (Cash Flows) Year * Present Value of Cash Flow 1 2 3 3 Total Price = Duration

If you buy a callable bond and interest rates decline, will the value of your bond...

If you buy a callable bond and interest rates decline, will the value of your bond rise by as much as it would have risen if the bond had not been callable? Explain. Here is what I have so far: A callable bond is a bond that can be redeemed before its maturity date. This basically means that the issuer can call the bond at a predetermined call date if they chose to. If interest rates decline in the market,...

Spot rates and forward rates. On January 1, 2015, one USD can be exchanged for eight...

Spot rates and forward rates. On January 1, 2015, one USD can be exchanged for eight foreign currencies (FC). The dollar can be invested short term at a rate of 4%, and the FC can be invested at 5%. 1. Calculate the direct and indirect spot exchange rates for Jan 1, 2015. 2. Calculate the 180-day forward rate to buy FC (assume 365 days per year.) 3. If the spot rate is 1FC = $0.740 and the 90-day forward rate...

You are given the following benchmark spot rates: Maturity Spot Rate 1 2.90% 2 3.20% 3...

You are given the following benchmark spot rates: Maturity Spot Rate 1 2.90% 2 3.20% 3 3.60% 4 4.20% a) Compute the forward rate between years 1 and 2. b) Compute the forward rate between years 1 and 3. c) What is the zero price today of a five-year zero-coupon bond if the forward price for a one-year zero-coupon bond beginning in four years is known to be 0.9461 d) Calculate the price of a 4% annual coupon corporate bond...

Tenor (yr) Spot Rate 1 0.58% 2 0.80% 3 1.01% 4 1.19% 5 1.36% 7 1.67%...

Tenor (yr) Spot Rate 1 0.58% 2 0.80% 3 1.01% 4 1.19% 5 1.36% 7 1.67% 8 1.79% 9 1.89% 10 1.98% What is the price of a three-years to maturity risky bond that pays 3% annual coupon if the bond is callable at face value (assuming a face value of $100)? What is the dollar value of the embedded call option? Note:An identical bond is currently trading with an OAS of 150 bps, and your analysis of interest rates...

Use the following information for problems 1, 2, 3, and 4: A non-callable $1,000 par- value...

Use the following information for problems 1, 2, 3, and 4: A non-callable $1,000 par- value bond matures in thirty years at par. The annual coupon rate is 5% with coupons payable annually. The bond was purchased at a price to yield an annual effective rate of 4%. 1. (1 point) Find the bond purchase price. 2. (1 point) Calculate the Macaulay duration and the modified duration for this bond. 3. (2 points) Suppose that the market interest rate increases...

Use the following information for problems 1, 2, 3, and 4: A non-callable $1,000 par- value bond matures in thirty years at par. The annual coupon rate is 5% with coupons payable annually. The bond was purchased at a price to yield an annual effective rate of 4%. 1. (1 point) Find the bond purchase price. 2. (1 point) Calculate the Macaulay duration and the modified duration for this bond. 3. (2 points) Suppose that the market interest rate increases...

Use the following information for questions 6-11. A BB+ rated firm (0.8., a high yield or non-investment grade) has issued a callable bond with the following features: • Exactly 2 years to maturity • 9% annual coupon • $100 par value • The bond is callable in exactly one year for par value. 6. Relative to a non-callable bond with identical features, the price of the callable bond will be a. Lower, because the buyer of the bond is also...

Use the following information for questions 6-11. A BB+ rated firm (0.8., a high yield or non-investment grade) has issued a callable bond with the following features: • Exactly 2 years to maturity • 9% annual coupon • $100 par value • The bond is callable in exactly one year for par value. 6. Relative to a non-callable bond with identical features, the price of the callable bond will be a. Lower, because the buyer of the bond is also...

Debt & Bonds

1. The table below presents the spot rates an investor

faces.

Year

Spot Rate

1

2%

2

3%

3

4%

4

5%

Assume that, for each maturity, there is a zero-coupon bond

traded in the market. These zeros pay $1,000 at their respective

maturity.

a. Is the term structure positive, inverted, or flat?

b. What is the forward rate from t=1 to t=2?

c. Suppose that the investor is expecting to receive $1 million

at t=1. This...

Debt & Bonds

1. The table below presents the spot rates an investor

faces.

Year

Spot Rate

1

2%

2

3%

3

4%

4

5%

Assume that, for each maturity, there is a zero-coupon bond

traded in the market. These zeros pay $1,000 at their respective

maturity.

a. Is the term structure positive, inverted, or flat?

b. What is the forward rate from t=1 to t=2?

c. Suppose that the investor is expecting to receive $1 million

at t=1. This...

Please answer the following time value of money questions below. Charting out each of the problem elements (ex. N = 10, PV = 500, etc.) will not only help you in answering the questions but will also assist me in following your calculations. 1. Calculate the value of a bond with a coupon rate of 7.5% and market interest rate of 9% that matures in 12 years. 2. What is the value of the bond in question 1 if the...

Please answer the following time value of money questions below. Charting out each of the problem elements (ex. N = 10, PV = 500, etc.) will not only help you in answering the questions but will also assist me in following your calculations. 1. Calculate the value of a bond with a coupon rate of 7.5% and market interest rate of 9% that matures in 12 years. 2. What is the value of the bond in question 1 if the...

Please answer the following time value of money questions below. Charting out each of the problem elements (ex. N = 10, PV = 500, etc.) will not only help you in answering the questions but will also assist me in following your calculations. 1. Calculate the value of a bond with a coupon rate of 7.5% and market interest rate of 9% that matures in 12 years. 2. What is the value of the bond in question 1 if the...

Please answer the following time value of money questions below. Charting out each of the problem elements (ex. N = 10, PV = 500, etc.) will not only help you in answering the questions but will also assist me in following your calculations. 1. Calculate the value of a bond with a coupon rate of 7.5% and market interest rate of 9% that matures in 12 years. 2. What is the value of the bond in question 1 if the...

Use the following information for problems 1, 2, 3, and 4: A non-callable $1,000 par- value bond matures in thirty years at par. The annual coupon rate is 5% with coupons payable annually. The bond was purchased at a price to yield an annual effective rate of 4%. 1. (1 point) Find the bond purchase price. 2. (1 point) Calculate the Macaulay duration and the modified duration for this bond. 3. (2 points) Suppose that the market interest rate increases...

Use the following information for problems 1, 2, 3, and 4: A non-callable $1,000 par- value bond matures in thirty years at par. The annual coupon rate is 5% with coupons payable annually. The bond was purchased at a price to yield an annual effective rate of 4%. 1. (1 point) Find the bond purchase price. 2. (1 point) Calculate the Macaulay duration and the modified duration for this bond. 3. (2 points) Suppose that the market interest rate increases...

Most questions answered within 3 hours.

-

Where is the error in this code sequence?

String s1 = "Hello";

String s2 = "ello";...

asked 11 months ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 11 months ago -

Consider this reaction:

Al2(SO4)3 (aq)+ BaCl3

(aq) Al2Cl6 (aq)- +

3BaSO4(s) . What is the...

asked 11 months ago -

Suppose that Savneet is considering increasing her

recent random sample from 20 car rentals to 40...

asked 11 months ago -

Trucks arrive at an unloading terminal at an average rate of 120

per hour.

Trucks arrive...

asked 11 months ago -

Why are methanol and ethanol completely soluble in water while

octanol is not very little soluble....

asked 11 months ago -

A facilities manager at a university reads in a research report

that the mean amount of...

asked 11 months ago -

When the CuSO4 is rehydrated by adding water to the anhydrous

compound, is this an endothermic...

asked 11 months ago -

A ray of sunlight is passing from diamond into crown glass; the

angle of incidence is...

asked 11 months ago -

A block of mass 0.249 kg is placed on top of a light, vertical

spring of...

asked 11 months ago -

how do the kidneys compensate in the presences of acidosis

a) trigger hyperventilate

b) reserve acid...

asked 11 months ago -

Question 501 pts

The rental rate of capital to the firm increases. Which of the

following...

asked 11 months ago